HSBC 2015 Annual Report Download - page 205

Download and view the complete annual report

Please find page 205 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

203

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

Additionally, risk may be managed by employing other types of collateral and credit risk enhancements such as second

charges, other liens and unsupported guarantees, but the valuation of such mitigants is less certain and their financial effect

has not been quantified.

Refinance risk

Many types of lending require the repayment of a significant proportion of the principal at maturity. Typically, the mechanism

of repayment for the customer is through the acquisition of a new loan to settle the existing debt. Refinance risk arises where

a customer is unable to repay such term debt on maturity, or to refinance debt at commercial rates. When there is evidence

that this risk may apply to a specific contract, HSBC may need to refinance the loan on concessionary terms that we would not

otherwise have considered, in order to recoup the maximum possible cash flows from the contract and potentially avoid the

customer defaulting on the repayment of principal. When there is sufficient evidence that borrowers, based on their current

financial capabilities, may fail at maturity to repay or refinance their loans, these loans are disclosed as impaired with

recognition of a corresponding impairment allowance where appropriate.

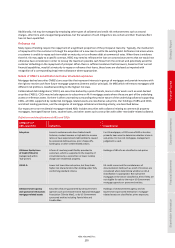

Nature of HSBC’s securitisation and other structured exposures

Mortgage-backed securities (‘MBS’s) are securities that represent interests in groups of mortgages and provide investors with

the right to receive cash from future mortgage payments (interest and/or principal). An MBS which references mortgages with

different risk profiles is classified according to the highest risk class.

Collateralised debt obligations (‘CDO’s) are securities backed by a pool of bonds, loans or other assets such as asset-backed

securities (‘ABS’s). CDOs may include exposure to sub-prime or Alt-A mortgage assets where these are part of the underlying

assets or reference assets. As there is often uncertainty surrounding the precise nature of the underlying collateral supporting

CDOs, all CDOs supported by residential mortgage-related assets are classified as sub-prime. Our holdings of ABSs and CDOs

and direct lending positions, and the categories of mortgage collateral and lending activity, are described below.

Our exposure to non-residential mortgage-related ABSs includes securities with collateral relating to commercial property

mortgages, leveraged finance loans, student loans, and other assets such as securities with other receivable-related collateral.

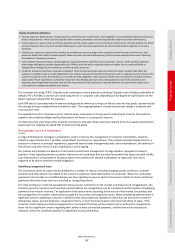

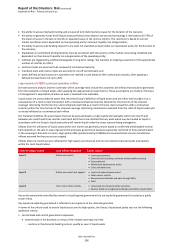

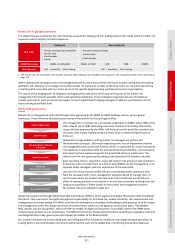

Definitions and classifications of ABSs and CDOs

Categories of

ABSs and CDOs Definition Classification

Sub-prime Loans to customers who have limited credit

histories, modest incomes or high debt-to-income

ratios or have experienced credit problems caused

by occasional delinquencies, prior charge-offs,

bankruptcy or other credit-related actions.

For US mortgages, a FICO score of 620 or less has

primarily been used to determine whether a loan is

sub-prime. For non-US mortgages, management

judgement is used.

US Home Equity Lines

of Credit (‘HELoC’s)

(categorised within

‘Sub-prime’)

A form of revolving credit facility provided to

customers, which is supported in the majority of

circumstances by a second lien or lower ranking

charge over residential property.

Holdings of HELoCs are classified as sub-prime.

US Alt-A Lower risk loans than sub-prime, but they share

higher risk characteristics than lending under fully

conforming standard criteria.

US credit scores and the completeness of

documentation held (such as proof of income), are

considered when determining whether an Alt-A

classification is appropriate. Non sub-prime

mortgages in the US are classified as Alt-A if they are

not eligible for sale to the major US Government

mortgage agencies or sponsored entities.

US Government agency

and sponsored enterprises

mortgage-related assets

Securities that are guaranteed by US Government

agencies such as the Government National Mortgage

Association (‘Ginnie Mae’), or by US Government

sponsored entities including Fannie Mae and

Freddie Mac.

Holdings of US Government agency and US

Government sponsored enterprises’ mortgage-

related assets are classified as prime exposures.