Redbox 2006 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2006 Redbox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

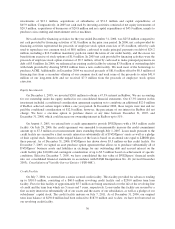

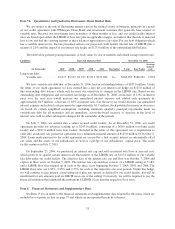

Item 7A. Quantitative and Qualitative Disclosures About Market Risk.

We are subject to the risk of fluctuating interest rates in the normal course of business, primarily as a result

of our credit agreement with JPMorgan Chase Bank and investment activities that generally bear interest at

variable rates. Because our investments have maturities of three months or less, and our credit facility interest

rates are based upon either the LIBOR or base rate plus an applicable margin, we believe that the risk of material

loss is low and that the carrying amount of these balances approximates fair value. For our debt obligation which

has a variable interest rate, the rate presented reflects our projected credit facility interest rate of LIBOR plus a

margin of 2.0% and the impact of our interest rate hedge on $125.0 million of the outstanding debt balance.

The table below presents principal amounts, at book value, by year of maturity and related average interest rates.

Liabilities Expected Maturity Date December 31, 2006

(in thousands) 2007 2008 2009 2010 2011 Thereafter Total Fair Value

Average

interest

rate

Long-term debt:

Variable rate .......... $1,917 $1,917 $1,917 $1,917 $179,284 $— $186,952 $186,952 7.07%

We have variable-rate debt that, at December 31, 2006, had an outstanding balance of $187.0 million. Under

the terms of our credit agreement, we have entered into a zero net cost interest rate hedge on $125.0 million of

this outstanding debt balance which will decrease our sensitivity to changes in the LIBOR rate. Based on our

outstanding debt obligations and our interest rate hedge as of December 31, 2006, an increase of 1.0% in interest

rates over the next year would increase our annualized interest expense and related cash payments by

approximately $0.9 million; a decrease of 1.0% in interest rates over the next year would decrease our annualized

interest expense and related cash payments by approximately $1.7 million. Such potential increases or decreases

are based on certain simplified assumptions, including minimum quarterly principal repayments made on

variable-rate debt for all maturities and an immediate, across-the-board increase or decrease in the level of

interest rates with no other subsequent changes for the remainder of the periods.

On July 7, 2004, we entered into a senior secured credit facility. As of December 31, 2006, our credit

agreement provides for advances totaling up to $247.0 million, consisting of a $60.0 million revolving credit

facility and a $187.0 million term loan facility. Included in the terms of this agreement was a requirement to

enter into an interest rate protection agreement for a minimum notional amount of $125.0 million by October 6,

2004. Loans made pursuant to the credit agreement are secured by a first security interest in substantially all of

our assets and the assets of our subsidiaries, as well as a pledge of our subsidiaries’ capital stock. The credit

facility matures on July 7, 2011.

On September 23, 2004, we purchased an interest rate cap and sold an interest rate floor at zero net cost,

which protects us against certain interest rate fluctuations of the LIBOR rate on $125.0 million of our variable

rate debt under our credit facility. The effective date of the interest rate cap and floor was October 7, 2004 and

expires in three years on October 9, 2007. The interest rate cap and floor consists of a LIBOR ceiling of 5.18%

and a LIBOR floor that stepped up in each of the three years beginning October 7, 2004, 2005 and 2006. The

LIBOR floor rates are 1.85%, 2.25% and 2.75% for each of the respective one-year periods. Under this hedge,

we will continue to pay interest at prevailing rates plus any spread, as defined by our credit facility, but will be

reimbursed for any amounts paid on LIBOR in excess of the ceiling. Conversely, we will be required to pay the

financial institution that originated the instrument if LIBOR is less than the respective floor rates.

Item 8. Financial Statements and Supplementary Data.

See Item 15 for an index to the financial statements and supplementary data required by this item, which are

included as a separate section on page 37 and which are incorporated herein by reference.

33