HSBC 2015 Annual Report Download - page 423

Download and view the complete annual report

Please find page 423 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

422 -

423

423 -

424

424 -

425

425 -

426

426 -

427

427 -

428

428 -

429

429 -

430

430 -

431

431 -

432

432 -

433

433 -

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

421

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

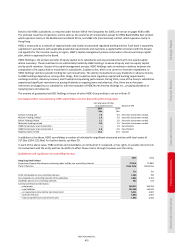

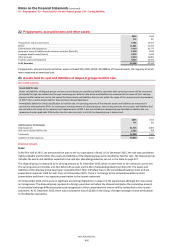

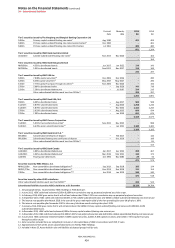

29 Provisions

Accounting policy

Provisions are recognised when it is probable that an outflow of economic benefits will be required to settle a present legal or constructive

obligation which has arisen as a result of past events and for which a reliable estimate can be made.

Critical accounting estimates and judgements

Provisions

Judgement is involved in determining whether a present obligation exists and in estimating the probability, timing and amount of any

outflows. Professional expert advice is taken on the assessment of litigation, property (including onerous contracts) and similar obligations.

Provisions for legal proceedings and regulatory matters typically require a higher degree of judgement than other types of provisions. When

matters are at an early stage, accounting judgements can be difficult because of the high degree of uncertainty associated with determining

whether a present obligation exists, and estimating the probability and amount of any outflows that may arise. As matters progress,

management and legal advisers evaluate on an ongoing basis whether provisions should be recognised, revising previous judgements and

estimates as appropriate. At more advanced stages, it is typically easier to make judgements and estimates around a better defined set of

possible outcomes. However, the amount provisioned can remain very sensitive to the assumptions used. There could be a wide range of

possible outcomes for any pending legal proceedings, investigations or inquiries. As a result, it is often not practicable to quantify a range

of possible outcomes for individual matters. It is also not practicable to meaningfully quantify ranges of potential outcomes in aggregate for

these types of provisions because of the diverse nature and circumstances of such matters and the wide range of uncertainties involved.

Provisions for customer remediation also require significant levels of estimation and judgement. The amounts of provisions recognised

depend on a number of different assumptions, for example, the volume of inbound complaints, the projected period of inbound complaint

volumes, the decay rate of complaint volumes, the population identified as systemically mis-sold and the number of policies per customer

complaint.

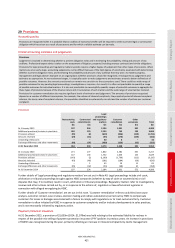

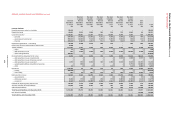

Provisions

Restructuring

costs

Contractual

commitments

Legal

proceedings

and regulatory

matters

Customer

remediation

Other

provisions Total

$m $m $m $m $m $m

At 1 January 2015 197 234 2,184 1,831 552 4,998

Additional provisions/increase in provisions 430 120 2,153 765 138 3,606

Provisions utilised (95) (2) (619) (856) (159) (1,731)

Amounts reversed (29) (15) (95) (170) (133) (442)

Unwinding of discounts

–

–

40 6

–

46

Exchange differences and other movements (40) (97) (489) (236) (63) (925)

At 31 December 2015 463 240 3,174 1,340 335 5,552

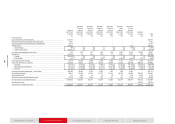

At 1 January 2014 271 177 1,832 2,382 555 5,217

Additional provisions/increase in provisions 147 136 1,752 1,440 154 3,629

Provisions utilised (143) (2) (1,109) (1,769) (112) (3,135)

Amounts reversed (43) (46) (281) (184) (66) (620)

Unwinding of discounts

–

1431011 65

Exchange differences and other movements (35) (32) (53) (48) 10 (158)

At 31 December 2014 197 234 2,184 1,831 552 4,998

Further details of ‘Legal proceedings and regulatory matters’ are set out in Note 40. Legal proceedings include civil court,

arbitration or tribunal proceedings brought against HSBC companies (whether by way of claim or counterclaim) or civil

disputes that may, if not settled, result in court, arbitration or tribunal proceedings. Regulatory matters refer to investigations,

reviews and other actions carried out by, or in response to the actions of, regulators or law enforcement agencies in

connection with alleged wrongdoing by HSBC.

Further details of ‘Customer remediation’ are set out in this note. ‘Customer remediation’ refers to activities (root cause

analysis, customer contact, case reviews, decision making and redress calculations) carried out by HSBC to compensate

customers for losses or damages associated with a failure to comply with regulations or to treat customers fairly. Customer

remediation is often initiated by HSBC in response to customer complaints and/or industry developments in sales practices,

and is not necessarily initiated by regulatory action.

Payment protection insurance

At 31 December 2015, a provision of $1,039m (2014: $1,079m) was held relating to the estimated liability for redress in

respect of the possible mis-selling of payment protection insurance (‘PPI’) policies in previous years. An increase in provisions

of $549m was recognised during the year, primarily reflecting an increase in inbound complaints by claims management