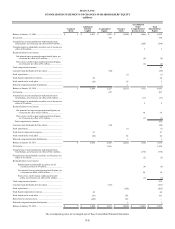

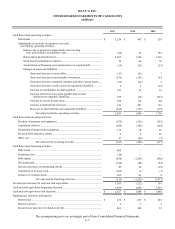

Macy's 2011 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2011 Macy's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

F-10

over the estimated lives of the related depreciable assets. The Company receives contributions from developers and

merchandise vendors to fund building improvement and the construction of vendor shops. Such contributions are netted against

the capital expenditures.

Buildings on leased land and leasehold improvements are amortized over the shorter of their economic lives or the lease

term, beginning on the date the asset is put into use. The Company receives contributions from landlords to fund buildings and

leasehold improvements. Such contributions are recorded as deferred rent and amortized as reductions to lease expense over the

lease term.

The Company recognizes operating lease minimum rentals on a straight-line basis over the lease term. Executory costs

such as real estate taxes and maintenance, and contingent rentals such as those based on a percentage of sales are recognized as

incurred.

The lease term, which includes all renewal periods that are considered to be reasonably assured, begins on the date the

Company has access to the leased property.

The carrying value of long-lived assets is periodically reviewed by the Company whenever events or changes in

circumstances indicate that a potential impairment has occurred. For long-lived assets held for use, a potential impairment has

occurred if projected future undiscounted cash flows are less than the carrying value of the assets. The estimate of cash flows

includes management’s assumptions of cash inflows and outflows directly resulting from the use of those assets in operations.

When a potential impairment has occurred, an impairment write-down is recorded if the carrying value of the long-lived asset

exceeds its fair value. The Company believes its estimated cash flows are sufficient to support the carrying value of its long-

lived assets. If estimated cash flows significantly differ in the future, the Company may be required to record asset impairment

write-downs.

If the Company commits to a plan to dispose of a long-lived asset before the end of its previously estimated useful life,

estimated cash flows are revised accordingly, and the Company may be required to record an asset impairment write-down.

Additionally, related liabilities arise such as severance, contractual obligations and other accruals associated with store closings

from decisions to dispose of assets. The Company estimates these liabilities based on the facts and circumstances in existence

for each restructuring decision. The amounts the Company will ultimately realize or disburse could differ from the amounts

assumed in arriving at the asset impairment and restructuring charge recorded.

The Company classifies certain long-lived assets as held for disposal by sale and ceases depreciation when the particular

criteria for such classification are met, including the probable sale within one year. For long-lived assets to be disposed of by

sale, an impairment charge is recorded if the carrying amount of the asset exceeds its fair value less costs to sell. Such

valuations include estimations of fair values and incremental direct costs to transact a sale.

The carrying value of goodwill and other intangible assets with indefinite lives are reviewed at least annually for possible

impairment in accordance with ASC Subtopic 350-20 “Goodwill.” Goodwill and other intangible assets with indefinite lives

have been assigned to reporting units for purposes of impairment testing. The reporting units are the Company’s retail operating

divisions. Goodwill and other intangible assets with indefinite lives are tested for impairment annually at the end of the fiscal

month of May. The Company estimates fair value based on discounted cash flows. Historically, the goodwill impairment test

involved a two-step process. The first step is a comparison of each reporting unit’s fair value to its carrying value. The reporting

unit’s discounted cash flows require significant management judgment with respect to sales, gross margin and SG&A rates,

capital expenditures and the selection and use of an appropriate discount rate. The projected sales, gross margin and SG&A

expense rate assumptions and capital expenditures are based on the Company’s annual business plan or other forecasted results.

Discount rates reflect market-based estimates of the risks associated with the projected cash flows directly resulting from the

use of those assets in operations. The estimates of fair value of reporting units are based on the best information available as of

the date of the assessment. If the carrying value of a reporting unit exceeds its estimated fair value in the first step, a second

step is performed, in which the reporting unit’s goodwill is written down to its implied fair value. The second step requires the

Company to allocate the fair value of the reporting unit derived in the first step to the fair value of the reporting unit’s net

assets, with any fair value in excess of amounts allocated to such net assets representing the implied fair value of goodwill for

that reporting unit. If the carrying value of an individual indefinite-lived intangible asset exceeds its fair value, such individual

indefinite-lived intangible asset is written down by an amount equal to such excess. Commencing in 2012, the Company will

be allowed to first assess qualitative factors to determine if it is more likely than not that the fair value of a reporting unit is less

than its carrying value and whether it is necessary to perform the two-step goodwill impairment process.

The Company capitalizes purchased and internally developed software and amortizes such costs to expense on a straight-

line basis over two to five years. Capitalized software is included in other assets on the Consolidated Balance Sheets.