Qantas 2007 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2007 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

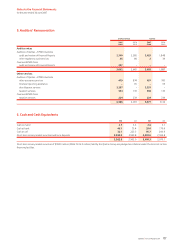

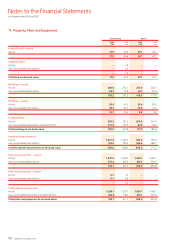

82 Qantas |Annual Report 2007

(Q) Property, Plant and Equipment continued

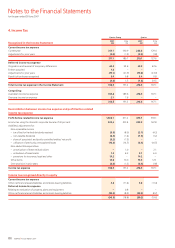

Depreciation and Amortisation

Depreciation and amortisation are provided on a straight-line basis on all

items of property, plant and equipment except for freehold and leasehold

land which are not depreciated or amortised. The depreciation and

amortisation rates of owned assets are calculated so as to allocate the cost

or valuation of an asset, less any estimated residual value, over the asset’s

estimated useful life to the Qantas Group. Assets are depreciated or

amortised from the date of acquisition or, with respect to internally

constructed assets, from the time an asset is completed and available for

use. The costs of improvements to assets are amortised over the remaining

useful life of the asset or the estimated useful life of the improvement,

whichever is the shorter. Assets under finance lease are amortised over the

term of the relevant lease or, where it is likely the Qantas Group will obtain

ownership of the asset, the life of the asset.

The principal asset depreciation and amortisation periods and estimated

residual value percentages are:

Years

Residual

Value (%)

Buildings and leasehold improvements 10 - 50 0

Plant and equipment 3 - 40 0

Aircraft and engines 2.5 - 20 0 - 20

Aircraft spare parts 15 - 20 0 - 20

Depreciation and amortisation rates and residual values are reviewed

annually and reassessed having regard to commercial and technological

developments and the estimated useful life of assets to the Qantas Group

and the long-term fleet plan.

Leased and Hire Purchase Assets

Leased assets under which the Qantas Group assumes substantially

all the risks and benefits of ownership are classified as finance leases.

Other leases are classified as operating leases.

Linked transactions involving the legal form of a lease are accounted

for as one transaction when a series of transactions are negotiated

as one or take place concurrently or in sequence and cannot be

understood economically alone.

Finance leases are capitalised. A lease asset and a lease liability equal

to the present value of the minimum lease payments and guaranteed

residual value are recorded at the inception of the lease. Any gains and

losses arising under sale and leaseback arrangements are deferred

and amortised over the lease term where the sale is not at fair value.

Capitalised leased assets are amortised on a straight-line basis over

the period in which benefits are expected to arise from the use of

those assets. Lease payments are allocated between the reduction

in the principal component of the lease liability and the interest element.

The interest element is charged to the Income Statement over the lease

term so as to produce a constant periodic rate of interest on the remaining

balance of the lease liability.

Fully prepaid leases are classified in the Balance Sheet as hire purchase

assets, to recognise that the financing structures impose certain

obligations, commitments and/or restrictions on the Qantas Group,

which differentiate these aircraft from owned assets.

Leases are deemed to be non-cancellable if significant financial penalties

associated with termination are anticipated.

Operating Leases

Rental payments under operating leases are charged to the Income

Statement on a straight-line basis over the period of the lease.

With respect to any premises rented under long-term operating leases,

which are subject to sub-tenancy agreements, provision is made for any

shortfall between primary payments to the head lessor less any recoveries

from sub-tenants. These provisions are determined on a discounted cash

flow basis, using a rate reflecting the cost of funds.

Manufacturers’ Credits

The Qantas Group receives credits from manufacturers in connection with

the acquisition of certain aircraft and engines. These credits are recorded

as a reduction to the cost of the related aircraft and engines. Where the

aircraft are held under operating leases, the credits are deferred and

reduced from the operating lease rentals on a straight-line basis over the

period of the related lease as deferred credits.

Capital Projects

Capital projects are stated at cost. When the asset is ready for its intended

use, it is capitalised and depreciated.

(R) Intangible Assets

Goodwill

All business combinations since transition to A-IFRS are accounted for

by applying the purchase method. Goodwill represents the difference

between the cost of the acquisition and the fair value of the net

identifiable assets acquired. Goodwill acquired before transition

to A-IFRS is carried at deemed cost utilising transition relief available.

Goodwill is stated at cost less any accumulated impairment losses.

Goodwill is allocated to CGUs and is tested annually for impairment. With

respect to associates and jointly controlled entities, the carrying amount of

goodwill is included in the carrying amount of the investment in the

associate or the jointly controlled entity.

Negative goodwill arising on an acquisition is recognised directly in the

Income Statement.

Airport Landing Slots

Airport landing slots are stated at cost less any accumulated impairment

losses. Airport landing slots are allocated to the Qantas CGU and are not

amortised as they are considered to have an indefinite useful life and are

tested annually for impairment.

Software

Software is stated at cost less accumulated amortisation and impairment

losses. Software development expenditure, including the cost of materials,

direct labour and other direct costs, is only recognised as an asset when

the Qantas Group controls future economic benefits as a result of the

costs incurred, it is probable that those future economic benefits will

eventuate and the costs can be measured reliably. Amortisation is charged

to the Income Statement on a straight-line basis over the estimated useful

life of three to five years.

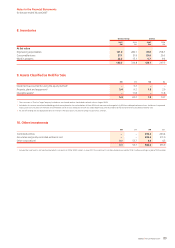

(S) Payables

Liabilities for trade creditors and other amounts are carried at cost.

(T) Frequent Flyer

The Qantas Group receives revenue from the sale to third parties of

rights to have Qantas award points allocated to members of the Qantas

Frequent Flyer Program. This revenue is deferred net of points which it

considers will not be redeemed (breakage) and recognised in the Income

Statement as net passenger revenue when the points are redeemed and

passengers uplifted. Revenue in relation to points which it is considered

will not be redeemed are recognised as net passenger revenue on the sale

of the points.

Notes to the Financial Statements

for the year ended 30 June 2007

1. Statement of Significant Accounting Policies continued