EasyJet 2008 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2008 EasyJet annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

easyJet plc

Annual report and accounts 2008

Notes to the

financial statements

continued

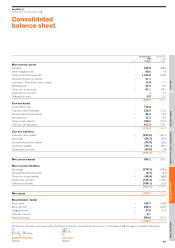

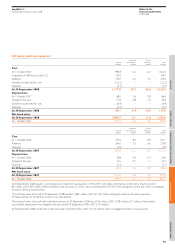

Basis of consolidation

The consolidated financial statements incorporate those of easyJet plc

and its subsidiaries for the years ended 30 September 2007 and 2008,

together with the attributable share of results and reserves of associated

undertakings, adjusted where appropriate to conform with easyJet’s

accounting policies.

A subsidiary is an entity controlled by easyJet. Control exists when easyJet

has the power, directly or indirectly, to govern the financial and operating

policies of an entity so as to benefit from its activities. A minority interest is

the portion of the profit or loss and net assets of a subsidiary attributable

to equity interests that are not owned, directly or indirectly through

subsidiaries, by easyJet.

Associates are those entities in which easyJet has significant influence, but

not control over the financial and operating policies. They are accounted

for using the equity method.

Intragroup balances, transactions and any unrealised gains and losses arising

from intragroup transactions are eliminated in preparing the consolidated

financial statements.

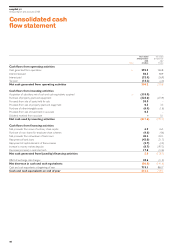

Foreign currencies

The primary economic environment in which a subsidiary operates

determines its functional currency. The functional currency of easyJet plc

is sterling. Certain subsidiaries have operations that are primarily

influenced by a currency other than sterling. Exchange differences arising

on the translation of these foreign operations are taken to reserves until

all or part of the interest is sold, when the relevant portion of the exchange

is recognised in income. Profits and losses of foreign operations are

translated into sterling at average rates of exchange during the year.

Transactions arising in foreign currencies are recorded using the rate

of exchange ruling at the date of the transaction. Monetary assets and

liabilities denominated in foreign currencies are translated into sterling

using the rate of exchange ruling at the balance sheet date and (except

where the asset or liability is designated as a cash flow hedge) the gains

or losses on translation are included in the consolidated income statement.

Non monetary assets and liabilities denominated in foreign currencies are

translated into sterling at foreign exchange rates ruling at the dates the

transactions were effected.

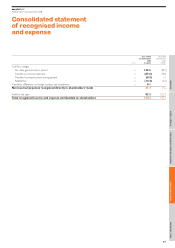

Revenue recognition

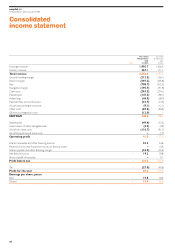

Revenues comprise the invoiced value of airline services, net

of air passenger duty, VAT and discounts, plus ancillary revenue.

Passenger revenue arises from the sale of flight seats and is recognised

when the service is provided. Unearned revenue represents flight seats

sold but not yet flown and is included in trade and other payables until

it is released to the income statement when the service is provided.

Ancillary revenue is generally recognised when the flight to which it relates

departs. Certain types of ancillary revenue are recognised at the time the

benefit of the service provided passes to the customer. Ancillary revenue

in the form of fixed annual fees is recognised evenly throughout the year.

Amounts paid by “no-show” customers are recognised as revenue when

the booked service is provided as such customers are not generally

entitled to change flights or seek refunds once a flight has departed.

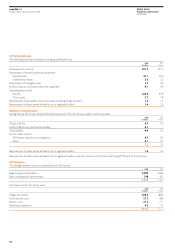

Business combinations

Business combinations are accounted for by applying the purchase method.

The cost of the acquisition is measured at the aggregate of the fair values,

at the date of exchange, of assets given and liabilities incurred or assumed

plus any costs directly attributable to the business combination. The acquiree’s

identifiable assets and liabilities are recognised at their fair values at the

acquisition date. Goodwill arising on acquisition is recognised as an asset

and initially measured at cost, being the excess of the cost of the business

combination over the Group’s interest in the net fair value of the

identifiable assets, liabilities and contingent liabilities recognised.

Goodwill and other intangible assets

Goodwill and landing rights at Gatwick have indefinite expected useful

lives and are tested for impairment annually or where there is any

indication of impairment. They are stated at cost less any accumulated

impairment losses.

Landing rights at Gatwick are considered to have an indefinite useful life

as they will remain available for use for the foreseeable future provided

minimum utilisation requirements are observed.

Other intangible assets are stated at cost less accumulated amortisation,

which is calculated to write off their cost, less estimated residual value, on

a straight-line basis over their expected useful lives. Expected useful lives

are reviewed annually.

Expected useful life

Computer software 3 years

Contractual rights Over the length of the

related contracts

49

OverviewDirectors’ reportReport on Directors’ remunerationFinancial informationOther information