2K Sports 2009 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2009 2K Sports annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

|

|

3. FAIR VALUE MEASURES

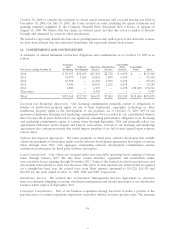

As of November 1, 2008, we adopted the guidance for Fair Value Measurements which establishes a three-

level fair value hierarchy that prioritizes the inputs used to measure fair value. This hierarchy requires

entities to maximize the use of ‘‘observable inputs’’ and minimize the use of ‘‘unobservable inputs.’’ The

three levels of inputs used to measure fair value are as follows:

P %9J9@Q*ICH98DF=79G=B57H=J9A5F?9HG:CF=89BH=75@5GG9HGCF@=56=@=H=9G

P %9J9@Q(6G9FJ56@9=BDIHGCH<9FH<5BEICH98DF=79G=B7@I898=B%9J9@GI7<5GEICH98DF=79G:CF

A5F?9HGH<5H5F9BCH57H=J9CFCH<9F=BDIHGH<5H5F9C6G9FJ56@9CF75B697CFFC6CF5H986MC6G9FJ56@9

A5F?9H85H5

P %9J9@ Q.BC6G9FJ56@9 =BDIHG H<5H 5F9 GIDDCFH98 6M @=HH@9 CF BC A5F?9H 57H=J=HM 5B8 H<5H 5F9

significant to the fair value of the assets or liabilities. This includes certain pricing models,

discounted cash flow methodologies and similar techniques that use significant unobservable inputs.

The table below segregates all financial assets and liabilities that are measured at fair value on a recurring

basis into the most appropriate level within the fair value hierarchy based on the inputs used to determine

the fair value at the measurement date.

Quoted prices

in active markets Significant other Significant unobservable

for identical assets observable inputs inputs

October 31, 2009 (level 1) (level 2) (level 3)

&CB9MA5F?9H:IB8G Q Q

5B?H=A989DCG=H Q Q

4. BUSINESS ACQUISITIONS AND CONSOLIDATION

We consummated the acquisitions described below, which largely reflect our strategy to diversify our

business by adding experienced development studios, intellectual properties and talented personnel

resources to our existing infrastructure. The acquisitions were not considered to be material to our

consolidated statements of operations, individually or in the aggregate. The results of operations and

financial positions of these acquisitions are included in our consolidated financial statements from their

respective acquisition dates forward and therefore affect comparability from period to period. During the

M95FG 9B898 (7HC69F 5B8 K9 D5=8 7CBH=B;9BH 7CBG=89F5H=CB C: 5B8

:CFCIFDF=CFM95F57EI=G=H=CBG

Cash and Goodwill

Development Value of Recorded on Identified

Acquisition Advances Stock Acquisition Intangible

Acquired Business Date Paid Issued Date Assets Contingent Consideration

&58C7 &5F7< .DHCD5M56@9=B75G<CFGHC7?

,C:HK5F9%% based on meeting certain employment

provisions and future product sales.

"@@IG=CB,C:HKCF?G 979A69F .DHC65G98CB:IHIF9DFC8I7H

sales.

"B &5F7< K9 57EI=F98 H<9 5GG9HG C: +C7?GH5F '9K B;@5B8 :CFA9F@M ?BCKB 5G &58 C7

,C:HK5F9 %% 44+C7?GH5F '9K B;@5B8 5B =B89D9B89BH 89J9@CDA9BH GHI8=C =B 'CFH< A9F=75 5B8

89J9@CD9FC:H<9I@@M:F5B7<=G9-CH5@7CBG=89F5H=CBD5=8IDCB57EI=G=H=CBK5G7CBG=GH=B;C:

=B75G<G<5F9GC:CIFIBF9;=GH9F987CAACBGHC7?5B8C:89J9@CDA9BH58J5B79GD5=8DF=CFHC

the acquisition. The terms of the transaction also include additional contingent deferred payments of up to

D5M56@9=B75G<CFGHC7?65G98CBA99H=B;79FH5=B9AD@CMA9BHDFCJ=G=CBGH<9F9@95G9C:G9J9F5@