HSBC 2015 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

HSBC HOLDINGS PLC

133

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

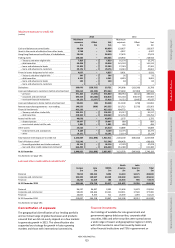

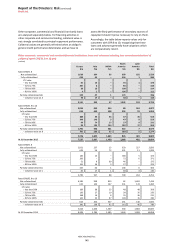

Europe Asia MENA

North

America

Latin

America Total

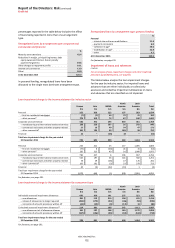

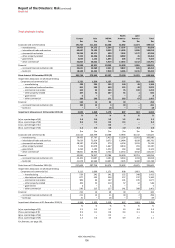

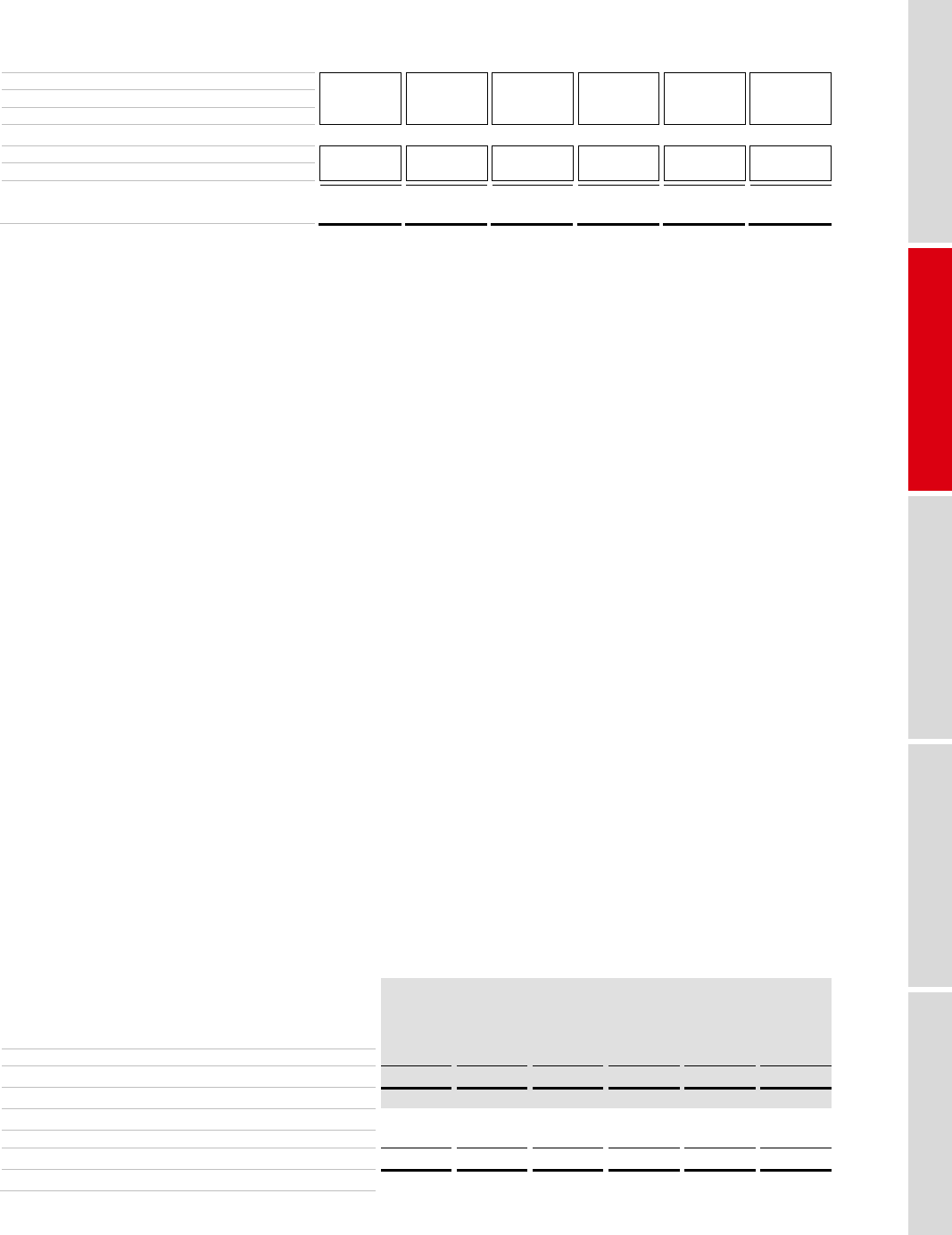

$m $m $m $m $m $m

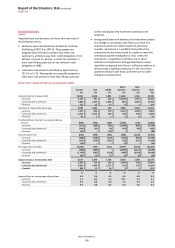

Individually assessed impairment allowances 617 351 32 190 590 1,780

–

new allowances 1,112 542 134 298 738 2,824

–

release of allowances no longer required (486) (171) (95) (88) (90) (930)

–

recoveries of amounts previously written off (9) (20) (7) (20) (58) (114)

Collectively assessed impairment allowances10 462 293 (33) 110 1,443 2,275

–

new allowances net of allowance releases 757 426 2 205 1,726 3,116

–

recoveries of amounts previously written off (295) (133) (35) (95) (283) (841)

Total loan impairment charge for the year ended

31 December 2014 1,079 644 (1) 300 2,033 4,055

For footnote, see page 191.

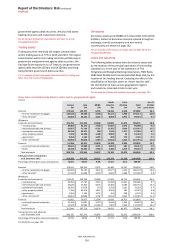

On a reported basis, loan impairment charges of $3.6bn

were $0.5bn lower than in 2014, primarily due to favourable

currency translation in Latin America and Europe.

The commentary that follows is on a constant currency basis,

while tables are presented on a reported basis.

Loan impairment charges increased by $219m compared

with 2014. Notably, in the fourth quarter of 2015, our loan

impairment charges increased compared with the third

quarter following a rise in individually assessed loan

impairment charges in a small number of countries. This was

reflective of specific circumstances associated with those

countries with no common underlying theme. In addition,

we increased our collectively assessed loan impairment

allowances on exposures related to the oil and gas industry

by $0.2bn. This was primarily in North America, Middle East

and North Africa, and Asia.

The commentary that follows sets out in more detail the

factors that have contributed to movements in loan

impairment charges compared with 2014.

Collectively assessed loan impairment allowances rose by

$221m, mainly in Middle East and North Africa, North

America and Asia, partly offset in Europe. It arose from

the following:

• in Middle East and North Africa (up by $167m), this was

mainly in the UAE and reflected increased impairment

allowances on our residential mortgage book following a

review of the quality and value of collateral. In addition,

loan impairment allowances increased on our corporate

and commercial exposures, notably in the oil and

foodstuffs industries;

• in North America (up by $132m) and Asia (up by $108m),

the increase was in the ‘other commercial’ sector. This

reflected an increase in allowances against our oil and

gas exposures in the regions. In our US CML portfolio,

loan impairment allowances on residential mortgages

were higher than in 2014 following lower favourable

market value adjustments of underlying properties as

improvements in housing market conditions were less

pronounced in 2015.

• in Europe, collectively assessed loan impairment

allowances were $192m lower as 2014 included

additional impairment charges from revisions to certain

estimates used in our corporate collective loan

impairment calculation.

Individually assessed loan impairment allowances were

broadly unchanged from 2014. This reflected decreases in

Latin America, Europe and Asia which were offset by

increases in Middle East and North Africa and in North

America. This included the following:

• in Latin America (down by $95m), Europe (down by

$44m) and Asia (down by $44m), we saw reductions in

individually assessed loan impairment allowances as 2014

included significant impairment charges related to

corporate and commercial exposures in our respective

regions. In Asia, the reduction was partly offset by an

increase in loan impairment allowances against a small

number of customers in Indonesia; and

• in Middle East and North Africa (up by $134m) and North

America (up by $47m), individually assessed loan

impairment allowances increased. In the former, this

primarily related to higher loan impairment allowances

on food wholesalers, while in North America the rise was

in the oil and gas sector.

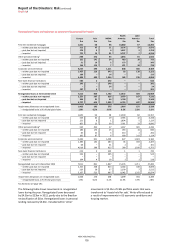

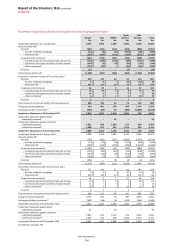

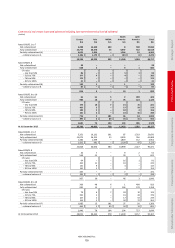

Charge for impairment losses as a percentage of average gross loans and advances to customers by geographical region

Europe Asia MENA

North

America

Latin

America Total

%%%% % %

New allowances net of allowance releases 0.31 0.23 1.07 0.41 5.37 0.48

Recoveries (0.11) (0.05) (0.11) (0.06) (0.50) (0.09)

Total charge for impairment losses at 31 December 2015 0.20 0.18 0.96 0.35 4.87 0.39

Amount written off net of recoveries 0.25 0.12 0.97 0.45 3.94 0.37

New allowances net of allowance releases 0.37 0.22 0.14 0.32 5.00 0.53

Recoveries (0.08) (0.04) (0.14) (0.09) (0.72) (0.10)

Total charge for impairment losses at 31 December 2014 0.29 0.18

–

0.23 4.28 0.43

Amount written off net of recoveries 0.49 0.13 0.58 0.97 3.59 0.58