NVIDIA 2011 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2011 NVIDIA annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

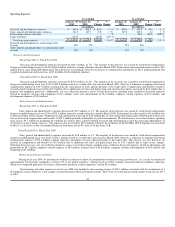

As of January 30, 2011, we had a valuation allowance of $148.0 million related to state and certain foreign deferred tax assets that management

determined are not likely to be realized due, in part, to projections of future taxable income and potential utilization limitations of tax attributes acquired as a

result of stock ownership changes. To the extent realization of the deferred tax assets becomes more-likely-than-not, we would recognize such deferred tax

asset as an income tax benefit during the period the realization occurred.

Our deferred tax assets do not include the excess tax benefit related to stock-based compensation that are a component of our federal and state net

operating loss and research tax credit carryforwards in the amount of $565.2 million as of January 30, 2011. Consistent with prior years, the excess tax benefit

reflected in our net operating loss and research tax credit carryforwards will be accounted for as a credit to stockholders’ equity, if and when realized. In

determining if and when excess tax benefits have been realized, we have elected to utilize the with-and-without approach with respect to such excess tax

benefits. We have also elected to ignore the indirect tax effects of stock-based compensation deductions for financial and accounting reporting purposes, and

specifically to recognize the full effect of the research tax credit in income from continuing operations.

We recognize the benefit from a tax position only if it is more-likely-than-not that the position would be sustained upon audit based solely on the

technical merits of the tax position. Our policy is to include interest and penalties related to unrecognized tax benefits as a component of income tax expense.

Please refer to Note 14 of these Notes to the Consolidated Financial Statements in Part IV, Item 15 of this Form 10-K for additional information.

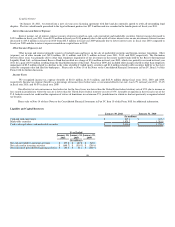

Goodwill

Our impairment review process compares the fair value of the reporting unit in which the goodwill resides to its carrying value. We determined that

our reporting units are equivalent to our operating segments, or components of an operating segment, for the purposes of completing our goodwill impairment

test. We utilize a two-step approach to testing goodwill for impairment. The first step tests for possible impairment by applying a fair value-based test. In

computing fair value of our reporting units, we use estimates of future revenues, costs and cash flows from such units. The second step, if necessary, measures

the amount of such impairment by applying fair value-based tests to individual assets and liabilities. Goodwill is subject to our annual impairment test during

the fourth quarter of our fiscal year, or earlier if indicators of potential impairment exist, using a fair value-based approach.

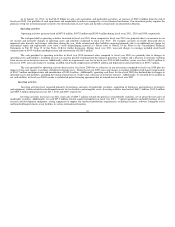

During the fourth quarter of fiscal year 2011, our market capitalization increased over 60% when compared to the same period in fiscal year 2010.

We completed our most recent annual impairment test during the fourth quarter of fiscal year 2011 and concluded that there was no impairment as the fair

value of our reporting units exceeded their carrying value. This assessment was based upon a discounted cash flow analysis, analysis of market comparables,

where appropriate, and analysis of our market capitalization. Determining the number of reporting units and the fair value of a reporting unit requires us to

make judgments and involves the use of significant estimates and assumptions. We also make judgments and assumptions in allocating assets and liabilities to

each of our reporting units. We base our fair value estimates on assumptions we believe to be reasonable but that are unpredictable and inherently uncertain.

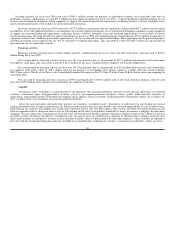

Our estimates of cash flows were based upon, among other things, certain assumptions about expected future operating performance, such as revenue

growth rates, operating margins, risk-adjusted discount rates, and future economic and market conditions. Our estimates of discounted cash flows may differ

from actual cash flows due to, among other things, economic conditions, changes to our business model or changes in operating performance. Additionally,

certain estimates of discounted cash flows involve businesses with limited financial history and developing revenue models, which increases the risk of

differences between the projected and actual performance. The long-term financial forecasts that we utilize represent the best estimate that we have at this

time and we believe that its underlying assumptions are reasonable. Significant differences between our estimates and actual cash flows could materially

affect our future financial results, which could impact our future estimates of the fair value of some or all of our reporting units. Determining the fair value of

our reporting units also requires us to use judgment in the selection of appropriate market comparables, if there are any, and the amount of weight to ascribe to

fair value measurements that are based on the market approach.

Any significant reductions in the actual amount of cash flows realized by our reporting units, reductions in the value of market comparables, or

reductions in our market capitalization could impact future estimates of the fair value of our reporting units. Such events could ultimately result in a charge to

our earnings in future periods due to the potential for a write-down of the goodwill associated with some or all of our reporting units.

40