Kia 2013 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2013 Kia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

|

|

As of the acquisition date, non-controlling interests in the acquiree are measured as the non-controlling interests’ proportionate share

of the acquiree’s identifiable net assets.

The consideration transferred in a business combination shall be measured at fair value, which shall be calculated as the sum of

the acquisition-date fair values of the assets transferred by the acquirer, the liabilities incurred by the acquirer to former owners of

the acquiree and the equity interests issued by the acquirer. However, any portion of the acquirer’s share-based payment awards

exchanged for awards held by the acquiree’s employees that is included in consideration transferred in the business combination shall

be measured in accordance with the method described above rather than at fair value.

Acquisition-related costs are costs the acquirer incurs to effect a business combination. Those costs include finder’s fees; advisory,

legal, accounting, valuation and other professional or consulting fees; general administrative costs, including the costs of maintaining

an internal acquisitions department; and costs of registering and issuing debt and equity securities. Acquisition-related costs, other

than those associated with the issue of debt or equity securities, are expensed in the periods in which the costs are incurred and

the services are received. The costs to issue debt or equity securities are recognized in accordance with K-IFRS No.1032

Financial

Instruments

:

Presentation and

K-IFRS No.1039

Financial Instruments: Recognition and Measurement.

GOODWILL

Goodwill derived from business combinations occurred is as the fair value of the consideration transferred including the

recognized amount of any non-controlling interest in the acquiree, less the net recognized amount of the identifiable assets acquired

and liabilities assumed, all measured as of the acquisition date. When the excess is negative, bargain purchase gain is immediately

recognize in statements of income for the period. Goodwill is subsequently measured at cost less accumulated impairment losses.

Acquisition of non-controlling interests is accounted for intercompany transaction, and related goodwill is not recognized.

(c) Associates and joint ventures

An associate is an entity in which the Company has significant influence, but not control, over the entity’s financial and operating policies.

Significant influence is presumed to exist when the Company holds between 20 and 50 percent of the voting power of another entity.

Joint ventures are those entities over whose activities the Company has joint control, established by contractual agreement, and

require unanimous consent for strategic financial and operating decisions.

The investment in an associate and joint venture is initially recognized at cost and the carrying amount is increased or decreased

to recognize the Company’s share of the profit or loss and changes in equity of the associate and joint venture after the date of

acquisition. Intra-group balances and transactions, and any unrealized income and expenses arising from intra-group transactions, are

eliminated in preparing the consolidated financial statements. Intra-group losses recognized as expense if intra-group losses indicate

an impairment that requires recognition in the consolidated financial statements.

If an associate and joint venture uses accounting policies different from those of the Company for like transactions and events in similar

circumstances, appropriate adjustments are made to its financial statements in applying the equity method.

When the Company’s share of losses exceeds its interest in an equity accounted investee, the carrying amount of that interest,

including any long-term investments, is reduced to nil and the recognition of further losses is discontinued except to the extent that the

Company has an obligation or has to make payments on behalf of the investee for further losses.

(d) Cash and cash equivalents

Cash and cash equivalents comprised of cash on hand, demand deposits and short-term, highly liquid investments that are readily

convertible to known amounts of cash and which are subject to an insignificant risk of changes in value.

(e) Inventories

Inventories are measured at the lower of cost or net realizable value. The cost of inventories is determined based on the specific

identification method for materials-in-transit and moving-average method for all other inventories, and includes expenditure incurred in

acquiring the inventories, production or conversion costs and other costs incurred in bringing them to their existing location and condition.

When inventories are sold, the carrying amount of those inventories is recognized as cost of goods sold in same period as the related

revenue. Net realizable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion

and selling expenses. The amount of any write-down of inventories to net realizable value and all losses of inventories are recognized

the investment continues to be recognized by applying the equity method and there has been no impact on the recognized assets,

liabilities and comprehensive income of the Company.

(vi) K-IFRS No. 1112, ‘Disclosure of Interests in Other Entities’

The Company adopted K-IFRS No. 1112, ‘Disclosure of Interests in Other Entities’ since January 1, 2013. The standard brings together

into a single standard all the disclosure requirements about an entity’s interests in subsidiaries, joint arrangements, associates and

unconsolidated structured entities. The standard requires the disclosure of information about the nature, risks and financial effects of

these interests (see note 8).

(vii) K-IFRS No. 1113, ‘Fair Value Measurement’

The Company adopted K-IFRS No. 1113, ‘Fair Value Measurement’ since January 1, 2013. The standard defines fair value and a single

framework for fair value, and requires disclosures about fair value measurements (see note 30).

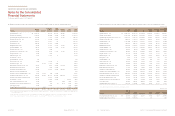

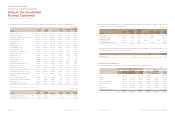

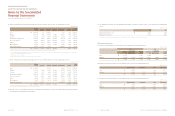

3. Significant Accounting Policies

The significant accounting policies applied by the Company in preparation of its consolidated financial statements are included

below. The accounting policies set out below have been applied consistently to all periods presented in these consolidated financial

statements except those as disclosed in note 2(f).

(a) Basis of consolidation

SUBSIDIARIES

Subsidiaries are entities controlled by the Company. Control exists when the Company has the power to govern the

financial and operating policies of the other entity so as to obtain benefits from its activities. The existence and effect of potential voting

rights that are currently exercisable or convertible are considered when assessing whether the Company controls another entity. The

financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until

the date that control ceases.

If a member of the Company uses accounting policies other than those adopted in the consolidated financial statements for like

transactions and events in similar circumstances, appropriate adjustments are made to its financial statements in preparing the

consolidated financial statements.

INTRA-GROUP TRANSACTIONS

Intra-group balances and transactions, and any unrealized income and expenses arising from intra-

group transactions, are eliminated in preparing the consolidated financial statements. Intra-group losses are recognized as expense if

intra-group losses indicate an impairment that requires recognition in the consolidated financial statements.

NON-CONTROLLING INTERESTS

Non-controlling interests in a subsidiary are accounted for separately from the Company’s

ownership interests in a subsidiary. Each component of net profit or loss and other comprehensive income is attributed to the owners of

the Company and non-controlling interest holders, even when the allocation reduces the non-controlling interest balance below zero.

CHANGES IN THE COMPANY’S OWNERSHIP INTEREST IN A SUBSIDIARY

Changes in the Company’s ownership interest in

a subsidiary that do not result in a loss of control are accounted for as equity transactions with owners in their capacity as owners.

Adjustments to non-controlling interests are based on a proportionate amount of the net assets of the subsidiary. The difference

between the consideration and the adjustments made to non-controlling interest is recognized directly in equity attributable to the

owners of the Company.

(b) Business combination

BUSINESS COMBINATION

A business combination is accounted for by applying the acquisition method, unless it is a combination

involving entities or businesses under common control.

Each identifiable asset and liability is measured at its acquisition-date fair value except for below:

- Only those contingent liabilities assumed in a business combination that are a present obligation and can be measured reliably are recognized

- Deferred tax assets or liabilities are recognized and measured in accordance with K-IFRS No. 1012

Income Taxes

- Employee benefit arrangements are recognized and measured in accordance with K-IFRS No.1019

Employee Benefits

For the years ended December 31, 2013 and 2012