HSBC 2015 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

Report of the Directors: Risk (continued)

Credit risk

HSBC HOLDINGS PLC

146

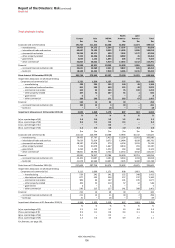

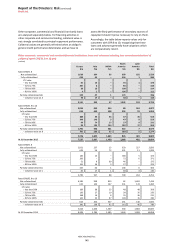

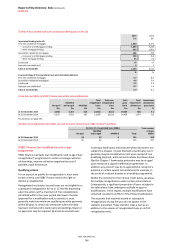

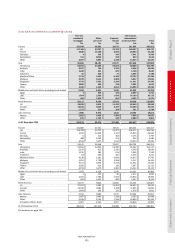

Trends in two months and over contractual delinquency in the US

2015 2014

$m $m

In personal lending in the US

First lien residential mortgages 1,954 3,271

–

Consumer and Mortgage Lending 1,049 2,210

–

other mortgage lending 905 1,061

Second lien residential mortgages 161 216

–

Consumer and Mortgage Lending 106 154

–

other mortgage lending 55 62

Credit card 16 17

Personal non-credit card 3 7

Total at 31 December 2,134 3,511

% %

As a percentage of the equivalent loans and receivables balances

First lien residential mortgages 5.7 8.6

Second lien residential mortgages 4.4 5.0

Credit card 2.3 2.4

Personal non-credit card 0.7 1.4

Total at 31 December 5.4 8.1

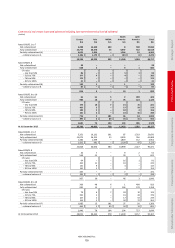

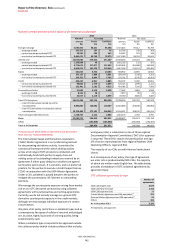

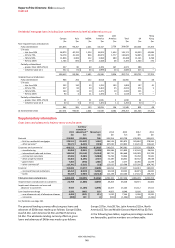

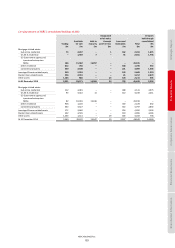

Gross loan portfolio of HSBC Finance real estate secured balances

Re-aged17

Modified

and re-aged Modified

Total

renegotiated

loans

Total non-

renegotiated

loans

Tota l

gross

loans

Tota l

impairment

allowances

Impairment

allowances/

gross loans

$m $m $m $m $m $m $m %

At 31 December 2015 4,858 5,257 519 10,634 8,612 19,246 986 5.1

At 31 December 2014 6,637 6,581 587 13,805 10,619 24,424 1,679 6.9

For footnote, see page 191.

Number of renegotiated real estate secured accounts remaining in HSBC Finance’s portfolio

Number of renegotiated loans (000s) Total number

of loans

(000s)

Re-aged

Modified

and re-aged Modified Total

At 31 December 2015 66 54 6126 240

A

t 31 December 2014 85 64 6 155 297

HSBC Finance loan modifications and re-age

programmes

HSBC Finance maintains loan modification and re-age (‘loan

renegotiation’) programmes in order to manage customer

relationships, improve collection opportunities and, if

possible, avoid foreclosure.

Qualifying criteria

For an account to qualify for renegotiation it must meet

certain criteria, and HSBC Finance retains the right to

decline a renegotiation.

Renegotiated real estate secured loans are not eligible for a

subsequent renegotiation for six or 12 months depending

upon the action, with a maximum of five renegotiations

permitted within a five-year period. Borrowers must be

approved for a modification and, to activate it, must

generally make two minimum qualifying monthly payments

within 60 days. In certain circumstances where the debt

has been restructured in bankruptcy proceedings, fewer or

no payments may be required. Real estate secured loans

involving a bankruptcy and accounts whose borrowers are

subject to a Chapter 13 plan filed with a bankruptcy court

generally may be considered current upon receipt of one

qualifying payment, while accounts whose borrowers have

filed for Chapter 7 bankruptcy protection may be re-aged

upon receipt of a signed reaffirmation agreement. In

addition, any account may be re-aged without receipt of a

payment in certain special circumstances (for example, in

the event of a natural disaster or a hardship programme).

Within the constraints of our Group credit policy, we allow

for multiple renegotiations under certain circumstances.

Consequently, a significant proportion of loans included in

the table above have undergone multiple re-ages or

modifications. In this regard, multiple modifications have

remained consistent at 70% to 75% of total modifications.

The accounts that received second or subsequent

renegotiations during the year do not appear in the

statistics presented. These statistics treat a loan as an

addition to the volume of renegotiated loans on its first

renegotiation only.