National Grid 2008 Annual Report Download - page 304

Download and view the complete annual report

Please find page 304 of the 2008 National Grid annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

294 -

295

295 -

296

296 -

297

297 -

298

298 -

299

299 -

300

300 -

301

301 -

302

302 -

303

303 -

304

304 -

305

305 -

306

306 -

307

307 -

308

308 -

309

309 -

310

310 -

311

311 -

312

312 -

313

313 -

314

314 -

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

-

544

-

545

-

546

-

547

-

548

-

549

-

550

-

551

-

552

-

553

-

554

-

555

-

556

-

557

-

558

-

559

-

560

-

561

-

562

-

563

-

564

-

565

-

566

-

567

-

568

-

569

-

570

-

571

-

572

-

573

-

574

-

575

-

576

-

577

-

578

-

579

-

580

-

581

-

582

-

583

-

584

-

585

-

586

-

587

-

588

-

589

-

590

-

591

-

592

-

593

-

594

-

595

-

596

-

597

-

598

-

599

-

600

-

601

-

602

-

603

-

604

-

605

-

606

-

607

-

608

-

609

-

610

-

611

-

612

-

613

-

614

-

615

-

616

-

617

-

618

-

619

-

620

-

621

-

622

-

623

-

624

-

625

-

626

-

627

-

628

-

629

-

630

-

631

-

632

-

633

-

634

-

635

-

636

-

637

-

638

-

639

-

640

-

641

-

642

-

643

-

644

-

645

-

646

-

647

-

648

-

649

-

650

-

651

-

652

-

653

-

654

-

655

-

656

-

657

-

658

-

659

-

660

-

661

-

662

-

663

-

664

-

665

-

666

-

667

-

668

-

669

-

670

-

671

-

672

-

673

-

674

-

675

-

676

-

677

-

678

-

679

-

680

-

681

-

682

-

683

-

684

-

685

-

686

-

687

-

688

-

689

-

690

-

691

-

692

-

693

-

694

-

695

-

696

-

697

-

698

-

699

-

700

-

701

-

702

-

703

-

704

-

705

-

706

-

707

-

708

-

709

-

710

-

711

-

712

-

713

-

714

-

715

-

716

-

717

-

718

|

|

BOWNE INTEGRATED TYPESETTING SYSTEM

CRC: 1102

Name: NATIONAL GRID

Date: 17-JUN-2008 03:10:51.35Operator: BNY99999TPhone: (212)924-5500Site: BOWNE OF NEW YORK

Y59930.SUB, DocName: EX-2.B.6.1, Doc: 6, Page: 98

Description: EXH 2(B).6.1

0/2702.00.00.00Y59930BNY

[E/O] EDGAR 2 *Y59930/702/2*

BOWNE INTEGRATED TYPESETTING SYSTEM

CRC: 1102

Name: NATIONAL GRID

Date: 17-JUN-2008 03:10:51.35Operator: BNY99999TPhone: (212)924-5500Site: BOWNE OF NEW YORK

Y59930.SUB, DocName: EX-2.B.6.1, Doc: 6, Page: 98

Description: EXH 2(B).6.1

0/2702.00.00.00Y59930BNY

[E/O] EDGAR 2 *Y59930/702/2*

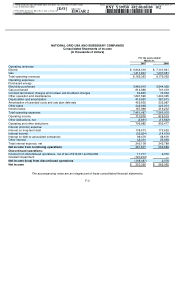

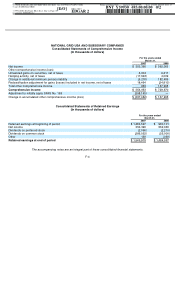

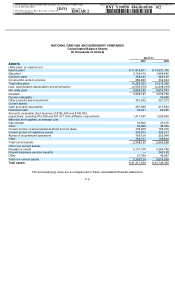

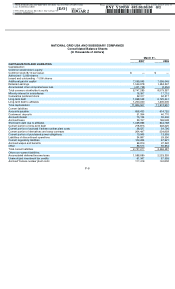

F-13

Deferred investment tax credits are amortized over the useful life of the underl

y

in

g

p

ro

p

ert

y

(

see Note G – “Income Taxes”

)

.

13 Derivatives

The Company accounts for derivative financial instruments under SFAS No. 133, “Accountin

g

for Derivatives and Hed

g

in

g

Activities,” and SFAS No. 149, “Amendment of SFAS No. 133 on Derivative Instruments and Hedging Activities,” as amended.

All derivatives except those qualifyin

g

for the normal purchase/normal sale exception are reco

g

nized on the balance sheet at

their fair value. Fair value is

g

enerally determined usin

g

current quoted market prices. If a contract is desi

g

nated as a cash

flow hed

g

e, the chan

g

e in its market value is

g

enerally deferred as a component of other comprehensive income until the

transaction it is hed

g

in

g

is completed. Conversely, the chan

g

e in the market value of a derivative not desi

g

nated as a cash

flow hed

g

e is deferred as a re

g

ulatory asset or liability. A cash flow hed

g

e is a hed

g

e of a forecasted transaction or the

variability of cash flows to be received or paid related to a reco

g

nized asset or liability. To qualify as a cash flow hed

g

e, the fair

value chan

g

es in the derivative must be expected to offset 80% to 125% of the chan

g

es in fair value or cash flows of the

hedged item. The Company also has purchase power agreements with non-affiliates for the purchase of power and capacity

for resale to its retail customers. These a

g

reements

g

enerally have no notional amounts and do not meet the definition of a

derivative under SFAS No. 133.

14 Comprehensive Income (Loss)

Comprehensive income (loss) is the chan

g

e in the equity of a company, not includin

g

those chan

g

es that result from

shareholder transactions. While the primary component of comprehensive income (loss) is net income, the other components

relate to additional minimum pension liability reco

g

nition, deferred

g

ains and losses associated with hed

g

in

g

activity, and

unrealized gains and losses associated with certain investments held as available for sale (see Note D — “Accumulated Other

Com

p

rehensive Income

(

Loss

)

”

)

.

15 New Accounting Standards

SFAS No. 123R

In December 2004, the FASB issued SFAS No. 123R, “Share-Based Payment.” SFAS No. 123R addresses the accountin

g

for

transactions in which a company receives employee services in exchan

g

e for (a) equity instruments of the company or

(b) liabilities that are based on the fair value of the company’s equity instruments or that may be settled by the issuance of

such equity instruments. SFAS No. 123R also eliminates the ability to account for share-based compensation transactions

using Accounting Principles Board (APB) Opinion No. 25, “Accounting for Stock Issued to Employees,” and requires that such

transactions be accounted for using a fair-value-based method. The adoption of SFAS No. 123R on April 1, 2006 did not have

a material impact on the Company’s results of operations or its financial position.

SFAS No. 154

In May 2005, the FASB issued SFAS No. 154, “Accountin

g

Chan

g

es and Error Corrections, a replacement of APB Opinion

No. 20 and FASB Statement No. 3.” Previously, APB No. 20, “Accounting Changes,” and SFAS No. 3, “Reportin

g

Accountin

g

Changes in Interim Financial Statements,” defined the requirements for the accountin

g

for and the reportin

g

of a chan

g

e in

accounting principle. SFAS No. 154 requires retrospective application to prior periods’ financial statements of chan

g

es in

accounting principle, unless it is impracticable to determine either the period-specific effects or the cumulative effect of the

change. When it is impracticable to determine the period-specific effects of an accountin

g

chan

g

e on one or more individual

prior periods presented, SFAS No. 154 requires that the new accountin

g

principle be applied to the balances of assets and

liabilities as of the be

g

innin

g

of the earliest period for which retrospective application is practicable and that a correspondin

g

adjustment be made to the openin

g

balance of retained earnin

g

s for that period rather than bein

g

reported in an income

statement.