HSBC 2015 Annual Report Download - page 246

Download and view the complete annual report

Please find page 246 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

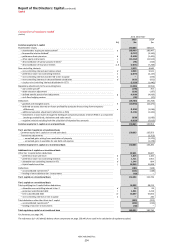

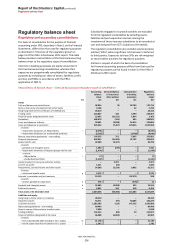

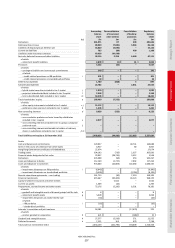

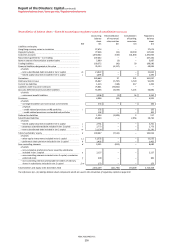

Report of the Directors: Capital (continued)

Appendix to Capital

HSBC HOLDINGS PLC

244

our investment and capital allocation decisions and seek to ensure that returns on investment meet the Group’s management

objectives. Our strategy is to allocate capital to businesses and entities on the basis of their ability to achieve established

RoRWA objectives and their regulatory and economic capital requirements.

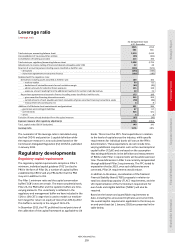

Risk-weighted asset plans

RWA plans form part of the Annual Operating Plan that is approved by the Board. Revised forecasts are submitted to the GMB

on a monthly basis and reported RWAs are monitored against plan.

Our global businesses are set targets in line with the priorities outlined in last June’s strategy update including RWA efficiency

and return on RWAs. Business performance against RWA targets is monitored through regular reporting to the Holding

Company ALCO as well as the GMB. Performance measures are aligned to the Group’s strategic actions. The management of

regulatory capital deductions is also addressed in the RWA monitoring framework through additional notional charges for

these items.

Analysis is undertaken within the RWA monitoring framework to identify the key drivers of movements. Particular attention is

paid to identifying and segmenting items within the day-to-day control of the business and those items that are driven by

changes in risk models or regulatory methodology. Analysis is also undertaken to recognise and report specific actions that are

targeted RWA reduction initiatives.

Capital generation

HSBC Holdings is the primary provider of equity capital to its subsidiaries and also provides them with non-equity capital where

necessary. These investments are substantially funded by HSBC Holdings’ own capital issuance and profit retention. As part of

its capital management process, HSBC Holdings seeks to maintain a prudent balance between the composition of its capital

and its investment in subsidiaries.

Capital measurement and allocation

The PRA supervises HSBC on a consolidated basis and therefore receives information on the capital adequacy of, and sets

capital requirements for, the Group as a whole. Individual banking subsidiaries are directly regulated by their local banking

supervisors, who set and monitor their capital adequacy requirements. Our capital at Group level is calculated under CRD IV

and supplemented by the PRA’s rules to effect the transposition of directive requirements.

Our policy and practice in capital measurement and allocation at Group level is underpinned by the CRD IV rules. In most

jurisdictions, non-banking financial subsidiaries are also subject to the supervision and capital requirements of local regulatory

authorities.

The Basel III framework, similarly to Basel II, is structured around three ‘pillars’: minimum capital requirements, supervisory

review process and market discipline. The CRD IV legislation implemented Basel III in the EU and, in the UK, the ‘PRA Rulebook’

for CRR Firms transposed the various national discretions under the CRD IV legislation into UK requirements. CRDIV also

introduces a number of capital buffers, including the CCB, CCyB, and other systemic buffers such as the G-SII buffer.

Regulatory capital

For regulatory purposes, our capital base is divided into three main categories, namely CET1, additional tier 1 and tier 2,

depending on their characteristics.

• CET1 capital is the highest quality form of capital, comprising shareholders’ equity and related non-controlling interests

(subject to limits). Under CRD IV various capital deductions and regulatory adjustments are made to these items which are

treated differently for the purposes of capital adequacy – these include deductions for goodwill and intangible assets,

deferred tax assets that rely on future profitability, negative amounts resulting from the calculation of expected loss

amounts under IRB, holdings of capital securities of financial sector entities and surplus defined benefit pension fund

assets.

• Additional tier 1 capital comprises eligible non-common equity capital securities and any related share premium; it also

includes qualifying securities issued by subsidiaries subject to certain limits. Holdings of additional tier 1 securities of

financial sector entities are deducted.

• Tier 2 capital comprises eligible capital securities and any related share premium and qualifying tier 2 capital securities

issued by subsidiaries subject to limits. Holdings of tier 2 capital securities of financial sector entities are deducted.

Pillar 1 capital requirements

Pillar 1 is comprised of the capital resources requirements for credit risk, market risk and operational risk. Credit risk includes

counterparty credit risk and securitisation requirements. These requirements are expressed in terms of RWAs.

Credit risk capital requirements

CRD IV applies three approaches of increasing sophistication to the calculation of Pillar 1 credit risk capital requirements. The

most basic, the standardised approach, requires banks to use external credit ratings to determine the risk weightings applied