Mazda 2007 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2007 Mazda annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

|

|

68

of transferring the substitutional portion on the date permission was received from the MHLW for

financial accounting purposes. The Company and the other Domestic Companies did not apply this

transitional provision in the year ended March 31, 2004.

On March 31, 2004, estimated plan assets to be returned to the government were ¥144,871 million. If

the transitional provision had been adopted in the year ended March 31, 2004, based on the estimated

plan assets at March 31, 2004, the effect of the adoption on the consolidated statement of income for

the year ended March 31, 2004 would have been to increase other income by ¥47,517 million.

On July 31, 2005, the Company and the other Domestic Companies obtained approval from the

MHLW to be relieved from the retirement benefit obligation of the substitutional portion which relates

to past employee services and to transfer of the retirement benefit obligation of the substitutional portion

and the related plan assets to the government. On March 28, 2006, the transfer of the plan assets

attributable to the substitutional portion to the government was completed. The effect of the transfer

on the consolidated statement of income for the year ended March 31, 2006 was to increase other

income by ¥59,611 million.

Other than defined benefit plan, defined contribution plan has been adopted. Accrued pension cost

of defined contribution plan was included in consolidated statement of income by ¥1,949 million.

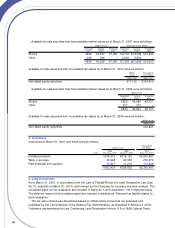

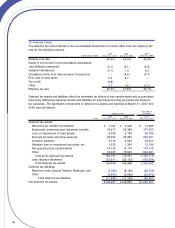

10. Contingent Liabilities

Contingent liabilities at March 31, 2007 were as follows:

Thousands of

Millions of yen U.S. dollars

Discounted trade notes receivable ¥00,348 $002,949

Factoring of receivables with recourse 24,471 207,381

Guarantees of loans and similar agreements 9,096 77,085

Letters of undertaking to provide guarantees for leases for factory facilities 21,339 180,839

11. Equity

The Corporate Law (“the Law”) became effective on May 1, 2006, replacing the Commercial Code

(“the Code”). Under Japanese laws and regulations, the entire amount paid for new shares is required

to be designated as common stock. However, a company may, by a resolution of the Board of

Directors, designate an amount not exceeding one half of the price of the new shares as additional

paid-in capital, which is included in capital surplus.

Under the Law, in cases where dividend distribution of surplus is made, the smaller of an amount

equal to 10% of the dividend or the excess, if any, of 25% of common stock over the total of additional

paid-in capital and legal earnings reserve, must be set aside as additional paid-in capital or legal earnings

reserve. Legal earnings reserve is included in retained earnings in the accompanying consolidated

balance sheets. Under the Code, companies were required to set aside an amount equal to at least

10% of cash dividends and other cash appropriations as legal earnings reserve until the total of legal

earnings reserve and additional paid-in capital could be used to eliminate or reduce a deficit by a

resolution of the shareholders' meeting or could be capitalized by a resolution of the Board of Directors.

Under the Law, both of these appropriations generally require a resolution of the shareholders’meeting.

Additional paid-in capital and legal earnings reserve may not be distributed as dividends. Under the

Code, however, additional paid-in capital and legal earnings reserve could be transferred to retained

earnings by the resolution of the shareholders’meeting as long as the total amount of legal earnings

reserve and additional paid-in capital remained equal to or exceeded 25% of the common stock bal-

ance. Under the Law, all additional paid-in capital and legal earnings reserve may be transferred to