TCF Bank 2004 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2004 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

2004 Annual Report 37

can be reached regarding TCF or for purposes of making comparisons

to other companies. Most of TCF’s non-performing assets and past

due loans and leases are secured by residential real estate. Given the

nature of these assets and the related mortgage foreclosure, property

sale and, if applicable, mortgage insurance claims processes, it can

take 18 months or longer for a loan to migrate from initial delinquency

to final disposition. This resolution process generally takes much

longer for loans secured by real estate than for unsecured loans or

loans secured by other property primarily due to state foreclosure laws.

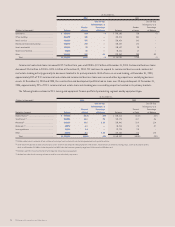

The key indicators of TCF’s credit quality and reserve coverage

for 2004 include the ratio of net charge-offs to average loans and

leases of .11%, the year-end allowance as a multiple of net charge-

offs of 8.4X, and income before income taxes and provision for loan

losses as a multiple of net charge-offs of 41.7X.

The following table sets forth information detailing the allowance for loan and lease losses and selected key indicators:

Year Ended December 31,

(Dollars in thousands) 2004 2003 2002 2001 2000

Balance at beginning of year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 76,619 $ 77,008 $ 75,028 $ 66,669 $ 55,755

Charge-offs:

Consumer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (4,821) (5,362) (6,939) (6,605) (7,041)

Commercial real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (602) (1,381) (2,181) (122) (76)

Commercial business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (235) (920) (5,952) (429) (143)

Leasing and equipment finance . . . . . . . . . . . . . . . . . . . . . . . . . . (8,508) (8,620) (9,230) (9,794) (2,426)

Residential real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (81) (86) (59) (1) (15)

(14,247) (16,369) (24,361) (16,951) (9,701)

Recoveries:

Consumer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,589 2,173 2,965 3,487 4,576

Commercial real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126 45 43 103 295

Commercial business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82 138 54 193 690

Leasing and equipment finance . . . . . . . . . . . . . . . . . . . . . . . . . . 2,963 1,083 1,264 649 254

Residential real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 899 –28

4,768 3,448 4,335 4,432 5,843

Net charge-offs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (9,479) (12,921) (20,026) (12,519) (3,858)

Provision charged to operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10,947 12,532 22,006 20,878 14,772

Acquired allowance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,791 ––––

Balance at end of year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 79,878 $ 76,619 $ 77,008 $ 75,028 $ 66,669

Key Indicators:

Ratio of net loan and lease charge-offs to average loans

and leases outstanding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11% .16% .25% .15% .05%

Year-end allowance as a multiple of net charge-offs . . . . . . . . . . . . . 8.4X 5.9X 3.8X 6.0X 17.3X

Income before income taxes and provision for loan losses

as a multiple of net charge-offs . . . . . . . . . . . . . . . . . . . . . . . . . 41.7X 26.3X 19.0X 28.0X 82.3X

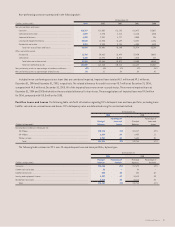

The allocation of TCF’s allowance for loan and lease losses is as follows:

Allocations as a Percentage of Total

Loans and Leases Outstanding by Type

At December 31, At December 31,

(Dollars in thousands) 2004 2003 2002 2001 2000 2004 2003 2002 2001 2000

Consumer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 9,939 $ 9,084 $ 8,532 $ 8,355 $ 9,764 .22% .25% .28% .33% .44%

Commercial real estate . . . . . . . . . . . . . . . . . 20,742 25,142 22,176 24,459 20,753 .96 1.31 1.21 1.51 1.51

Commercial business . . . . . . . . . . . . . . . . . . . 7,696 11,797 15,910 12,117 9,668 1.81 2.76 3.62 2.87 2.36

Leasing and equipment finance . . . . . . . . . . . 24,566 13,515 12,881 11,774 7,583 1.79 1.16 1.24 1.23 .89

Unallocated . . . . . . . . . . . . . . . . . . . . . . . . 16,139 16,139 16,139 16,139 16,139 N.A. N.A. N.A. N.A. N.A.

Subtotal . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79,082 75,677 75,638 72,844 63,907 .94 1.06 1.20 1.32 1.31

Residential real estate . . . . . . . . . . . . . . . . . 796 942 1,370 2,184 2,762 .08 .08 .08 .08 .08

Total allowance balance . . . . . . . . . . . . . $79,878 $76,619 $77,008 $75,028 $66,669 .85 .92 .95 .91 .78

N.A. Not Applicable.