Albertsons 2009 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2009 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

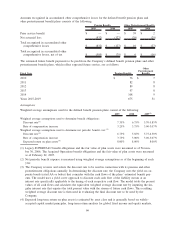

|

|

is subject to the uncertainties inherent in the litigation process, based on the information presently available to

the Company, management does not expect that the ultimate resolution of this lawsuit will have a material

adverse effect on the Company’s financial condition, results of operations or cash flows.

In September 2008, a class action complaint was filed against the Company, as well as International

Outsourcing Services, LLC (“IOS”), Inmar, Inc., Carolina Manufacturer’s Services, Inc., Carolina Coupon

Clearing, Inc. and Carolina Services, in the United States District Court in the Eastern District of Wisconsin.

The plaintiffs in the case are a consumer goods manufacturer, a grocery co-operative and a retailer marketing

services company who allege on behalf of a purported class that the Company and the other defendants

(i) conspired to restrict the markets for coupon processing services under the Sherman Act and (ii) were part

of an illegal enterprise to defraud the plaintiffs under the Federal Racketeer Influenced and Corrupt

Organizations Act. The plaintiffs seek monetary damages, attorneys’ fees and injunctive relief. The Company

intends to vigorously defend this lawsuit, however all proceedings have been stayed in the case pending the

result of the criminal prosecution of certain former officers of IOS. Although this lawsuit is subject to the

uncertainties inherent in the litigation process, based on the information presently available to the Company,

management does not expect that the ultimate resolution of this lawsuit will have a material adverse effect on

the Company’s financial condition, results of operations or cash flows.

In December 2008, a class action complaint was filed in the United States District Court for the Western

District of Wisconsin against the Company alleging that a 2003 transaction between the Company and C&S

Wholesale Grocers, Inc. (“C&S”) was a conspiracy to restrain trade and allocate markets. In the 2003

transaction, the Company purchased certain assets of the Fleming Corporation as part of Fleming Corporation’s

bankruptcy proceedings and sold certain of the assets of the Company to C&S which were located in New

England. The complaint alleges that the conspiracy was concealed and continued through the use of non-

compete and non-solicitation agreements and the closing down of the distribution facilities that the Company

and C&S purchased from the other. Plaintiffs are seeking monetary damages, injunctive relief and attorneys’

fees. The Company is vigorously defending this lawsuit. Although this lawsuit is subject to the uncertainties

inherent in the litigation process, based on the information presently available to the Company, management

does not expect that the ultimate resolution of this lawsuit will have a material adverse effect on the

Company’s financial condition, results of operations or cash flows.

The Company is also involved in routine legal proceedings incidental to its operations. Some of these routine

proceedings involve class allegations, many of which are ultimately dismissed. Management does not expect

that the ultimate resolution of these legal proceedings will have a material adverse effect on the Company’s

financial condition, results of operations or cash flows.

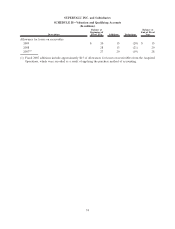

The statements above reflect management’s current expectations based on the information presently available

to the Company, however, predicting the outcomes of claims and litigation and estimating related costs and

exposures involves substantial uncertainties that could cause actual outcomes, costs and exposures to vary

materially from current expectations. In addition, the Company regularly monitors its exposure to the loss

contingencies associated with these matters and may from time to time change its predictions with respect to

outcomes and its estimates with respect to related costs and exposures and believes recorded reserves are

adequate. It is possible, although management believes it is remote, that material differences in actual

outcomes, costs and exposures relative to current predictions and estimates, or material changes in such

predictions or estimates, could have a material adverse effect on the Company’s financial condition, results of

operations or cash flows.

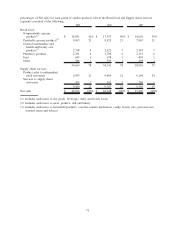

Pension Plan / Health and Welfare Plan Contingencies

The Company contributes to various multi-employer pension plans under collective bargaining agreements,

primarily defined benefit pension plans. These plans generally provide retirement benefits to participants based

on their service to contributing employers. Based on available information, the Company believes that some of

the multi-employer plans to which it contributes are underfunded. Company contributions to these plans could

increase in the near term. However, the amount of any increase or decrease in contributions will depend on a

variety of factors, including the results of the Company’s collective bargaining efforts, investment returns on

the assets held in the plans, actions taken by the trustees who manage the plans and requirements under the

Pension Protection Act and Section 412(e) of the Internal Revenue Code. Furthermore, if the Company were

70