TCF Bank 2003 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2003 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

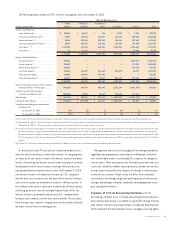

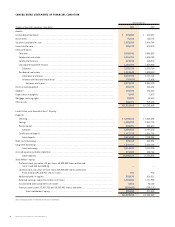

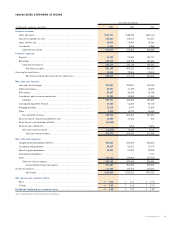

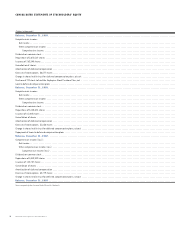

44 TCF Financial Corporation and Subsidiaries

TCF, like most financial institutions, has material interest rate risk

exposure to changes in both short-term and long-term interest

rates as well as variable interest rate indices (e.g., prime).

TCF’s Asset/Liability Committee manages TCF’s interest-rate risk

based on interest rate expectations and other factors. The principal

objective of TCF’s asset/liability management activities is to provide

maximum levels of net interest income while maintaining acceptable

levels of interest rate risk and liquidity risk and facilitating the

funding needs of the Company.

Although the measure is subject to a number of assumptions and

is only one of a number of measurements, management believes that

the interest rate gap (difference between interest-earning assets

and interest-bearing liabilities repricing within a given period) is an

important indication of TCF’s exposure to interest rate risk and the

related volatility of net interest income in a changing interest rate

environment. While the interest rate gap measurement has some

limitations, which include no assumptions regarding future asset or

liability production and the possibility of a static interest rate envi-

ronment which can result in large quarterly changes due to changes

of the above items, interest rate gap represents the net asset or lia-

bility sensitivity at a point in time. In addition to the interest rate gap

analysis, management also utilizes a simulation model to measure

and manage TCF’s interest rate risk, relative to a base case scenario.

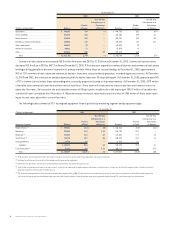

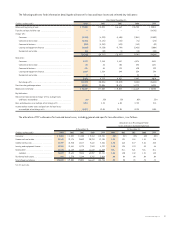

TCF’s one-year interest rate gap was a positive $161.3 million, or

1% of total assets, at December 31, 2003, compared with a positive

$1.1 billion, or 9% of total assets at December 31, 2002. A positive

interest rate gap position exists when the amount of interest-earning

assets maturing or repricing, including assumed prepayments, within

a particular time period exceeds the amount of interest-bearing lia-

bilities maturing or repricing. The decrease in the one-year interest

rate gap is primarily the result of a decrease in fixed-rate mortgage-

backed securities and residential real estate loans of $1.5 billion.

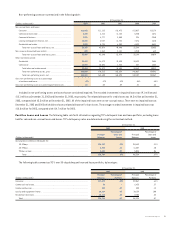

TCF’s balance sheet is generally positioned to benefit from rising

interest rates due to a positive interest rate gap position. TCF would

also likely benefit from an increase in interest rates as this might

signify that economic conditions are improving. The favorable impact

of an increase in interest rates on net interest income would be par-

tially diminished by the fact that at December 31, 2003, $1.7 billion

of variable rate consumer loans and $379 million of variable rate

commercial loans were at their interest rate floors. These loans will

remain at their interest rate floors until interest rates rise above the

floor rates. An increase in the TCF base rate of 50 basis points would

result in the repricing of $1.2 billion of variable rate consumer loans

and $303.9 million of variable rate commercial loans currently at

their floor rates. Additionally, increases in interest rates could have

an adverse impact on TCF’s checking account balances, if customers

transfer some of these funds to higher interest rate deposit products

or other investments and would likely result in an increase in the cost

of interest-bearing deposits. An increase in interest rates would

affect TCF’s fixed-rate/variable-rate product origination mix and

origination volumes and would also likely result in slower fixed-rate

loan prepayments.

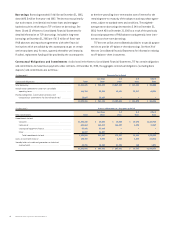

While this positive interest rate gap may compress net interest

income in the short-term, TCF believes this positive interest rate

gap to be warranted because current rates are well below historical

averages, and consequently, there is a greater possibility over time

of higher interest rates versus lower interest rates. However, if interest

rates remain at current levels or fall further, TCF could continue to

experience an increase in prepayments of residential loans, mortgage-

backed securities and fixed-rate consumer and commercial real

estate loans and may continue to experience further compression

of its net interest income.

The one-year interest rate gap could be significantly affected by

external factors such as prepayment rates other than those assumed,

early withdrawals of deposits, changes in the correlation of various

interest-bearing instruments, competition, a general rise or decline

in interest rates, and the possibility that TCF’s counterparties will

exercise their option to call certain of TCF’s longer-term callable

borrowings. Decisions by management to purchase or sell assets

or to retire debt could change the maturity/repricing and spread

relationships. In addition, TCF’s interest-rate risk may increase

during periods of rising interest rates due to slower prepayments

on fixed-rate loans and mortgage-backed securities. TCF estimates

that a 100 basis point increase in interest rates would slow pre-

payments on the $2.7 billion of mortgage-backed securities and

residential real estate loans at December 31, 2003 by approximately

$328.8 million, or 49%. A slowing in prepayments would increase the

estimated life of the mortgage-backed securities and residential

real estate loan portfolios and may adversely impact net interest

income or net interest margin in the future.