Chevron 2008 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2008 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

Chevron Corporation 2008 Annual Report 85

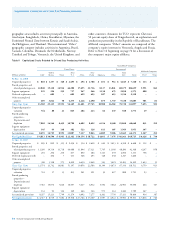

Assumptions The following weighted-average assumptions were used to determine benefit obligations and net periodic benefit costs

for years ended December 31:

Pension Benefits

2008 2007 2006 Other Benefits

U.S. Int’l. U.S. Int’l. U.S. Int’l. 2008 2007 2006

Assumptions used to determine

benefit obligations

Discount rate 6.3% 7.5% 6.3% 6.7% 5.8% 6.0% 6.3% 6.3% 5.8%

Rate of compensation increase 4.5% 6.8% 4.5% 6.4% 4.5% 6.1% 4.0% 4.5% 4.5%

Assumptions used to determine

net periodic benefit cost

Discount rate* 6.3% 6.7% 5.8% 6.0% 5.8% 5.9% 6.3% 5.8% 5.9%

Expected return on plan assets 7.8% 7.4% 7.8% 7.5% 7.8% 7.4% N/A N/A N/A

Rate of compensation increase 4.5% 6.4% 4.5% 6.1% 4.2% 5.1% 4.5% 4.5% 4.2%

* The 2006 U.S. discount rate reflects remeasurement on July 1, 2006, due to plan combinations and changes, primarily several Unocal plans into related Chevron plans.

Expected Return on Plan Assets The company’s estimated

long-term rate of return on pension assets is driven pri marily

by actual historical asset-class returns, an assessment of

expected future performance, advice from external actuarial

firms and the incorporation of specific asset-class risk factors.

Asset allocations are periodically updated using pension plan

asset/liability studies, and the company’s estimated long-term

rates of return are consistent with these studies.

There have been no changes in the expected long-term

rate of return on plan assets since 2002 for U.S. plans, which

account for 68 percent of the company’s pension plan assets.

At December 31, 2008, the estimated long-term rate of

return on U.S. pension plan assets was 7.8 percent.

The market-related value of assets of the major U.S. pen-

sion plan used in the determination of pension expense was

based on the market values in the three months preceding

the year-end measurement date, as opposed to the maximum

allowable period of five years under U.S. accounting rules.

Management considers the three-month time period long

enough to minimize the effects of distortions from day-to-

day market volatility and still be contemporaneous to the

end of the year. For other plans, market value of assets as of

year-end is used in calculating the pension expense.

Discount Rate The discount rate assumptions used to deter-

mine U.S. and international pension and postretirement

benefit plan obligations and expense reflect the prevailing

rates available on high-quality, fixed-income debt instruments.

At December 31, 2008, the company selected a 6.3 percent

discount rate for the major U.S. pension and postretirement

plans. This rate was based on a cash flow analysis that

matched estimated future benefit payments to the Citigroup

Pension Discount Yield Curve as of year-end 2008. The

discount rates at the end of 2007 and 2006 were 6.3 percent

and 5.8 percent, respectively.

Note 22 Employee Benefit Plans – Continued

Other Benefit Assumptions For the measurement of accumu-

lated postretirement benefit obligation at December 31, 2008,

for the main U.S. postretirement medical plan, the assumed

health care cost-trend rates start with 7 percent in 2009 and

gradually decline to 5 percent for 2017 and beyond. For this

measurement at December 31, 2007, the assumed health care

cost-trend rates started with 8 percent in 2008 and gradually

declined to 5 percent for 2014 and beyond. In both measure-

ments, the annual increase to company contributions was

capped at 4 percent.

Assumed health care cost-trend rates can have a signifi-

cant effect on the amounts reported for retiree health care

costs. The impact is mitigated by the 4 percent cap on the

company’s medical contributions for the primary U.S. plan.

A one-percentage-point change in the assumed health care

cost-trend rates would have the following effects:

1 Percent 1 Percent

Increase Decrease

Effect on total service and interest cost components $ 9 $ (8)

Effect on postretirement benefit obligation $ 88 $ (75)

Plan Assets and Investment Strategy The company’s pension

plan weighted-average asset allocations at December 31 by

asset category are as follows:

U.S. International

Asset Category 2008 2007 2008 2007

Equities 52% 64% 47% 56%

Fixed Income 34% 23% 50% 43%

Real Estate 13% 12% 2% 1%

Other 1% 1% 1% –

Total 100% 100% 100% 100%