HSBC 2015 Annual Report Download - page 477

Download and view the complete annual report

Please find page 477 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

467 -

468

468 -

469

469 -

470

470 -

471

471 -

472

472 -

473

473 -

474

474 -

475

475 -

476

476 -

477

477 -

478

478 -

479

479 -

480

480 -

481

481 -

482

482 -

483

483 -

484

484 -

485

485 -

486

486 -

487

487 -

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

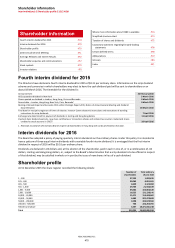

HSBC HOLDINGS PLC

475

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

Taxation of shares and

dividends

Taxation – UK residents

The following is a summary, under current law, of certain UK

tax considerations that are likely to be material to the

ownership and disposition of HSBC Holdings ordinary

shares. The summary does not purport to be a

comprehensive description of all the tax considerations that

may be relevant to a holder of shares. In particular, the

summary deals with shareholders who are resident solely in

the UK for UK tax purposes and only with holders who hold

the shares as investments and who are the beneficial owners

of the shares, and does not address the tax treatment of

certain classes of holders such as dealers in securities.

Holders and prospective purchasers should consult their own

advisers regarding the tax consequences of an investment

in shares in light of their particular circumstances, including

the effect of any national, state or local laws.

Taxation of dividends

Currently no tax is withheld from dividends paid by

HSBC Holdings.

UK resident individuals: periods to 5 April 2016

For periods up to 5 April 2016 dividends are paid with an

associated tax credit which is available for set-off by certain

individual shareholders against any liability they may have

to UK income tax. Currently, the associated tax credit is

equivalent to 10% of the combined cash dividend and tax

credit, i.e. one-ninth of the cash dividend.

For individual shareholders who are resident in the UK for

taxation purposes and liable to UK income tax at the basic

rate, no further UK income tax liability arises on the receipt

of a dividend from HSBC Holdings. Individual shareholders

who are liable to UK income tax at the higher rate or

additional rate are taxed on the combined amount of the

dividend and the tax credit at the dividend upper rate

(currently 32.5%) and the dividend additional rate

(currently 37.5%), respectively. The tax credit is available

for set-off against the dividend upper rate and the dividend

additional rate liability. Individual UK resident shareholders

are not entitled to any tax credit repayment.

UK resident individuals: periods from 6 April 2016

If draft legislation for the Finance Bill 2016 is enacted in its

current form, the dividend tax credit will be abolished from

6 April 2016, to be replaced by a £5,000 annual exemption

for dividend income received by individual shareholders. In

addition, the income tax rates on dividend income outside

the £5,000 annual allowance would change to 7.5% for

basic rate taxpayers, 32.5% for higher rate taxpayers and

38.1% for additional rate taxpayers.

UK resident companies

Shareholders that are within the charge to UK corporation

tax should generally be entitled to an exemption from UK

corporation tax on any dividends received from HSBC

Holdings. However, the exemptions are not comprehensive

and are subject to anti-avoidance rules. Shareholders

within the charge to UK corporation tax are also not

entitled to tax credits on any dividends received (even if

received before 6 April 2016).

If the conditions for exemption are not met or cease to be

satisfied, or a shareholder within the charge to UK

corporation tax elects for an otherwise exempt dividend to

be taxable, the shareholder will be subject to UK

corporation tax on dividends received from HSBC Holdings

at the rate of corporation tax applicable to that

shareholder.

Scrip dividends

Information on the taxation consequences of the HSBC

Holdings scrip dividends offered in lieu of the 2014 fourth

interim dividend and the first, second and third interim

dividends for 2015 was set out in the Secretary’s letters to

shareholders of 20 March, 5 June, 26 August and

4 November 2015. In no case was the difference between

the cash dividend foregone and the market value of the

scrip dividend in excess of 15% of the market value.

Accordingly, for individual shareholders, the amount of the

dividend income chargeable to tax, and, the acquisition

price of the HSBC Holdings ordinary shares for UK capital

gains tax purposes, was the cash dividend foregone.

Taxation of capital gains

The computation of the capital gains tax liability arising on

disposals of shares in HSBC Holdings by shareholders subject

to UK tax on capital gains can be complex, partly depending

on whether, for example, the shares were purchased since

April 1991, acquired in 1991 in exchange for shares in The

Hongkong and Shanghai Banking Corporation Limited, or

acquired subsequent to 1991 in exchange for shares in other

companies.

For capital gains tax purposes, the acquisition cost for

ordinary shares is adjusted to take account of subsequent

rights and capitalisation issues. Any capital gain arising on a

disposal by a UK company may also be adjusted to take

account of indexation allowance. If in doubt, shareholders

are recommended to consult their professional advisers.

Stamp duty and stamp duty reserve tax

Transfers of shares by a written instrument of transfer

generally will be subject to UK stamp duty at the rate of 0.5%

of the consideration paid for the transfer, and such stamp

duty is generally payable by the transferee.

An agreement to transfer shares, or any interest therein,

normally will give rise to a charge to stamp duty reserve tax

at the rate of 0.5% of the consideration. However, provided

an instrument of transfer of the shares is executed pursuant

to the agreement and duly stamped before the date on

which the stamp duty reserve tax becomes payable, under

the current practice of UK HM Revenue and Customs

(‘HMRC’) it will not be necessary to pay the stamp duty

reserve tax, nor to apply for such tax to be cancelled. Stamp

duty reserve tax is generally payable by the transferee.

Paperless transfers of shares within CREST, the UK’s paperless

share transfer system, are liable to stamp duty reserve tax at

the rate of 0.5% of the consideration. In CREST transactions,

the tax is calculated and payment made automatically.