HSBC 2015 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

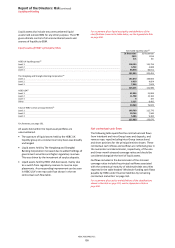

Report of the Directors: Risk (continued)

Liquidity and funding

HSBC HOLDINGS PLC

156

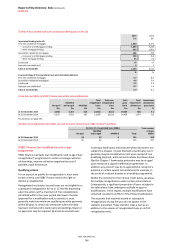

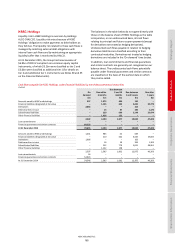

The liquidity position of the Group can also be represented

by the stand-alone ratios of each of our principal operating

entities. The table below displays the individual LCR levels

for the principal HSBC operating entities on an EC LCR

Delegated Regulation basis. The ratios shown for operating

entities in non-EU jurisdictions can vary from their local LCR

measures due to differences in the way non-EU regulators

have implemented the Basel III recommendations.

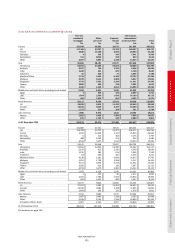

Operating entities’ LCRs

At

31 December

2015

%

HSBC UK liquidity group19 107

The Hongkong and Shanghai Banking Corporation –

Hong Kong Branch20

150

The Hongkong and Shanghai Banking Corporation –

Singapore Branch20

189

HSBC Bank USA21 116

HSBC France22 127

Hang Seng Bank 199

HSBC Canada22 142

HSBC Bank China 183

For footnotes, see page 191.

At 31 December 2015, all the Group’s operating entities

were individually within the risk tolerance level established

by the Board and applicable under the new internal

framework which took effect from 1 January 2016.

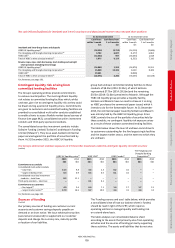

Management of liquidity and funding risk

Forward-looking framework

From 1 January 2016, the Group implemented a new

internal LFRF, using the external LCR and NSFR regulatory

framework as a foundation, but adding extra metrics/limits

and overlays to address the risks that we consider are not

adequately reflected by the external regulatory framework.

The key aspects of the new internal LFRF are:

i. stand-alone management of liquidity and funding by

operating entity;

ii. operating entity classification by inherent liquidity risk

(‘ILR’) categorisation;

iii. minimum operating entity EC LCR requirement

depending on ILR categorisation (EC LCR Delegated

Regulation basis);

iv. minimum operating entity NSFR requirement

depending on ILR categorisation (on the basis of the

Basel 295 publication, pending finalisation of the EC

NSFR delegated regulation);

v. legal entity depositor concentration limit;

vi. operating entity three-month and twelve-month

cumulative rolling term contractual maturity limits

covering deposits from banks, deposits from non-bank

financials and securities issued;

vii. annual individual liquidity adequacy assessment

(‘ILAA’) by operating entity; and

viii. during 2016, we will also introduce a minimum

operating entity LCR requirement by currency.

The new internal LFRF and the risk tolerance (limits) were

approved by the RMM and the Board on the basis of

recommendations made by the Group Risk Committee.

Our ILAA process has been designed to identify risks that

are not reflected in the Group framework and where

additional limits are assessed to be required locally, and to

validate the risk tolerance at the operating entity level.

The decision to create an internal framework modelled

around the external regulatory framework was driven by

the need to ensure that the external and internal

frameworks are directionally aligned and that the Group’s

internal funds transfer pricing framework incentivises the

global businesses within each operating entity to

collectively comply with both the external (regulatory) and

the internal risk tolerance.

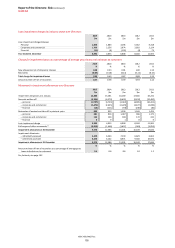

Current framework

The 2015, LFRF employed two key measures to define,

monitor and control the liquidity and funding risk of each

of our operating entities. The ACF ratio was used to

monitor the structural long-term funding position, and the

stressed coverage ratio, incorporating Group-defined stress

scenarios, was used to monitor the resilience to severe

liquidity stresses. Although in place before and during

2015, this framework and its accompanying metrics will

be demised as the new framework outlined above is

implemented.

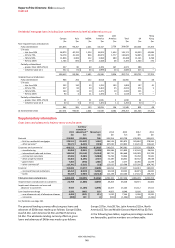

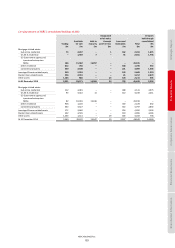

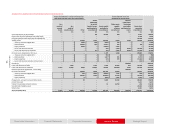

The three principal entities listed in the tables below

represented 65% (2014: 66%) of the Group’s customer

accounts. Including the other principal entities, the

percentage was 88% (2014: 88%).

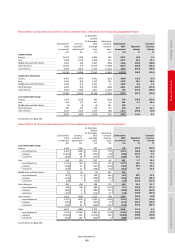

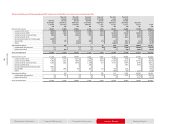

Advances to core funding ratio

The table overleaf shows the extent to which loans and

advances to customers in our principal banking entities

were financed by reliable and stable sources of funding.

ACF limits set for principal operating entities at

31 December 2015 ranged between 80% and 120%.

Core funding represents the core component of customer

deposits and any term professional funding with a residual

contractual maturity beyond one year. Capital is excluded

from our definition of core funding.