TCF Bank 2003 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2003 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

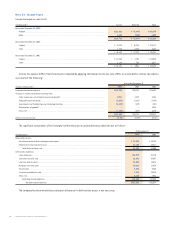

54 TCF Financial Corporation and Subsidiaries

Income Taxes Income taxes are accounted for using the asset

and liability method. Under this method, deferred tax assets and

liabilities are recognized for the future tax consequences attributable

to differences between the financial statement carrying amounts of

existing assets and liabilities and their respective tax bases. Deferred

tax assets and liabilities are measured using enacted tax rates

expected to apply to taxable income in the years in which those tem-

porary differences are expected to be recovered or settled. The effect

on deferred tax assets and liabilities of a change in tax rates is rec-

ognized in income in the period that includes the enactment date.

The determination of current and deferred income taxes is based

on complex analyses of many factors including interpretation of

Federal and state income tax laws, the difference between tax

and financial reporting basis of assets and liabilities (temporary

differences), estimates of amounts due or owed such as the timing

of reversals of temporary differences and current financial account-

ing standards. Actual results could differ significantly from the

estimates and interpretations used in determining the current and

deferred income tax liabilities.

Lease Financing TCF provides various types of lease financing

that are classified for accounting purposes as either direct financing,

sales-type, leveraged or operating leases. Leases that transfer sub-

stantially all of the benefits and risks of equipment ownership to the

lessee are classified as direct financing or sales-type leases and are

included in loans and leases. Direct financing and sales-type leases

are carried at the combined present value of the future minimum

lease payments and the lease residual value. Investments in leveraged

leases are the sum of all lease payments (less non-recourse debt

payments) plus estimated residual values, less unearned income.

The determination of the lease classification requires various judg-

ments and estimates by management including the fair value of the

equipment at lease inception, useful life of the equipment under

lease, and collectibility of minimum lease payments.

Sales-type leases generate dealer profit which is recognized at

lease inception by recording lease revenue net of the lease cost.

Lease revenue consists of the present value of the future minimum

lease payments discounted at the rate implicit in the lease. Lease

cost consists of the leased equipment’s book value, less the present

value of its residual. The revenues associated with other types of

leases are recognized over the term of the underlying leases. Interest

income on direct financing and sales-type leases is recognized using

methods which approximate a level yield over the term of the leases.

Income from leveraged leases is recognized using a method which

approximates a level yield over the term of the leases based on the

unrecovered equity investment. Management has policies and proce-

dures in place for the determination of lease classification and

review of the related judgments and estimates for all lease financings.

Additionally, some lease financings include a residual value

component, which represents the estimated value of the leased

equipment at the end of the initial term of the lease. The estimation

of residual values involves judgments regarding product and technol-

ogy changes, customer behavior, shifts in supply and demand and

other economic assumptions. These estimates are reviewed at least

annually and downward adjustments, if necessary, are charged to

non-interest expense in the periods in which they become known.

Pension Plan As summarized in Note 18, TCF provides pension

benefits to eligible employees in the TCF Cash Balance Pension Plan.

In accordance with Statement of Financial Accounting Standards

(“SFAS”) No. 87 “Employers’ Accounting for Pensions,” the Company

does not consolidate the assets and liabilities associated with the

pension plan.

The measurement of the projected benefit obligation, prepaid

pension asset and annual pension expense involves complex actuarial

valuation methods and the use of actuarial and economic assump-

tions. Due to the long-term nature of the pension plan obligation,

actual results may differ significantly from the actuarial-based

estimates. Differences between estimates and actual experience are

required to be deferred and under certain circumstances amortized

over the future expected working lifetime of plan participants.

As a result, these differences are not recognized when they occur.

TCF closely monitors all assumptions and updates them annually.

OTHER SIGNIFICANT ACCOUNTING POLICIES

Investments Investments are carried at cost, adjusted for amor-

tization of premiums or accretion of discounts, using methods which

approximate a level yield.

Securities Available for Sale Securities available for sale

are carried at fair value with the unrealized holding gains or losses,

net of related deferred income taxes, reported as accumulated

other comprehensive income (loss), which is a separate component

of stockholders’ equity. Cost of securities sold is determined on a

specific identification basis and gains or losses on sales of securities

available for sale are recognized at trade dates. Declines in the

value of securities available for sale that are considered other than

temporary are recorded in noninterest income as a loss on securities

available for sale. Discounts and premiums on securities available

for sale are amortized using methods which approximate a level yield

over the life of the security.

Loans Held for Sale Loans held for sale include residential

mortgage and education loans. Residential mortgage loans held for

sale are carried at the lower of cost or market as adjusted for the

effects of fair value hedges using quoted market prices. See Note 19

for additional information concerning derivative instruments and