HSBC 2015 Annual Report Download - page 198

Download and view the complete annual report

Please find page 198 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

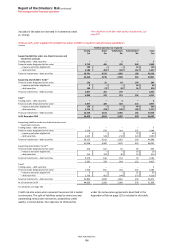

Report of the Directors: Risk (continued)

Appendix to Risk – Policies and practices

HSBC HOLDINGS PLC

196

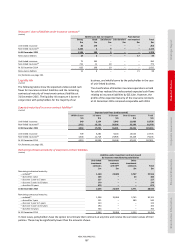

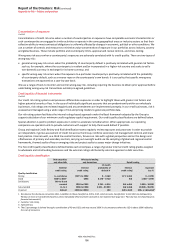

Concentration of exposure

(Audited)

Concentrations of credit risk arise when a number of counterparties or exposures have comparable economic characteristics or

such counterparties are engaged in similar activities or operate in the same geographical areas or industry sectors so that their

collective ability to meet contractual obligations is uniformly affected by changes in economic, political or other conditions. We

use a number of controls and measures to minimise undue concentration of exposure in our portfolios across industry, country

and global business. These include portfolio and counterparty limits, approval and review controls, and stress testing.

Wrong-way risk occurs when a counterparty’s exposures are adversely correlated with its credit quality. There are two types of

wrong-way risk:

• general wrong-way risk occurs when the probability of counterparty default is positively correlated with general risk factors

such as, for example, where the counterparty is resident and/or incorporated in a higher-risk country and seeks to sell a

non-domestic currency in exchange for its home currency; and

• specific wrong-way risk occurs when the exposure to a particular counterparty is positively correlated with the probability

of counterparty default, such as a reverse repo on the counterparty’s own bonds. It is our policy that specific wrong-way

transactions are approved on a case-by-case basis.

We use a range of tools to monitor and control wrong-way risk, including requiring the business to obtain prior approval before

undertaking wrong-way risk transactions outside pre-agreed guidelines.

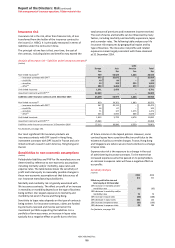

Credit quality of financial instruments

(Audited)

Our credit risk rating systems and processes differentiate exposures in order to highlight those with greater risk factors and

higher potential severity of loss. In the case of individually significant accounts that are predominantly within our wholesale

businesses, risk ratings are reviewed regularly and any amendments are implemented promptly. In our retail businesses, risk is

assessed and managed using a wide range of risk and pricing models to generate portfolio data.

Our risk rating system facilitates the internal ratings-based approach under the Basel framework adopted by the Group to

support calculation of our minimum credit regulatory capital requirement. Our credit quality classifications are defined below.

Special attention is paid to problem exposures in order to accelerate remedial action. When appropriate, our operating

companies use specialist units to provide customers with support to help them avoid default if possible.

Group and regional Credit Review and Risk Identification teams regularly review exposures and processes in order to provide

an independent, rigorous assessment of credit risk across the Group, reinforce secondary risk management controls and share

best practice. Internal audit, as a third line control function, focuses on risks with a global perspective and on the design and

effectiveness of primary and secondary controls, carrying out oversight audits via the sampling of global and regional control

frameworks, themed audits of key or emerging risks and project audits to assess major change initiatives.

The five credit quality classifications defined below each encompass a range of granular internal credit rating grades assigned

to wholesale and retail lending businesses and the external ratings attributed by external agencies to debt securities.

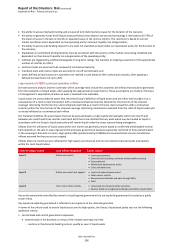

Credit quality classification

Debt securities

and other bills

Wholesale lending

and derivatives Retail lending

External

credit rating

Internal

credit rating

12 month

probability of

default %

Internal

credit rating1

Expected

loss %

Quality classification

Strong A

–

and above CRR21 to CRR2 0

–

0.169 EL31 to EL2 0

–

0.999

Good BBB+ to BBB– CRR3 0.170 – 0.740 EL3 1.000 – 4.999

Satisfactory BB+ to B and

unrated

CRR4 to CRR5 0.741 – 4.914 EL4 to EL5 5.000 – 19.999

Sub-standard B

–

to C CRR6 to CRR8 4.915 – 99.999 EL6 to EL8 20.000

–

99.999

Impaired Default CRR9 to CRR10 100 EL9 to EL10 100+ or defaulted4

1 We observe the disclosure convention that, in addition to those classified as EL9 to EL10, retail accounts classified EL1 to EL8 that are delinquent by

90 days or more are considered impaired, unless individually they have been assessed as not impaired (see page 127, ‘Past due but not impaired gross

financial instruments’).

2 Customer risk rating.

3 Expected loss.

4 The EL percentage is derived through a combination of PD and LGD, and may exceed 100% in circumstances where the LGD is above 100% reflecting

the cost of recoveries.