HSBC 2015 Annual Report Download - page 405

Download and view the complete annual report

Please find page 405 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

395 -

396

396 -

397

397 -

398

398 -

399

399 -

400

400 -

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

403

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

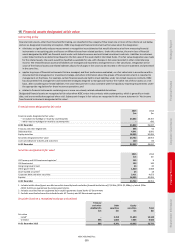

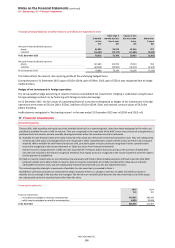

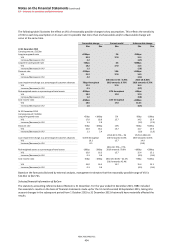

Bank of Communications Co., Limited

HSBC’s investment in BoCom was equity accounted with effect from August 2004. Its significant influence in BoCom was

established as a result of representation on the Board of Directors and, in accordance with the Technical Cooperation and

Exchange Programme, HSBC is assisting in the maintenance of financial and operating policies and a number of staff have been

seconded to assist in this process.

Impairment testing

At 31 December 2015, the fair value of HSBC’s investment in BoCom had been below the carrying amount for approximately

44 months, apart from a short period in 2013 and briefly during the first half of 2015. As a result, the Group performed an

impairment test on the carrying amount of the investment in BoCom. The test confirmed that there was no impairment at

31 December 2015.

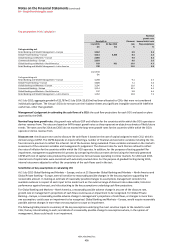

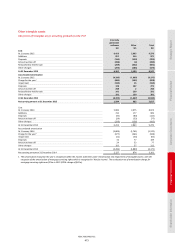

At 31 December 2015 At 31 December 2014

VIU

Carrying

value

Fair

value VIU

Carrying

value

Fair

value

$bn $bn $bn $bn $bn $bn

Bank of Communications Co., Limited 17.0 15.3 9.9 15.7 14.6 13.1

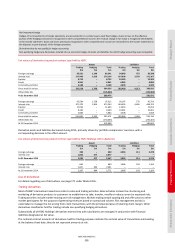

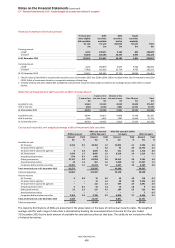

Basis of recoverable amount

The impairment test was performed by comparing the recoverable amount of BoCom, determined by a value in use (‘VIU’)

calculation, with its carrying amount. The VIU calculation uses discounted cash flow projections based on management’s

estimates of earnings. Cash flows beyond the short- to medium-term are then extrapolated in perpetuity using a long-term

growth rate. An imputed capital maintenance charge (‘CMC’) is calculated to reflect the expected regulatory capital

requirements, and is calculated as a deduction from forecast cash flows. The principal inputs to the CMC calculation include

estimates of asset growth, the ratio of risk-weighted assets to total assets, and the expected regulatory capital requirements.

Management judgement is required in estimating the future cash flows of BoCom.

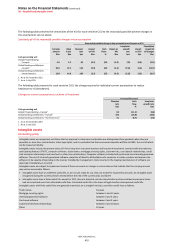

Key assumptions in VIU calculation

Long-term growth rate: the growth rate used was 5% (2014: 5%) for periods after 2018 and does not exceed forecast GDP

growth in mainland China.

Long-term asset growth rate: the growth rate used was 4% (2014: 4%) for periods after 2018 and this is the rate of growth

required for an assumed 5% long-term growth rate in profit.

Discount rate: the discount rate of 13% (2014: 13%) is derived from a range of values obtained by applying a Capital Asset

Pricing Model (‘CAPM’) calculation for BoCom, using market data. Management supplements this by comparing the rates

derived from the CAPM with discount rates available from external sources, and HSBC’s discount rate for evaluating

investments in mainland China. The discount rate used is within the range of 10.1% to 14.2% (2014: 11.4% to 14.2%) indicated

by the CAPM and external sources.

Loan impairment charge as a percentage of customer advances: the ratio used ranges from 0.71% to 0.78% (2014: 0.73% to

1%) in the short- to medium-term and is based on the forecasts disclosed by external analysts. It was assumed that the

long-term ratio will stabilise at a rate of 0.70% (2014: 0.65%) which is slightly higher than the historical rate of 0.65%.

Risk-weighted assets as a percentage of total assets: the ratio used was 67% for all forecast periods (2014: 70% to 72% in the

short- to medium-term and 70% in the long-term). This is consistent with the forecasts disclosed by external analysts.

Cost-income ratio: the ratio used was 41% (2014: ranged from 40.0% to 42.4%) in the short- to medium-term. The ratios were

consistent with the short- to medium-term range forecasts of 40.3% to 40.7% (2014: 37.2% to 44.5%) disclosed by external

analysts.

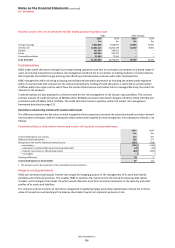

Sensitivity analyses were performed on each key assumption to ascertain the impact of reasonably possible changes in

assumptions. The following change to each key assumption used on its own in the VIU calculation would reduce the headroom

to nil.

Key assumption Changes to key assumption to reduce headroom to nil

• Long-term growth rate

• Long-term asset growth rate

• Discount rate

• Loan impairment charge as a percentage of customer advances

• Risk-weighted assets as a percentage of total assets

• Cost-income ratio

• Decrease by 62 basis points

• Increase by 62 basis points

• Increase by 82 basis points

• Increase by 13 basis points

• Increase by 5.4%

• Increase by 2.8%