HSBC 2015 Annual Report Download - page 326

Download and view the complete annual report

Please find page 326 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

Report of the independent auditors to the members of HSBC Holdings plc

Audit Report

HSBC HOLDINGS PLC

324

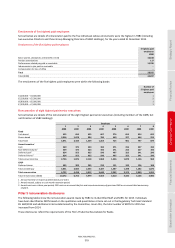

(iii) Audit work executed on individual legal entities

We received opinions from PwC member firms which had been appointed as the external auditors of The Hongkong and

Shanghai Banking Corporation Limited, HSBC Bank plc, HSBC North America Holdings Inc, HSBC Mexico S.A., HSBC Bank

Brasil S.A. – Banco Multiplo, HSBC Vida e Previdência (Brasil) S.A., HSBC Bank Argentina S.A., HSBC Bank Middle East

Limited, HSBC Bank Canada, HSBC Private Banking Holdings (Suisse) S.A. and HSBC Insurance (Bermuda) Limited. I was in

active dialogue throughout the year with the partners responsible for these audits; this included consideration of how

they planned and performed their work. I visited most of these subsidiaries since HSBC’s decision to appoint PwC as

auditor, as well as businesses in a further 7 countries. I also attended meetings with management in each of these key

subsidiaries at the year end.

The audits of these key subsidiaries relied upon work performed by PwC member firms in Germany, France, Turkey,

Malta, China, India, Australia, Qatar, Oman, the UAE and Bahrain. I considered how my subsidiary audit teams instructed

and reviewed the work undertaken in these locations in order to ensure the quality and adequacy of the work.

Collectively, these teams completed procedures covering 81% of total assets, 77% of total operating income and 88% of

profit before tax.

(iv) Audit procedures undertaken at a Group level and on the Parent Company.

I ensured that appropriate further audit work was undertaken for HSBC as the Parent Company. This work included

auditing, for example, the consolidation of the Group’s results, the preparation of the financial statements, certain

disclosures within the Directors remuneration report, litigation provisions and exposures and management’s entity level

and oversight controls relevant to financial reporting.

In aggregate, these four areas provided me with the evidence required to form an opinion on the consolidated financial

statements of HSBC.

The purpose and scope of my audit

An audit has an important role in providing confidence in the financial statements that are provided by companies to their

members. The audit opinion does not provide assurance over any particular number or disclosure, but over the financial

statements taken as a whole. It is the Directors’ responsibility to prepare the financial statements and to be satisfied that they

give a true and fair view. These responsibilities have been recognised on behalf of the Board of Directors on page 322.

The scope of an audit is sometimes not fully understood. I believe that it is important that you understand the scope in order

to understand the assurance that my opinion provides. My responsibility is to undertake my work and express my opinion in

accordance with applicable law and the International Standards on Auditing (UK and Ireland) as issued by the Financial

Reporting Council of the United Kingdom. These standards also require me to comply with the APB’s Ethical Standards for

auditors. A description of the scope of an audit is provided on the Financial Reporting Council’s website at

www.frc.org.uk/auditscopeukprivate; I recommend that you read this description carefully. It is also important that you

understand the inherent limitations of the audit which are disclosed in the description, for example the possibility that an

approach based upon sampling and other audit techniques may not identify all issues.

In order for me to perform my work, I had regard to the concept of materiality. I have determined materiality as follows:

Overall Group materiality $1,050m.

How I determined it 5% of adjusted profit before tax excluding the debt valuation adjustment and non-qualifying

hedges.

Why I believe this is appropriate Given the geographically dispersed nature of HSBC and the diversity of its banking activities, I

believe a standard benchmark of 5% of adjusted profit before tax is an appropriate quantitative

indicator of materiality, although of course an item could also be material for qualitative reasons.

I selected adjusted profit before tax, because as discussed on page 48, management believes it best

reflects the performance of HSBC. I excluded the debt valuation adjustment and non-qualifying

hedges as they are recurring items.