HSBC 2015 Annual Report Download - page 333

Download and view the complete annual report

Please find page 333 of the 2015 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

338 -

339

339 -

340

340 -

341

341 -

342

342 -

343

343 -

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

|

|

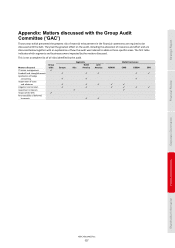

HSBC HOLDINGS PLC

331

Strategic Report Financial Review Corporate Governance Financial Statements Shareholder Information

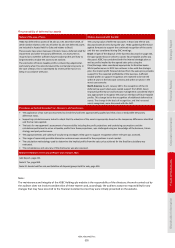

Impairment of loans and advances

Nature of the area of focus Matters discussed with the GAC

Impairment allowances represent management's best estimate of

the losses incurred within the loan portfolios at the balance sheet

date. They are calculated on a collective basis for portfolios of loans

of a similar nature and on an individual basis for significant loans.

The calculation of both collective and individual impairment

allowances is inherently judgemental for any bank.

Collective impairment allowances are calculated using statistical

models which approximate the impact of current economic and

credit conditions on large portfolios of loans. The inputs to these

models are subject to management judgement and model overlays

are often required.

For specific impairments, judgement is required to determine when

an impairment event has occurred and then to estimate the

expected future cash flows related to that loan.

The audit was focused on impairment due to the materiality of the

balances and the subjective nature of the calculation. The largest

loan portfolios are in Europe and Asia. The most significant

impairment allowances are in Europe, North America and Latin

America.

The policies and methodologies used by HSBC were discussed with

the GAC. The impairment policies and practices applied are consistent

with the requirements of IFRS. The methodologies used to calculate

collective impairment allowances are relatively standard which means

that modelling risk is low but that changes in individual inputs can

have a significant bearing on the impairment charge.

The discussion covered positive observations around the governance

supporting changes to model inputs and our observations on

suggested enhancements to documentation.

At each GAC and Group Risk Committee meeting there was a

discussion on changes to risk factors and other inputs within the

collective allowance models as well as discussions on individually

significant loan impairments. In light of the further deterioration in

the spot price of oil, a specific discussion on the exposures to the oil

and gas sector was held with GAC at the year end. This discussion

considered the appropriate treatment of the Group’s exposure within

the collective impairment calculation and the additional $0.2bn

increase at the year-end.

Procedures performed to support our discussions and conclusions

• The controls management has established to support their collective and specific impairment calculations were tested.

• For collective impairment this included controls over the appropriateness of models used to calculate the charge, the process of

determining key assumptions and the identification of loans to be included within the calculation.

• For specific impairment charges on individual loans this included controls over the compilation and review of the credit watch list, credit

file review processes, approval of external collateral valuation vendors and review controls over the approval of significant individual

impairments.

• For collective allowances the appropriateness of the modelling policy and methodology used for material portfolios was independently

assessed by reference to the accounting standards and market practices and model calculations were tested through re-performance

and code review.

• The appropriateness of management’s judgements was also independently considered in respect of calculation methodologies and

segmentation, economic factors and judgemental overlays, period of historical loss rates used, loss emergence periods, cure rates for

impaired loans and the valuation of recovery assets and collateral.

• For specific allowances the appropriateness of provisioning methodologies and policies was independently assessed for a sample of

loans across the portfolio selected on the basis of risk. An independent view was formed on the levels of provisions booked based on the

detailed loan and counterparty information in the credit file. Calculations within a sample of discounted cash flow models were re-

performed.

Relevant references in the Annual Report and Accounts 2015

Impaired loans, page 128.

Areas of special interest, page 116.

GAC Report, page 262.

Note 1 (j): Impairment of loans and advances, page 354.