GE 2010 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2010 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

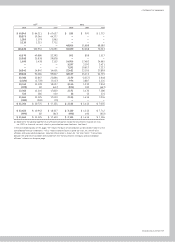

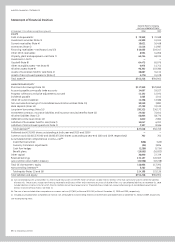

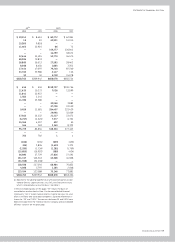

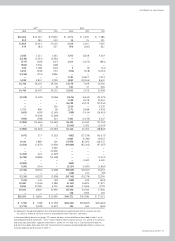

GE 2010 ANNUAL REPORT 77

For short-duration insurance contracts, including accident

and health insurance, we report premiums as earned income over

the terms of the related agreements, generally on a pro-rata

basis. For traditional long-duration insurance contracts including

term, whole life and annuities payable for the life of the annuitant,

we report premiums as earned income when due.

Premiums received on investment contracts (including annui-

ties without significant mortality risk) and universal life contracts

are not reported as revenues but rather as deposit liabilities. We

recognize revenues for charges and assessments on these con-

tracts, mostly for mortality, contract initiation, administration

and surrender. Amounts credited to policyholder accounts are

charged to expense.

Liabilities for traditional long-duration insurance contracts

represent the present value of such benefits less the present

value of future net premiums based on mortality, morbidity,

interest and other assumptions at the time the policies were

issued or acquired. Liabilities for investment contracts and uni-

versal life policies equal the account value, that is, the amount

that accrues to the benefit of the contract or policyholder includ-

ing credited interest and assessments through the financial

statement date.

Liabilities for unpaid claims and estimated claim settlement

expenses represent our best estimate of the ultimate obligations

for reported and incurred-but-not-reported claims and the

related estimated claim settlement expenses. Liabilities for

unpaid claims and estimated claim settlement expenses are

continually reviewed and adjusted through current operations.

Fair Value Measurements

For financial assets and liabilities measured at fair value on a

recurring basis, fair value is the price we would receive to sell

an asset or pay to transfer a liability in an orderly transaction with

a market participant at the measurement date. In the absence of

active markets for the identical assets or liabilities, such measure-

ments involve developing assumptions based on market

observable data and, in the absence of such data, internal informa-

tion that is consistent with what market participants would use in

a hypothetical transaction that occurs at the measurement date.

Observable inputs reflect market data obtained from indepen-

dent sources, while unobservable inputs reflect our market

assumptions. Preference is given to observable inputs. These

two types of inputs create the following fair value hierarchy:

Level 1— Quoted prices for identical instruments in active

markets.

Level 2— Quoted prices for similar instruments in active markets;

quoted prices for identical or similar instruments in

markets that are not active; and model-derived valua-

tions whose inputs are observable or whose significant

value drivers are observable.

Level 3— Significant inputs to the valuation model are

unobservable.

We maintain policies and procedures to value instruments using

the best and most relevant data available. In addition, we have

risk management teams that review valuation, including

Realized gains and losses are accounted for on the specific

identification method. Unrealized gains and losses on investment

securities classified as trading and certain retained interests are

included in earnings.

Inventories

All inventories are stated at the lower of cost or realizable values.

Cost for a significant portion of GE U.S. inventories is determined

on a last-in, first-out (LIFO) basis. Cost of other GE inventories is

determined on a first-in, first-out (FIFO) basis. LIFO was used for

39% of GE inventories at both December 31, 2010 and 2009. GECS

inventories consist of finished products held for sale; cost is

determined on a FIFO basis.

Intangible Assets

We do not amortize goodwill, but test it at least annually for

impairment at the reporting unit level. A reporting unit is the

operating segment, or a business one level below that operating

segment (the component level) if discrete financial information is

prepared and regularly reviewed by segment management.

However, components are aggregated as a single reporting unit

if they have similar economic characteristics. We recognize an

impairment charge if the carrying amount of a reporting unit

exceeds its fair value and the carrying amount of the reporting

unit’s goodwill exceeds the implied fair value of that goodwill. We

use discounted cash flows to establish fair values. When available

and as appropriate, we use comparative market multiples to

corroborate discounted cash flow results. When all or a portion of

a reporting unit is disposed of, goodwill is allocated to the gain or

loss on disposition based on the relative fair values of the busi-

ness disposed of and the portion of the reporting unit that will

be retained.

We amortize the cost of other intangibles over their estimated

useful lives unless such lives are deemed indefinite. The cost of

intangible assets is generally amortized on a straight-line basis

over the asset’s estimated economic life, except that individually

significant customer-related intangible assets are amortized in

relation to total related sales. Amortizable intangible assets are

tested for impairment based on undiscounted cash flows and, if

impaired, written down to fair value based on either discounted

cash flows or appraised values. Intangible assets with indefinite

lives are tested annually for impairment and written down to fair

value as required.

GECS Investment Contracts, Insurance Liabilities and

Insurance Annuity Benefits

Certain entities, which we consolidate, provide guaranteed

investment contracts to states, municipalities and municipal

authorities.

Our insurance activities also include providing insurance and

reinsurance for life and health risks and providing certain annuity

products. Three product groups are provided: traditional insur-

ance contracts, investment contracts and universal life insurance

contracts. Insurance contracts are contracts with significant

mortality and/or morbidity risks, while investment contracts are

contracts without such risks. Universal life insurance contracts

are a particular type of long-duration insurance contract whose

terms are not fixed and guaranteed.