HSBC 2015 Annual Report Download - page 411

Download and view the complete annual report

Please find page 411 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

401 -

402

402 -

403

403 -

404

404 -

405

405 -

406

406 -

407

407 -

408

408 -

409

409 -

410

410 -

411

411 -

412

412 -

413

413 -

414

414 -

415

415 -

416

416 -

417

417 -

418

418 -

419

419 -

420

420 -

421

421 -

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

409

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

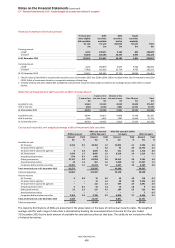

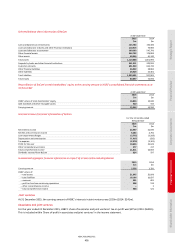

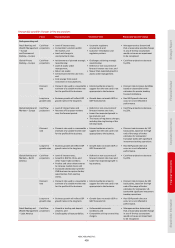

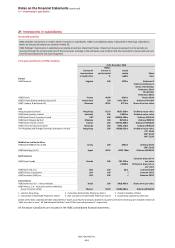

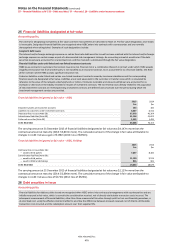

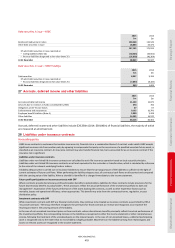

Reasonably possible changes in key assumptions

Input Key assumptions Associated risks Reasonably possible change

Cash-generating unit

Retail Banking and

Wealth Management

– Europe

and Commercial

Banking

–

Europe

Cash flow

projections

• Level of interest rates;

• Competitors’ positions within

the market; and

• Level and change in

unemployment rates.

• Uncertain regulatory

environment; and

• Customer remediation and

regulatory actions.

• Management has determined

that a reasonably possible change

in any of the key assumptions

would not cause an impairment

to be recognised.

Global Private

Banking – Europe

Cash flow

projections

• Achievement of planned strategic

repositioning;

• Level of assets under

management;

• Return on assets;

• Central bank interest rate rises;

and

• Cost savings from recent

investment in new platforms.

• Challenges achieving strategic

repositioning;

• Deferral or non-occurrence of

forecast interest rate rises; and

• Slower than expected growth in

assets under management.

• Cash flow projections decrease

by 20%.

Discount

rate

• Discount rate used is a reasonable

estimate of a suitable market rate

for the profile of the business.

• External evidence arises to

suggest that the rate used is not

appropriate to the business.

• Discount rate increases by 60bps

based on observable broker

estimates for private banking

focused institutions.

Long-term

growth rates

• Business growth will reflect GDP

growth rates in the long term.

• Growth does not match GDP or

GDP forecasts fall.

• Real GDP growth does not

occur or is not reflected in

performance.

Global Banking and

Markets – Europe

Cash flow

projections

• Level of interest rates; and

• Recovery of European markets

over the forecast period.

• Deferral or non-occurrence of

forecast interest rate rises;

• Lower than expected growth in

key markets; and

• The impact of regulatory changes,

including the ring fencing of the

UK retail bank.

• Cash flow projections decrease

by 20%.

Discount

rate

• Discount rate used is a reasonable

estimate of a suitable market rate

for the profile of the business.

• External evidence arises to

suggest that the rate used is not

appropriate to the business.

• Discount rate increases by 110

basis points, based on the high

end of the range of broker

estimates for comparator

European banks with significant

investment banking operations.

Long-term

growth rates

• Business growth will reflect GDP

growth rates in the long term.

• Growth does not match GDP or

GDP forecasts fall.

• Real GDP growth does not

occur or is not reflected in

performance.

Global Banking and

Markets – North

America

Cash flow

projections

• Level of interest rates;

• Growth in NAFTA, China, and

other major trade corridors;

• Product and sales enhancements

to increase market share; and

• Increased collaboration with the

CMB business to capture further

opportunities from existing

clients.

• Deferral or non-occurrence of

forecast interest rate rises; and

• Lower than expected growth in

key markets.

• Cash flow projections decrease

by 20%.

Discount

rate

• Discount rate used is a reasonable

estimate of a suitable market rate

for the profile of the business.

• External evidence arises to

suggest that the rate used is not

appropriate to the business.

• Discount rate increases by 100

basis points, based on the high

end of the range of broker

estimates for comparator US

banks with significant investment

banking operations.

Long-term

growth rates

• Business growth will reflect GDP

growth rates in the long term.

• Growth does not match GDP or

GDP forecasts fall.

• Real GDP growth does not

occur or is not reflected in

performance.

Retail Banking and

Wealth Management

– Latin America

Cash flow

projections

• Growth in lending and deposit

volumes; and

• Credit quality of loan portfolios.

• Unfavourable economic

conditions; and

• Competitive pricing constraining

margins.

• Management has determined

that a reasonably possible change

in any of the key assumptions

would not cause an impairment

to be recognised.