HSBC 2015 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

147

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

Types of loan renegotiation programmes in HSBC Finance

• A temporary modification is a change to the contractual terms of

a loan that results in HSBC Finance giving up a right to contractual

cash flows over a pre-defined period, typically two years. With a

temporary modification the loan is expected to revert back to the

original contractual terms, including the interest rate charged,

after the modification period. An example is reduced interest

payments.

A substantial number of HSBC Finance modifications involve

interest rate reductions, which lower the amount of interest

income HSBC Finance is contractually entitled to receive in future

periods. Historically, modifications were granted for terms as low

as six months, although more recent modifications have a

minimum term of two years.

• A permanent modification is a change to the contractual terms of

a loan that results in HSBC Finance giving up a right to contractual

cash flows over the life of the loan.

An example is a permanent reduction in the interest rate charged.

HSBC Finance also offers a ‘re-age’ renegotiation programme,

which results in the resetting of an account’s contractual

delinquency status to current (non-delinquent) upon fulfilment

of certain requirements and without additional concessions. The

overdue principal and/or interest is deferred and paid at a later

date. Loan re-ageing enables customers who have been unable

to make a small number of payments to have their loan

delinquency status reset to current so that their credit score is

not affected by the overdue balances. Re-aging may be offered

to customers either without any modification of original loan

terms, or as part of a loan modification transaction.

All renegotiation transactions described above with the

exception of first time re-ages on accounts that are less than 60

days past due are classified as impaired. These remain classified

as impaired until they have demonstrated a history of payment

performance against their original contracted terms for at least

12 months, with the exception of permanent modifications. All

modified loans with terms over two years are considered to be

permanently impaired.

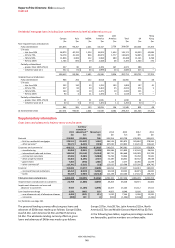

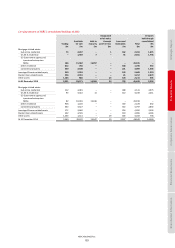

Collateral and other credit enhancements held

(Audited)

The tables below provide a quantification of the value

of fixed charges we hold over specific assets where we

have a history of enforcing, and are able to enforce,

collateral in satisfying a debt in the event of the borrower

failing to meet its contractual obligations, and where

the collateral is cash or can be realised by sale in an

established market. The collateral valuation excludes any

adjustments for obtaining and selling the collateral and, in

particular, loans shown as not collateralised or partially

collateralised may also benefit from other forms of credit

mitigants. UK and Hong Kong are shown, both within

regional figures and separately, due to the size of their

portfolios.

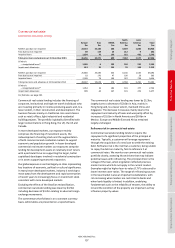

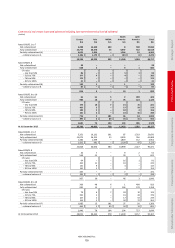

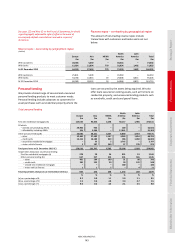

Residential mortgage loans including loan commitments by level of collateral

(Audited)

Europe

Asia MENA

North

America

Latin

America Tota l

UK

Hong

Kong

$m $m $m $m $m $m $m $m

Non-impaired loans and advances

Fully collateralised 128,113 100,102 2,144 41,567 1,869 273,795 122,221 61,784

LTV ratio:

–

less than 50% 70,851 59,212 595 12,369 710 143,737 68,362 42,589

–

51% to 75% 47,933 33,237 985 22,071 903 105,129 45,762 15,961

–

76% to 90% 8,322 6,522 535 5,502 222 21,103 7,584 2,254

–

91% to 100% 1,007 1,131 29 1,625 34 3,826 513 980

Partially collateralised:

–

greater than 100% LTV (A) 540 168 46 1,208 13 1,975 321 97

–

collateral value on A 434 155 37 1,147 11 1,784 221 95

128,653 100,270 2,190 42,775 1,882 275,770 122,542 61,881

Impaired loans and advances

Fully collateralised 1,407 222 44 6,713 109 8,495 1,191 46

LTV ratio:

–

less than 50% 518 105 18 1,247 90 1,978 469 42

–

51% to 75% 619 76 13 2,819 14 3,541 540 3

–

76% to 90% 183 34 81,811 42,040 133 1

–

91% to 100% 87 7 5 836 1936 49

–

Partially collateralised:

–

greater than 100% LTV (B) 178 8 18 628 1833 49

–

–

collateral value on B 160 6 13 547

–

726 36

–

1,585 230 62 7,341 110 9,328 1,240 46

At 31 December 2015 130,238 100,500 2,252 50,116 1,992 285,098 123,782 61,927