HSBC 2015 Annual Report Download - page 242

Download and view the complete annual report

Please find page 242 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

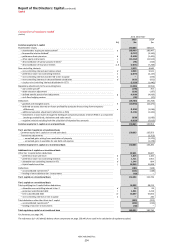

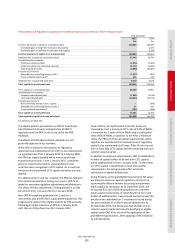

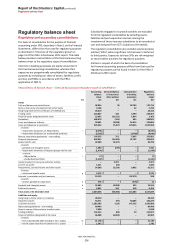

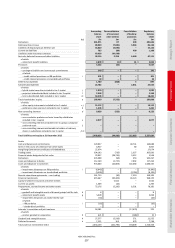

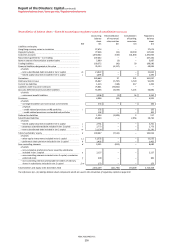

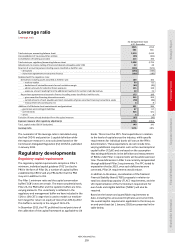

Report of the Directors: Capital (continued)

Regulatory developments

HSBC HOLDINGS PLC

240

Capital requirements framework (end point)

CRD IV capital buffers

CRD IV established a number of capital buffers, to be

met with CET1 capital, broadly aligned with the Basel III

framework. In the UK, with the exception of the CCyB

which applied with immediate effect, CRD IV capital buffers

are being phased in from 1 January 2016.

Automatic restrictions on capital distributions apply if

a bank’s CET1 capital falls below the level of its CRD IV

combined buffer. The CRD IV combined buffer is defined

as the total of the CCB, the CCyB, the global systemically

important institutions (‘G-SII’s) buffer and the systemic risk

buffer (‘SRB’), as these become applicable.

At 31 December 2015, the applicable CCyB rates in force

were 1% set by Norway and Sweden. Relevant credit

exposures located in Norway and Sweden were $2.4bn and

$1.5bn respectively. At 31 December 2015, this resulted in

an immaterial Group institution-specific CCyB requirement.

The Hong Kong Monetary Authority (‘HKMA’) CCyB rate of

0.625% was implemented on 27 January 2016 in respect of

Hong Kong exposures, following communication from the

FPC. The impact of the HKMA CCyB rate on our Group

institution-specific CCyB rate is expected to be 7bps (based

on RWAs at 31 December 2015).

The CCyB rates introduced by Norway and Sweden will

increase to 1.5% from June 2016. In January 2016, the

HKMA also announced that the CCyB rate applied to

exposures in Hong Kong will be increased to 1.25% from

1 January 2017.

In December 2015, the FPC maintained a 0% CCyB rate for

UK exposures. At the same time, the FPC published the

final calibration of the capital framework for UK banks.

Within this, the FPC indicated that going forward it would

apply a more active use of the CCyB and stated that it

intends to publish a revised policy statement on the use of

the CCyB in March 2016. The FPC also noted that it expects

to set a countercyclical buffer rate for UK exposures, in the

region of 1% when risks are judged to be neither subdued

nor elevated. The CCyB rate will be informed by the annual

UK concurrent stress test of major UK banks. If a rate

change is introduced it is expected to come into effect

12 months later.

In December 2015, the PRA confirmed our applicable G-SII

buffer as 2.5%. The G-SII buffer together with the CCB of

2.5%, came into effect on 1 January 2016. These are being

phased in until 2019 in increments of 25% of the end point

buffer requirement. Therefore, as of 1 January 2016, the

requirement for each buffer is 0.625% of RWAs.

Alongside CRD IV requirements, since 2014, the PRA has

expected major UK banks and building societies to meet a

7% CET1 ratio using the CRD IV end point definition. At

1 January 2016, with the introduction of the G-SII buffer

and the CCB, our minimum CET1 capital requirements and

combined buffer requirement taken together amount to

7.1% (based on RWAs at 31 December 2015), effectively

superseding the previous PRA guidance on the CET1 ratio.

In January 2016, the FPC published a consultation on its

proposed framework for the SRB. It is proposed that it will

apply to ring-fenced banks and large building societies and

will be implemented from 1 January 2019. The buffer to be

applied to HSBC's ring-fenced bank has yet to be

determined.

Further details of the aforementioned CRD IV buffers are

set out in the Appendix to Capital on page 246.

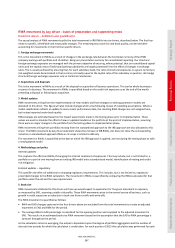

Pillar 2 and the ‘PRA buffer’

The Pillar 2 framework requires banks to hold capital in

respect of risks not captured in the Pillar 1 framework and

to assess risks which banks may become exposed to over a

forward-looking planning horizon. The PRA’s assessment

results in the determination of ICG/Pillar 2A and Pillar 2B,

respectively.

Pillar 2A was previously required to be met by total capital

but, since 1 January 2015, must be met with at least 56%

CET1. Furthermore, the PRA expects firms not to meet the

CRD IV buffers with any CET1 required to meet its ICG.

The Pillar 2A requirement is a point in time assessment

of the amount of capital the PRA considers that a bank

should hold to meet the overall financial adequacy rule.

It is therefore subject to change as part of the PRA’s

supervisory review process. In November 2015, our

Pillar 2A requirement was set at 2.3% of RWAs, of which

1.3% is met by CET1.

In July 2015, the PRA published a final policy statement

PS17/15, setting out amendments to the PRA Rulebook

and Supervisory Statements in relation to the Pillar 2

framework. The revised framework became effective on

1 January 2016. The PRA’s Statement of Policy sets out the

methodologies that it will use to inform its setting of firms’

Pillar 2 capital requirements, including new approaches

for determining Pillar 2 requirements for credit risk,

operational risk, credit concentration risk and pension

obligation risk.

In parallel, in July 2015, the PRA also issued its supervisory

statement SS31/15 in which it introduced a PRA buffer to

replace the capital planning buffer determined under

PRA buffer (illustrative)

Capital

conservation

buffer

Systemic

buffers

(SRB/G-SII)

Macro-prudential tools

(CCyB/sectoral capital

requirements

)

Pillar 2A/ICG

Pillar 1

(

CET1

)(

CET1

)(

CET1

)(

CET1

)(

CET1, AT1

and T2

)

(

CET1,

AT1

and

T2

)

2.5%

2.5%

2.3%

(of which 1.3% CET1)

8%

(of which 4.5% CET1)

0.2%