Costco 2010 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2010 Costco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

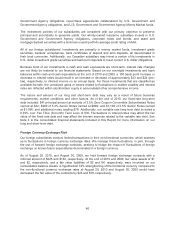

Government Agency obligations, repurchase agreements collateralized by U.S. Government and

Government Agency obligations, and U.S. Government and Government Agency Money Market funds.

The investment policies of our subsidiaries are consistent with our primary objective to preserve

principal and secondarily to generate yields. Our wholly-owned insurance subsidiary invests in U.S.

Government and Government Agency obligations, corporate notes and bonds, and asset and

mortgage-backed securities with a minimum overall portfolio average credit rating of AAA.

All of our foreign subsidiaries’ investments are primarily in money market funds, investment grade

securities, bankers’ acceptances, bank certificates of deposit and term deposits, all denominated in

their local currencies. Additionally, our Canadian subsidiary may invest a portion of its investments in

U.S. dollar investment grade securities and bank term deposits to meet current U.S. dollar obligations.

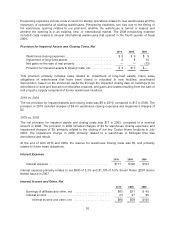

Because most of our investments in cash and cash equivalents are short-term, interest rate changes

are not likely be material to our financial statements. Based on our overnight investments and bank

balances within cash and cash equivalents at the end of 2010 and 2009, a 100 basis point increase or

decrease in interest rates would result in an increase or decrease of approximately $23 and $24 (pre-

tax), respectively, to interest income on an annual basis. For those investments that are classified as

available-for-sale, the unrealized gains or losses related to fluctuations in market volatility and interest

rates are reflected within stockholders’ equity in accumulated other comprehensive income.

The nature and amount of our long and short-term debt may vary as a result of future business

requirements, market conditions and other factors. As of the end of 2010, our fixed-rate long-term

debt included: $41 principal amount at maturity of 3.5% Zero Coupon Convertible Subordinated Notes

carried at $32; $900 of 5.3% Senior Notes carried at $899; and $1,100 of 5.5% Senior Notes carried

at $1,096, and additional notes totaling $78. Additionally, our variable rate long-term debt included a

0.35% over Yen Tibor (6-month) Term Loan of $35. Fluctuations in interest rates may affect the fair

value of the fixed-rate debt and may affect the interest expense related to the variable rate debt. See

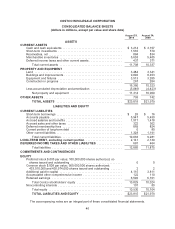

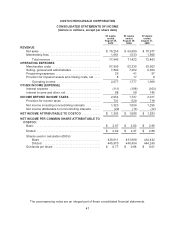

Note 4 to the consolidated financial statements included in this Report for more information on our

long and short-term debt.

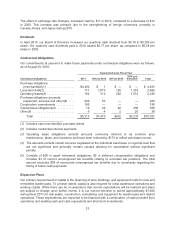

Foreign Currency-Exchange Risk

Our foreign subsidiaries conduct limited transactions in their non-functional currencies, which exposes

us to fluctuations in foreign currency exchange rates. We manage these fluctuations, in part, through

the use of forward foreign exchange contracts, seeking to hedge the impact of fluctuations of foreign

exchange on known future expenditures denominated in a foreign currency.

As of August 29, 2010, and August 30, 2009, we held forward foreign exchange contracts with a

notional amount of $225 and $183, respectively. At the end of 2010 and 2009, fair value assets of $1

and $2, respectively, and a fair value liabilities of $3 and $4, respectively, were recorded on our

consolidated balance sheets. A hypothetical 10% strengthening of the functional currency compared to

the non-functional currency exchange rates at August 29, 2010 and August 30, 2009 would have

decreased the fair value of the contracts by $23 and $18, respectively.

40