EasyJet 2008 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2008 EasyJet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

easyJet plc

Annual report and accounts 2008

Notes to the

financial statements

continued

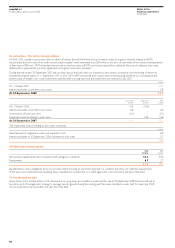

Financial instruments

Financial instruments are recognised when easyJet becomes a party to

the contractual provisions of the relevant instrument and derecognised

when it ceases to be a party to such provisions.

Where market values are not available, the fair value of financial instruments

is calculated by discounting cash flows at prevailing interest rates and by

applying year end exchange rates.

Non-derivative financial assets

Non-derivative financial assets are recorded at amortised cost and include

loan notes, trade receivables, cash and money market deposits. Restricted

cash comprises cash deposits which have restrictions governing their use

and is classified as a current or non-current asset based on the estimated

remaining length of the restriction. Cash and cash equivalents comprise

cash held in bank accounts with no access restrictions and bank or money

market deposits repayable on demand or maturing within three months

of inception.

Impairment losses are recognised on financial assets carried at amortised

cost where there is objective evidence that a loss has been incurred. The

amount of the loss is measured as the difference between the asset’s

carrying amount and the present value of future cash flows, discounted

at the original effective interest rate.

If, subsequently, the amount of the impairment loss decreases, and the

decrease can be related objectively to an event that occurred after the

impairment was recognised, the appropriate portion of the loss is reversed.

Both impairment losses and reversals are recognised in the income

statement as components of net finance income.

Investments in equity instruments are carried at cost where fair value cannot

be reliably measured due to significant variability in the range of reasonable

fair value estimates.

Non-derivative financial liabilities

Non-derivative financial liabilities are initially recorded at fair value of net

proceeds, and subsequently at amortised cost.

Derivative financial instruments

Derivative financial instruments are measured at fair value.

Derivative financial instruments designated as cash flow hedges are used

to mitigate operating and investing transaction exposures to movements

in jet fuel prices and currency exchange rates. Hedge accounting is applied

to these instruments.

Changes in intrinsic fair value are recognised in shareholders’ funds to the

extent that they are effective. All other changes in fair value are recognised

immediately in the income statement. Where the hedged item results in a

non-financial asset or liability the accumulated gains and losses previously

recognised in shareholders’ funds form part of the initial carrying value of

the asset or liability. Otherwise accumulated gains and losses are recognised

in the income statement in the same period in which the hedged items

affect the income statement.

Hedge accounting is discontinued when a hedging instrument is

derecognised (e.g. through expiry or disposal), or no longer qualifies for

hedge accounting. Where the hedged item is a highly probable forecast

transaction, the related gains and losses remain in shareholders’ funds until

the transaction takes place.

When a hedged future transaction is no longer expected to occur, any

related gains and losses previously recognised in shareholders’ funds are

immediately recognised in the income statement.

Tax

Tax expense in the income statement consists of current and deferred tax.

The charge for current tax is based on the results for the year as adjusted

for income that is exempt and expenses that are not deductible using tax

rates that are applicable to the taxable income. Tax is recognised in the

income statement except when it relates to items credited or charged

directly to shareholders’ funds, in which case it is recognised in

shareholders’ funds.

Deferred tax is provided in full on temporary differences relating to

the carrying amount of assets and liabilities where it is probable that

the recovery or settlement will result in an obligation to pay more,

or a right to pay less, tax in the future with the following exceptions:

• where the temporary difference arises from goodwill or from the initial

recognition (other than in a business combination) of other assets

and liabilities in a transaction that affects neither taxable income nor

accounting profit.

• deferred tax arising on investments in subsidiaries, associates and joint

ventures, is not recognised where the Group is able to control the

reversal of the temporary difference and it is probable that the

temporary difference will not reverse in the foreseeable future.

Deferred tax is measured on an undiscounted basis at the tax rates that

are expected to apply in the periods in which recovery of assets and

settlement of liabilities are expected to take place, based on tax rates

or laws enacted or substantively enacted at the balance sheet date.

Deferred tax assets represent amounts recoverable in future periods

in respect of deductible temporary differences, losses and tax credits

carried forwards. Deferred tax assets are recognised to the extent that

it is probable that there will be suitable taxable profits from which they

can be deducted.

Deferred tax liabilities represent the amount of income taxes payable

in future periods in respect of taxable temporary differences.

Deferred tax assets and liabilities are offset when there is a legally

enforceable right to set off current tax assets against current tax liabilities

and it is the intention to settle these on a net basis.

51

OverviewDirectors’ reportReport on Directors’ remunerationFinancial informationOther information