HSBC 2015 Annual Report Download - page 349

Download and view the complete annual report

Please find page 349 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

344 -

345

345 -

346

346 -

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

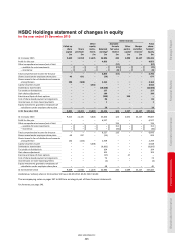

Notes on the Financial Statements

1 – Basis of preparation and significant accounting policies

HSBC HOLDINGS PLC

347

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

1 Basis of preparation and significant accounting policies

(a) Compliance with International Financial Reporting Standards

International Financial Reporting Standards (‘IFRSs’) comprise accounting standards issued or adopted by the International

Accounting Standards Board (‘IASB’) and interpretations issued or adopted by the IFRS Interpretations Committee (‘IFRS IC’).

The consolidated financial statements of HSBC and the separate financial statements of HSBC Holdings have been prepared in

accordance with IFRSs as issued by the IASB and as endorsed by the European Union (‘EU’). EU-endorsed IFRSs could differ

from IFRSs as issued by the IASB if, at any point in time, new or amended IFRSs were not to be endorsed by the EU.

At 31 December 2015, there were no unendorsed standards effective for the year ended 31 December 2015 affecting these

consolidated and separate financial statements, and there was no difference between IFRSs endorsed by the EU and IFRSs

issued by the IASB in terms of their application to HSBC. Accordingly, HSBC’s financial statements for the year ended 31

December 2015 are prepared in accordance with IFRSs as issued by the IASB.

Standards adopted during the year ended 31 December 2015

There were no new standards applied during the year ended 31 December 2015.

During 2015, HSBC adopted a number of interpretations and amendments to standards which had an insignificant effect on

the consolidated financial statements of HSBC and the separate financial statements of HSBC Holdings.

(b) Differences between IFRSs and Hong Kong Financial Reporting Standards

There are no significant differences between IFRSs and Hong Kong Financial Reporting Standards in terms of their application

to HSBC and consequently there would be no significant differences had the financial statements been prepared in accordance

with Hong Kong Financial Reporting Standards. The Notes on the Financial Statements, taken together with the Report of the

Directors, include the aggregate of all disclosures necessary to satisfy IFRSs and Hong Kong reporting requirements.

(c) Future accounting developments

In addition to completing its projects on financial instrument accounting, revenue recognition and leasing, discussed below,

the IASB is working on a project on insurance accounting which could represent significant changes to accounting

requirements in the future.

Minor amendments to IFRSs

The IASB has published a number of minor amendments to IFRSs through the Annual Improvements to IFRSs 2012–2014 cycle

and in a series of stand-alone amendments, one of which has not yet been endorsed for use in the EU. HSBC has not early

applied any of the amendments effective after 31 December 2015 and it expects they will have an insignificant effect, when

applied, on the consolidated financial statements of HSBC and the separate financial statements of HSBC Holdings.

Major new IFRSs

The IASB has published IFRS 9 ‘Financial Instruments’, IFRS 15 ‘Revenue from Contracts with Customers’ and IFRS 16 ‘Leases’.

None of these IFRSs have yet been endorsed for use in the EU.

IFRS 9 ‘Financial Instruments’

In July 2014, the IASB issued IFRS 9 ‘Financial Instruments’, which is the comprehensive standard to replace IAS 39 ‘Financial

Instruments: Recognition and Measurement’, and includes requirements for classification and measurement of financial assets

and liabilities, impairment of financial assets and hedge accounting.

Classification and measurement

The classification and measurement of financial assets will depend on how these are managed (the entity’s business model)

and their contractual cash flow characteristics. These factors determine whether the financial assets are measured at

amortised cost, fair value through other comprehensive income (‘FVOCI’) or fair value through profit or loss (‘FVPL’). In many

instances, the classification and measurement outcomes will be similar to IAS 39, although differences will arise. For example,

under IFRS 9, embedded derivatives are not separated from host financial assets and equity securities are measured at FVPL

or, in limited circumstances, fair value movements will be shown in OCI. The combined effect of the application of the business

model and the contractual cash flow characteristics tests may result in some differences in the population of financial assets

measured at amortised cost or fair value compared with IAS 39. The classification of financial liabilities is essentially unchanged.

For certain liabilities measured at fair value, gains or losses relating to changes in the entity’s own credit risk are to be included

in other comprehensive income.

HSBC conducted an assessment of potential classification and measurement changes to financial assets based on the

composition of the balance sheet as at 31 December 2014. This may not be fully representative of the impact as at 1 January

2018 because IFRS 9 requires that business models be assessed based on the facts and circumstances from the date of initial

application. In addition, the contractual terms and conditions of the financial assets assessed as at 31 December 2014 may

not reflect the contractual terms and conditions of HSBC’s financial assets at transition. However, based on the assessment