Office Depot 2007 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2007 Office Depot annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

|

|

29

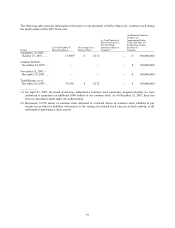

a related $6 million impact recognized in the fourth quarter. A change in foreign country law, which was enacted

during the fourth quarter of 2007, will result in realization of tax benefits from existing net operating loss

carryforwards in that country and, accordingly, we eliminated the 2007 valuation allowance of approximately $9

million on deferred tax assets. Also in 2007, we recognized approximately $4 million of net tax benefits from other

valuation allowance changes and book to tax return adjustments.

We currently expect our operating effective tax rate for 2008 to be about 30%. However, the effective tax rate in

future periods can be affected by variability in our mix of income, the tax rates in various jurisdictions, changes in

the rules related to accounting for income taxes, outcomes from tax audits that regularly are in process and our

assessment of the need for accruals for uncertain tax positions, and therefore may be higher or lower than it has been

over the past three years.

The effective income tax rate increased in 2006, reflecting a greater impact in the prior year from closing certain

worldwide tax audits and adjusted provisions for uncertain tax positions and a shift in mix of income from higher to

lower tax jurisdictions. During 2005, we also adjusted certain valuation allowances based on our current assessment

of realization of the related deferred tax assets. This decrease was partially offset by additional tax expense from

completing our plans to repatriate additional foreign earnings under the provisions of the American Jobs Creation

Act.

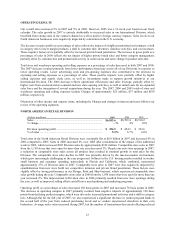

LIQUIDITY AND CAPITAL RESOURCES

Liquidity

At December 29, 2007, we had approximately $223 million in cash and equivalents and another $689 million

available under our revolving credit facility. We anticipate opening 75 new stores in 2008, and we expect to remodel

substantially all remaining stores over the next few years. We will also continue to make supply chain network

improvements.

Our primary needs for cash include working capital for operations, capital expenditures for new stores, store

remodels, information technology projects and supply chain costs, and funds to service our debt obligations and

make acquisitions. We continually review our financing options. Although we currently anticipate that we will fund

our 2008 operations, expansion and other activities through cash on hand, funds generated from operations, property

and equipment leases and funds available under our existing credit facilities, we may consider alternative financing

as appropriate for market conditions.

We hold cash throughout our service areas, but we principally manage our cash through regional headquarters in

North America and Europe. We may move cash between those regions from time to time through short-term

transactions and have used these cash transfers at the end of fiscal quarterly periods to pay down borrowings

outstanding under our credit facilities. Although such transfers and debt repayments took place at the end of 2006

and each of the first three quarters of 2007, we completed a non-taxable distribution to the U.S. in the amount of

$220 million during the fourth quarter of the year, thereby permanently repatriating this cash. Additional

distributions, including distributions of foreign earnings or changes in long-term arrangements could result in

significant additional U.S. tax payments and income tax expense. Currently, there are no plans to change our

expectation of foreign earnings reinvestment or the long-term nature of our intercompany arrangements.

In May 2007, we amended and extended our Revolving Credit Facility (the “Agreement”). The Agreement provides

for multi-currency borrowings of up to $1 billion which, upon approval of the lenders, may be increased to $1.25

billion. The Agreement has a sub-limit of up to $350 million for standby and trade letters of credit issuances.

Amounts may be borrowed, repaid and reborrowed through May 25, 2012. Borrowings under this Agreement will

bear interest at either (a) the base rate, described in the Agreement as a fluctuating rate equal to the lead bank’s base

rate, (b) the Eurodollar rate, described in the Agreement as a periodic fixed rate equal to the London Interbank

Offering Rate (“LIBOR”) plus a percentage spread based on our credit rating and fixed charge coverage ratio, or (c)

the rate set through a bid process. The effective interest rate on yen borrowings was 1.4625% and other borrowings

was 5.275% at the end of 2007. At December 29, 2007, we had approximately $689 million of available credit under

our revolving credit facility that includes coverage of $76 million from outstanding letters of credit. We had an

additional $57 million of letters of credit outstanding under separate agreements.