Macy's 2011 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2011 Macy's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

18

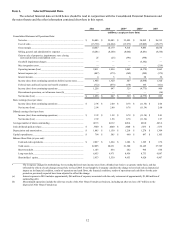

and early spring. The Company purchases a substantial portion of its merchandise inventories and other goods and services

otherwise than through binding contracts. Consequently, the amounts shown as “Other obligations” in the foregoing table do

not reflect the total amounts that the Company would need to spend on goods and services in order to operate its businesses in

the ordinary course.

The Company has not included in the contractual obligations table approximately $134 million of long-term liabilities for

unrecognized tax benefits for various tax positions taken or approximately $60 million of related accrued federal, state and

local interest and penalties. These liabilities may increase or decrease over time as a result of tax examinations, and given the

status of examinations, the Company cannot reliably estimate the period of any cash settlement with the respective taxing

authorities. The Company has included in the contractual obligations table $18 million of liabilities for unrecognized tax

benefits that the Company expects to settle in cash in the next year. The Company has not included in the contractual obligation

table the $389 million Pension Plan liability. The Company's funding policy is to contribute amounts necessary to satisfy

pension funding requirements, including requirements of the Pension Protection Act of 2006, plus such additional amounts

from time to time as are determined to be appropriate to improve the Pension Plan's funded status. The Pension Plan's funded

status is affected by many factors including discount rates and the performance of Pension Plan assets. The Company is

currently planning to make a pension funding contribution of approximately $150 million in 2012.

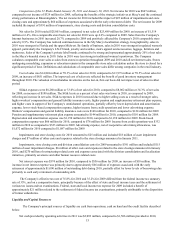

Management believes that, with respect to the Company's current operations, cash on hand and funds from operations,

together with its credit facility and other capital resources, will be sufficient to cover the Company's reasonably foreseeable

working capital, capital expenditure and debt service requirements and other cash requirements in both the near term and over

the longer term. The Company's ability to generate funds from operations may be affected by numerous factors, including

general economic conditions and levels of consumer confidence and demand; however, the Company expects to be able to

manage its working capital levels and capital expenditure amounts so as to maintain sufficient levels of liquidity. To the extent

that the Company's cash balances from time to time exceed amounts that are needed to fund its immediate liquidity

requirements, the Company will consider alternative uses of some or all of such excess cash. Such alternative uses may include,

among others, the redemption or repurchase of debt, equity or other securities through open market purchases, privately

negotiated transactions or otherwise, and the funding of pension related obligations. Depending upon its actual and anticipated

sources and uses of liquidity, conditions in the capital markets and other factors, the Company will from time to time consider

the issuance of debt or other securities, or other possible capital markets transactions, for the purpose of raising capital which

could be used to refinance current indebtedness or for other corporate purposes including the redemption or repurchase of debt,

equity or other securities through open market purchases, privately negotiated transactions or otherwise, and the funding of

pension related obligations.

The Company intends from time to time to consider additional acquisitions of, and investments in, retail businesses and

other complementary assets and companies. Acquisition transactions, if any, are expected to be financed from one or more of

the following sources: cash on hand, cash from operations, borrowings under existing or new credit facilities and the issuance

of long-term debt or other securities, including common stock.

Critical Accounting Policies

Merchandise Inventories

Merchandise inventories are valued at the lower of cost or market using the last-in, first-out (LIFO) retail inventory

method. Under the retail inventory method, inventory is segregated into departments of merchandise having similar

characteristics, and is stated at its current retail selling value. Inventory retail values are converted to a cost basis by applying

specific average cost factors for each merchandise department. Cost factors represent the average cost-to-retail ratio for each

merchandise department based on beginning inventory and the fiscal year purchase activity. The retail inventory method

inherently requires management judgments and contains estimates, such as the amount and timing of permanent markdowns to

clear unproductive or slow-moving inventory, which may impact the ending inventory valuation as well as gross margins.

Permanent markdowns designated for clearance activity are recorded when the utility of the inventory has diminished.

Factors considered in the determination of permanent markdowns include current and anticipated demand, customer

preferences, age of the merchandise and fashion trends. When a decision is made to permanently mark down merchandise, the

resulting gross profit reduction is recognized in the period the markdown is recorded.

The Company receives certain allowances from various vendors in support of the merchandise it purchases for resale.

The Company receives certain allowances as reimbursement for markdowns taken and/or to support the gross margins earned

in connection with the sales of merchandise. These allowances are generally credited to cost of sales at the time the

merchandise is sold in accordance with ASC Subtopic 605-50, “Customer Payments and Incentives.” The Company also

receives advertising allowances from approximately 1,000 of its merchandise vendors pursuant to cooperative advertising

programs, with some vendors participating in multiple programs. These allowances represent reimbursements by vendors of