Porsche 2011 Annual Report Download - page 169

Download and view the complete annual report

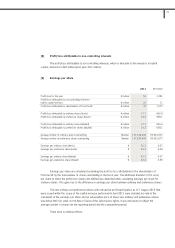

Please find page 169 of the 2011 Porsche annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

|

|

Income from assets for which a group entity has a buy-back obligation cannot be realized until the

assets have definitely left the group. If a fixed repurchase price was agreed when the contract was concluded,

the difference between the selling and repurchase price is recognized as income ratably over the term of the

contract. Prior to that time, the assets are accounted for as inventories.

Revenue from receivables from financial services is realized using the effective interest method.

Revenue is generally recorded separately for each business transaction. If two or more transactions

are linked in such a way that the commercial effect cannot be understood without reference to the series of

transactions as a whole, the criteria for revenue recognition are applied to these transactions as a whole. If, for

example, loans in the financial services sector are issued at below market interest rates to promote sales of

new vehicles, revenue is reduced by the incentive arising from the loan.

Revenue from long-term development contracts is recognized in accordance with the percentage of

completion method.

Interest income and expenses are determined using the effective interest method for financial

instruments measured at amortized cost and interest-bearing securities held for sale.

Dividend income is recognized when the group’s right to receive the payment is established.

Production-related expenses are recognized upon delivery or utilization of the service, while all other

expenses are recognized as an expense as incurred. The same applies for development costs not eligible for

recognition as part of the cost of an asset.

Contingent liabilities

A contingent liability is a possible obligation to third parties that arises from past events and whose

existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events

not wholly within the control of the Porsche SE group. A contingent liability may also be a present obligation

that arises from past events but is not recognized because an outflow of resources is not probable or the

amount of the obligation cannot be measured with sufficient reliability. The amount of contingent liabilities is

only stated in cases where the probability of an outflow of resources is not classified as remote by

management.

Significant accounting judgments and estimates

The preparation of consolidated financial statements requires certain judgments and estimates that

have an effect on recognition, measurement, presentation and disclosure of assets, liabilities, income and

expenses as well as contingent assets and contingent liabilities. These judgments and estimates reflect the

current information available. Key sources of estimations are the parameters influencing the profit or loss from

investments accounted for at equity such as the fair value from purchase price allocations, the useful lives and

amortization or depreciation methods as well as the measurement of provisions at the level of the investees,

the measurement of impairment losses and reversals of impairment losses recognized on the carrying amounts

of associates and joint ventures (see the section “Equity accounting” under “Consolidation principles”), the

measurement of derivative financial instruments (see section 4.2.2 in note [21]), the measurement of

169

3