Albertsons 2009 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2009 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

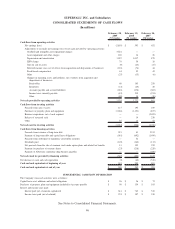

|

|

liabilities that are remeasured at least annually and did not have a material effect on the Company’s

consolidated financial statements. The Company will defer adoption of SFAS No. 157 for one year for

nonfinancial assets and nonfinancial liabilities that are recognized or disclosed at fair value in the financial

statements on a nonrecurring basis. The Company is evaluating the effect the implementation of FSP

FAS 157-2 will have on the consolidated financial statements.

In December 2007, the FASB issued SFAS No. 141 (revised 2007), “Business Combinations”

(“SFAS No. 141(R)”). SFAS No. 141(R) expands the definition of a business combination and requires the fair

value of the purchase price of an acquisition, including the issuance of equity securities, to be determined on

the acquisition date. SFAS No. 141(R) also requires that all assets, liabilities and any non-controlling interest

in an acquired business be recorded at fair value at the acquisition date. In addition, SFAS No. 141(R) requires

that acquisition costs generally be expensed as incurred, restructuring costs generally be expensed in periods

subsequent to the acquisition date and changes in accounting for deferred tax asset valuation allowances and

acquired income tax uncertainties after the measurement period impact income tax expense. SFAS No. 141(R)

is effective for the Company’s fiscal year beginning March 1, 2009 on a prospective basis for all business

combinations for which the acquisition date is on or after the effective date, with the exception of the

accounting for adjustments to income tax-related amounts, which is applied to acquisitions that closed prior to

the effective date. The adoption of SFAS No. 141(R) to prior acquisitions is not expected to have a material

effect on the Company’s consolidated financial statements.

In December 2007, the FASB issued SFAS No. 160, “Noncontrolling Interests in Consolidated Financial

Statements—an Amendment of ARB No. 51.” SFAS No. 160 changes the accounting and reporting for

minority interests such that minority interests will be recharacterized as noncontrolling interests and will be

required to be reported as a component of equity, and requires that purchases or sales of equity interests that

do not result in a change in control be accounted for as equity transactions and, upon a loss of control,

requires the interest sold, as well as any interest retained, to be recorded at fair value with any gain or loss

recognized in earnings. SFAS No. 160 is effective for the Company’s fiscal year beginning March 1, 2009,

with early adoption prohibited. The adoption of SFAS No. 160 is not expected to have a material effect on the

Company’s consolidated financial statements.

In April 2008, the FASB approved FSP FAS 142-3, “Determination of the Useful Life of Intangible Assets.”

FSP FAS 142-3 amends the factors that should be considered in developing renewal or extension assumptions

used to determine the useful life of a recognized intangible asset under SFAS No. 142, “Goodwill and Other

Intangible Assets.” FSP FAS 142-3 is effective for the Company’s fiscal year beginning March 1, 2009 on a

prospective basis to intangible assets acquired on or after the effective date, with early adoption prohibited.

In May 2008, the FASB approved FSP APB 14-1, “Accounting for Convertible Debt Instruments That May Be

Settled in Cash upon Conversion (Including Partial Cash Settlement).” FSP APB 14-1 clarifies that convertible

debt instruments that may be settled in cash upon conversion (including partial cash settlement) are not

addressed by paragraph 12 of Accounting Principles Board (“APB”) Opinion No. 14, “Accounting for

Convertible Debt and Debt issued with Stock Purchase Warrants.” Additionally, FSP APB 14-1 specifies that

issuers of such instruments should separately account for the liability and equity components in a manner that

will reflect the entity’s nonconvertible debt borrowing rate when interest cost is recognized in subsequent

periods. FSP APB 14-1 is effective for the Company’s fiscal year beginning March 1, 2009. The adoption of

FSP APB 14-1 is not expected to have a material effect on the Company’s consolidated financial statements.

In June 2008, the FASB issued FSP EITF 03-6-1, “Determining Whether Instruments Granted in Share-Based

Payment Transactions Are Participating Securities.” FSP EITF 03-6-1 addresses whether instruments granted

in share-based payment transactions are participating securities prior to vesting and, therefore, need to be

included in computing earnings per share under the two-class method described in SFAS No. 128, “Earnings

Per Share.” FSP EITF 03-6-1 requires companies to treat unvested share-based payment awards that have non-

forfeitable rights to dividend or dividend equivalents as a separate class of securities in calculating earnings

per share. FSP EITF 03-6-1 will be effective for the Company’s fiscal year beginning March 1, 2009, with

early adoption prohibited. The adoption of FSP EITF 03-6-1 is not expected to have a material effect on the

Company’s consolidated financial statements.

52