Avon 2008 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2008 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

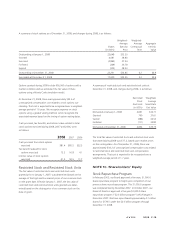

the tax years that remained subject to examination by major tax

jurisdiction for our most significant subsidiaries were as follows:

Jurisdiction Open Years

Brazil 2003 - 2008

China 2004 - 2008

Mexico 2003 - 2008

Poland 2003 - 2008

Russia 2007 - 2008

United States 2006 - 2008

We anticipate that it is reasonably possible that the total amount

of unrecognized tax benefits could decrease in the range of $10

to $15 within the next 12 months due to the closure of tax years

by expiration of the statute of limitations and audit settlements.

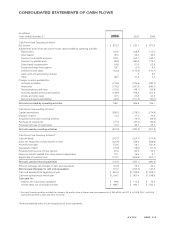

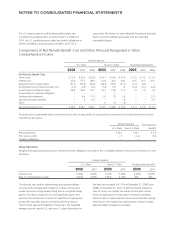

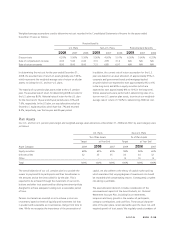

NOTE 7. Financial Instruments and Risk

Management

We operate globally, with manufacturing and distribution facili-

ties in various locations around the world. We may reduce our

exposure to fluctuations in cash flows associated with changes in

interest rates and foreign exchange rates by creating offsetting

positions through the use of derivative financial instruments.

Since we use foreign currency-rate sensitive and interest-rate

sensitive instruments to hedge a certain portion of our existing

and forecasted transactions, we expect that any gain or loss in

value of the hedge instruments generally would be offset by

decreases or increases in the value of the underlying forecasted

transactions.

We do not enter into derivative financial instruments for trading

or speculative purposes, nor are we a party to leveraged deriva-

tives. The master agreements governing our derivative contracts

generally contain standard provisions that could trigger early

termination of the contracts in certain circumstances, including if

we were to merge with another entity and the creditworthiness

of the surviving entity were to be “materially weaker” than that

of Avon prior to the merger.

Accounting Policies

Derivatives are recognized on the balance sheet at their fair

values. When we become a party to a derivative instrument, we

designate the instrument as either a fair value hedge, a cash

flow hedge, a net investment hedge, or a non-hedge. The ac-

counting for changes in fair value (gains or losses) of a derivative

instrument depends on whether it has been designated by Avon

and qualifies as part of a hedging relationship and further, on

the type of hedging relationship.

• Changes in the fair value of a derivative that is designated as a

fair value hedge, along with the loss or gain on the hedged

asset or liability that is attributable to the hedged risk are

recorded in earnings.

• Changes in the fair value of a derivative that is designated as a

cash flow hedge are recorded in accumulated other compre-

hensive loss (“AOCI”) to the extent effective and reclassified

into earnings in the same period or periods during which the

transaction hedged by that derivative also affects earnings.

• Changes in the fair value of a derivative that is designated as a

hedge of a net investment in a foreign operation are recorded

in foreign currency translation adjustments within AOCI to the

extent effective as a hedge.

• Changes in the fair value of a derivative not designated as a

hedging instrument are recognized in earnings in other

expense, net on the Consolidated Statements of Income.

Realized gains and losses on a derivative are reported on the

Consolidated Statements of Cash Flows consistent with the

underlying hedged item.

We assess, both at the hedge’s inception and on an ongoing

basis, whether the derivatives that are used in hedging

transactions are highly effective in offsetting changes in fair

values or cash flows of hedged items. Highly effective means

that cumulative changes in the fair value of the derivative are

between 80% – 125% of the cumulative changes in the fair

value of the hedged item. The ineffective portion of the

derivative’s gain or loss, if any, is recorded in earnings in other

expense, net on the Consolidated Statements of Income. We

include the change in the time value of options in our assess-

ment of hedge effectiveness. When we determine that a deriva-

tive is not highly effective as a hedge, hedge accounting is dis-

continued. When it is probable that a forecasted transaction will

not occur, we discontinue hedge accounting for the affected

portion of the forecasted transaction, and reclassify gains and

losses that were accumulated in AOCI to earnings in other

expense, net on the Consolidated Statements of Income.

Interest Rate Risk

Our long-term, fixed-rate borrowings are subject to interest rate

risk. We use interest rate swaps, which effectively convert the

fixed rate on the debt to a floating interest rate, to manage our

interest rate exposure. At December 31, 2008 and 2007, we

held interest rate swap agreements that effectively converted

approximately 50% and 30% of our outstanding long-term,

fixed-rate borrowings to a variable interest rate based on LIBOR,

respectively. Our total exposure to floating interest rates at

December 31, 2008 and 2007, was approximately 65% and

60%, respectively.

At December 31, 2008 and 2007, we had interest rate swaps

designated as fair value hedges of fixed-rate debt, with unreal-

ized gains (losses) of $83.7 and ($10.8), respectively.

A V O N 2008 F-15