Avon 2008 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2008 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92

|

|

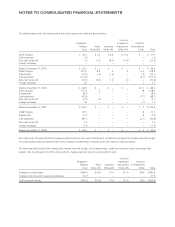

SCHEDULE II

AVON PRODUCTS, INC. AND SUBSIDIARIES

VALUATION AND QUALIFYING ACCOUNTS

Years ended December 31, 2008, 2007 and 2006

Additions

(In millions)

Description

Balance

at

Beginning

of Period

Charged

to Costs

and

Expenses

Charged

to

Revenue Deductions

Balance

at End

of

Period

2008

Allowance for doubtful accounts receivable $109.0 $195.5 $ – $202.5(1) $102.0

Allowance for sales returns 32.1 – 369.3 375.6(2) 25.8

Allowance for inventory obsolescence 216.9 80.8 – 199.5(3) 98.2

Deferred tax asset valuation allowance 278.3 5.8(4) ––

(5) $284.1

2007

Allowance for doubtful accounts receivable $ 91.1 $164.1 $ – $146.2(1) $109.0

Allowance for sales returns 28.0 – 338.1 334.0(2) 32.1

Allowance for inventory obsolescence 125.0 280.6 – 188.7(3) 216.9

Deferred tax asset valuation allowance 234.1 62.9(4) – 18.7(5) 278.3

2006

Allowance for doubtful accounts receivable $ 85.8 $144.7 $ – $139.4(1) $ 91.1

Allowance for sales returns 24.3 – 295.0 291.3(2) 28.0

Allowance for inventory obsolescence 82.4 179.7 – 137.1(3) 125.0

Deferred tax asset valuation allowance 145.2 88.9(4) – – 234.1

(1) Accounts written off, net of recoveries and foreign currency translation adjustment.

(2) Returned product destroyed and foreign currency translation adjustment.

(3) Obsolete inventory destroyed and foreign currency translation adjustment.

(4) Increase in valuation allowance for tax loss carryforward benefits is because it is more likely than not that some or all of the deferred tax assets will not be

utilized in the future.

(5) Release of valuation allowance on deferred tax assets that are more likely than not to be utilized in the future.

A V O N 2008 F-37