TCF Bank 2004 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2004 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

24 TCF Financial Corporation and Subsidiaries

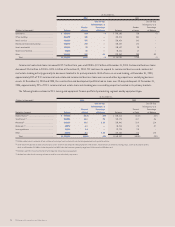

Achieving net interest margin growth over time is dependent on

TCF’s ability to generate higher-yielding assets and lower-cost

retail deposits. The net impact of the changes in interest-bearing

assets and deposits and borrowings has positioned TCF to be asset

sensitive (i.e. more assets than liabilities will be maturing, repricing,

or prepaying during the next twelve months). Although this positive

gap position may benefit TCF in a rising rate environment, if interest

rates remain at current levels or fall further, the net interest margin

may compress and net interest income may decline. An increase in

interest rates would affect TCF’s fixed-rate/variable-rate product

origination mix and would extend the estimated life of its residen-

tial real estate loan and mortgage-backed securities portfolios. A

change in origination mix and/or the extending of the estimated

life of mortgage-related assets may have an adverse impact on

future net interest income or net interest margin as fixed-rate

assets are funded with interest-bearing liabilities with increasing

rates. Competition for checking, savings and money market deposits,

important sources of lower-cost funds for TCF, is intense. A decline

in these low-cost deposits may have an adverse impact on future

net interest income or net interest margin as TCF would need to

replace these funds with short- or long-term borrowings which may

have a higher interest cost. See “Consolidated Financial Condition

Analysis – Market Risk – Interest-Rate Risk” and “Consolidated

Financial Condition Analysis – Deposits” for further discussion on

TCF’s interest rate risk position.

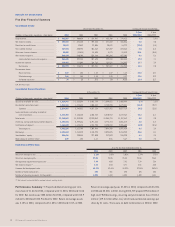

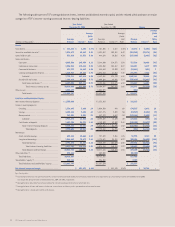

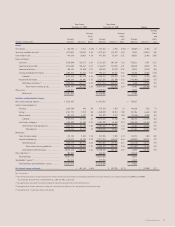

The following table presents the components of the changes in net interest income by volume and rate:

Year Ended Year Ended

December 31, 2004 December 31, 2003

Versus Same Period in 2003 Versus Same Period in 2002

Increase (Decrease) Due to Increase (Decrease) Due to

(In thousands) Volume(1) Rate(1) Total Volume(1) Rate(1) Total

Interest income:

Investments . . . . . . . . . . . . . . . . . . . . . . . . $ 890 $ (1,946) $ (1,056) $ (2,375) $ (48) $ (2,423)

Securities available for sale . . . . . . . . . . . . (18,761) (4,417) (23,178) 713 (15,164) (14,451)

Loans held for sale . . . . . . . . . . . . . . . . . . . (5,775) (2,708) (8,483) 2,421 (4,869) (2,448)

Loans and leases:

Consumer . . . . . . . . . . . . . . . . . . . . . . . 44,623 (14,155) 30,468 40,204 (32,725) 7,479

Commercial real estate . . . . . . . . . . . . 8,743 (7,164) 1,579 7,026 (16,514) (9,488)

Commercial business . . . . . . . . . . . . . . (594) 143 (451) 518 (4,197) (3,679)

Leasing and equipment finance . . . . . 13,597 (6,145) 7,452 8,009 (11,544) (3,535)

Residential real estate . . . . . . . . . . . . (19,557) (5,484) (25,041) (49,442) (13,857) (63,299)

Total interest income . . . . . . . . . . . . . . . . . . . . 13,444 (32,154) (18,710) 1,006 (92,850) (91,844)

Interest expense:

Checking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189 2,683 2,872 209 (740) (531)

Savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (119) (1,689) (1,808) 2,535 (9,161) (6,626)

Money market . . . . . . . . . . . . . . . . . . . . . . . (566) (889) (1,455) (329) (4,961) (5,290)

Certificates of deposit . . . . . . . . . . . . . . . . (5,508) (8,315) (13,823) (10,602) (15,542) (26,144)

Short-term borrowings . . . . . . . . . . . . . . . . 684 2,529 3,213 2,693 (3,145) (452)

Long-term borrowings . . . . . . . . . . . . . . . . 9,982 (28,437) (18,455) (26,838) (7,883) (34,721)

Total interest expense . . . . . . . . . . . . . . . . . . . . 3,911 (33,367) (29,456) 1,396 (75,160) (73,764)

Net interest income . . . . . . . . . . . . . . . . . . . . . . 10,247 499 10,746 685 (18,765) (18,080)

(1) Changes attributable to the combined impact of volume and rate have been allocated proportionately to the change due to volume and the change due to rate.