HSBC 2015 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

Report of the Directors: Risk (continued)

Credit risk

HSBC HOLDINGS PLC

144

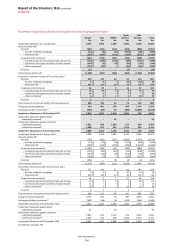

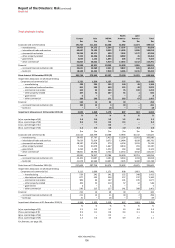

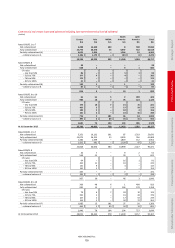

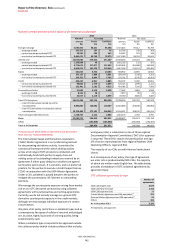

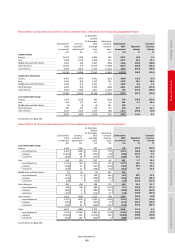

Total personal lending (continued)

Europe Asia MENA

North

America

Latin

America Total

$m $m $m $m $m $m

First lien residential mortgages (D) 131,000 93,147 2,647 55,577 4,153 286,524

Of which:

–

interest only (including offset) 44,163 956

–

276

–

45,395

–

affordability including ARMs 337 5,248

–

16,452

–

22,037

Other personal lending (E) 47,531 36,368 3,924 9,823 9,384 107,030

–

other 34,567 25,695 2,633 4,328 4,846 72,069

–

credit cards 12,959 10,289 897 1,050 3,322 28,517

–

second lien residential mortgages

–

56 2 4,433

–

4,491

–

motor vehicle finance 5 328 392 12 1,216 1,953

Total gross loans at 31 December 2014 (F) 178,531 129,515 6,571 65,400 13,537 393,554

Impairment allowances on personal lending

First lien residential mortgages (d) 306 46 97 1,644 36 2,129

Other personal lending (e) 786 208 97 350 1,030 2,471

–

other 438 87 59 43 672 1,299

–

credit cards 347 119 33 36 298 833

–

second lien residential mortgages

–

–

–

271

–

271

–

motor vehicle finance 125

–

60 68

Total impairment allowances at 31 December 2014 (f) 1,092 254 194 1,994 1,066 4,600

%%%% % %

(d) as a percentage of D 0.2

–

3.7 3.0 0.9 0.7

(e) as a percentage of E 1.7 0.6 2.5 3.6 11.0 2.3

(f) as a percentage of F 0.6 0.2 3.0 3.0 7.9 1.2

On a reported basis, total personal lending was $374bn at

31 December 2015, down from $394bn at the end of 2014.

The reduction of $20bn was mainly due to adverse foreign

exchange movements of $19bn, the reclassification of

$7.6bn of assets of our Brazilian operations as ‘Assets held

for sale’ and the run-off of our CML portfolio in North

America of $5bn during the year. Excluding these factors,

personal lending balances grew by $12bn in 2015. This was

primarily driven by increased mortgage and other lending

in Asia.

Loan impairment allowances reduced by $1.7bn on a

reported basis, mainly due to the Brazilian reclassification

($0.8bn) and the run-off of the US CML portfolio ($0.7bn).

Personal lending loan impairment charges were largely

unchanged at $1.8bn on a reported basis. On a constant

currency basis, they were $0.3bn higher than in 2014,

reflecting increased write-offs in the UAE following a

review of the quality and value of residential mortgage

collateral and the effects of adverse macroeconomic

conditions in Brazil.

Mortgage lending

We offer a wide range of mortgage products designed

to meet customer needs, including capital repayment,

interest-only, affordability and offset mortgages.

Group credit policy prescribes the range of acceptable

residential property LTV thresholds with the maximum

upper limit for new loans set at between 75% and 95%.

Specific LTV thresholds and debt-to-income ratios are

managed at regional and country levels and, although the

parameters must comply with Group policy, strategy and

risk appetite, they differ in the various locations in which

we operate to reflect the local economic and housing

market conditions, regulations, portfolio performance,

pricing and other product features.

Reported gross mortgage lending balances declined by

$12bn. Adverse foreign exchange differences and the

Brazilian reclassification reduced the gross mortgage

lending balances by further $13bn and $2.1bn respectively.

The commentary that follows is on a constant currency

basis, while tables are presented on a reported basis.

Excluding the effect of the Brazilian reclassification and the

US CML run-off portfolio, mortgage lending balances

increased by $7.7bn during the year.

Mortgage lending in Asia, excluding the reclassification to

other personal lending discussed on page 145, grew by

$6.4bn. The increases were primarily attributable to

continued growth in Hong Kong ($4.2bn), mainland China

($1.7bn) and Australia ($1.1bn) as a result of strong

demand and our competitive customer offerings. During

the year, mortgage lending in Singapore fell by $1.1bn

due to a business decision to constrain the level of our

mortgage portfolio, coupled with the effect of a range of

personal lending regulations. The quality of our Asian

mortgage book remained high with negligible defaults and

impairment allowances. The average LTV ratio on new

mortgage lending in Hong Kong was 43% compared with an

estimated 29% for the overall portfolio.

In North America, the US CML portfolio, including second

lien mortgages, declined by $5.2bn in 2015 as we

continued to run it off. The US Premier mortgage portfolio

increased by $1.1bn during 2015 as we focused on growth

in our core portfolios of higher quality mortgages. Our

Canadian mortgage lending balances also grew by $0.8bn

during the year. Collectively assessed impairment

allowances reduced during the year due to continued

improvements in the credit quality of the mortgage

portfolio and continued loan sales.

In Europe, UK mortgage balances were unchanged and our

products remained competitive in the prolonged low

interest rate market environment. In the UK, the credit