TCF Bank 2004 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2004 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

2004 Annual Report 43

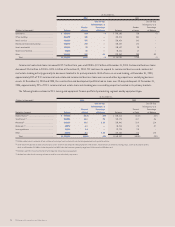

Commitments to lend are agreements to lend to a customer pro-

vided there is no violation of any condition in the contract. These

commitments generally have fixed expiration dates or other termi-

nation clauses and may require payment of a fee. Since certain of

the commitments are expected to expire without being drawn upon,

the total commitment amounts do not necessarily represent future

cash requirements. Collateral predominantly consists of residential

and commercial real estate.

Loans serviced with recourse represent a contingent guarantee

based upon the failure to perform by another party. These loans

consist of $94.9 million of Veterans Administration (“VA”) loans. As

is typical of a servicer of VA loans, TCF must cover any principal loss

in excess of the VA’s guarantee if the VA elects its “no-bid” option

upon the foreclosure of a loan. Since conditions under which TCF

would be required either to cover any principal loss in excess of the

VA’s guarantee may not materialize, the actual cash requirements

are expected to be significantly less than the amount provided in

the table above.

Standby letters of credit and guarantees on industrial revenue

bonds are conditional commitments issued by TCF guaranteeing

the performance of a customer to a third party. These conditional

commitments expire in various years through the year 2009. Since

the conditions under which TCF is required to fund these commitments

may not materialize, the cash requirements are expected to be less

than the total outstanding commitments. Collateral held on these

commitments primarily consists of commercial real estate mortgages.

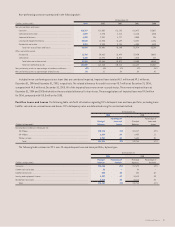

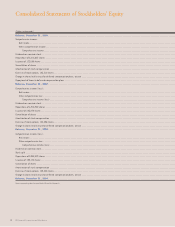

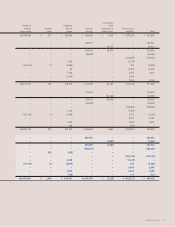

Stockholders’ Equity Stockholders’ equity at December 31,

2004 was $958.4 million, or 7.8% of total assets, up from $920.9 mil-

lion, or 8.1% of total assets, at December 31, 2003. The increase in

stockholders’ equity was primarily due to the net income of $255

million partially offset by the repurchase of 4 million shares of TCF’s

common stock at a cost of $116.1 million, the payment of $104 mil-

lion in dividends on common stock and a $7.1 million decrease in

accumulated comprehensive income for the year ended December

31, 2004. On July 21, 2003, TCF’s Board of Directors authorized the

repurchase of up to an additional 5% of TCF’s common stock, or

7.2 million shares. At December 31,2004, 3.5 million shares remain

available under this authorization from the Board of Directors.

Since January 1, 1998, the Company has repurchased 54.2 million

shares of its common stock at an average cost of $17.58 per share.

For the year ended December 31, 2004, average total equity to

average assets was 7.94% compared with 8.03% for the year ended

December 31, 2003. Dividends paid to common shareholders on

a per share basis totaled 75 cents in 2004, an increase of 15.4%

from 65 cents in 2003. TCF’s dividend payout ratio was 40.3% in

2004 and 42.6% in 2003. The Company’s primary funding sources

for common dividends are dividends received from its subsidiary

bank. At December 31, 2004, TCF and TCF National Bank exceeded

their regulatory capital requirements and are considered “well-

capitalized” under guidelines established by the Federal Reserve

Board and the Office of the Comptroller of the Currency. See Notes

15 and 16 of Notes to Consolidated Financial Statements. TCF has

used stock options as a form of employee compensation to a lim-

ited extent in prior years. At December 31, 2004, the number of

incentive stock options outstanding was 325,864, or.18%, of total

shares outstanding.

Market Risk – Interest-Rate Risk TCF’s results of operations

are dependent to a large degree on its net interest income and its

ability to manage its interest rate risk. Although TCF manages other

risks, such as credit and liquidity risk, in the normal course of its

business, the Company considers interest rate risk to be its most

significant market risk. Since TCF does not hold a trading portfolio,

the Company is not exposed to market risk from trading activities.

The mismatch between maturities, interest rate sensitivities and

prepayment characteristics of assets and liabilities results in inter-

est rate risk. TCF, like most financial institutions, has material inter-

est rate risk exposure to changes in both short-term and long-term

interest rates as well as variable interest rate indices (e.g., prime).

TCF’s Asset/Liability Committee manages TCF’s interest rate risk

based on interest rate expectations and other factors. The principal

objective of TCF’s asset/liability management activities is to provide

maximum levels of net interest income while maintaining acceptable

levels of interest rate risk and liquidity risk and facilitating the

funding needs of the Company.