Albertsons 2009 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2009 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

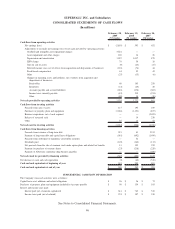

NOTE 5—PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment, net, consisted of the following:

2009 2008

Land $ 1,313 $ 1,335

Buildings 3,443 3,269

Property under construction 315 333

Leasehold improvements 1,613 1,383

Equipment 4,201 3,777

Capitalized leases 1,030 1,015

Total property plant and equipment 11,915 11,112

Accumulated depreciation (4,091) (3,347)

Accumulated amortization on capital leases (296) (232)

Total property, plant and equipment, net $ 7,528 $ 7,533

Depreciation expense was $945, $911 and $793 for fiscal 2009, 2008 and 2007, respectively. Amortization

expense related to capital leased assets was $67, $64 and $54 for fiscal 2009, 2008 and 2007, respectively.

NOTE 6—FAIR VALUES OF FINANCIAL INSTRUMENTS

For certain of the Company’s financial instruments, including cash and cash equivalents, receivables and

accounts payable, the fair values approximate book values due to their short maturities.

The estimated fair value of notes receivable was less than the book value by approximately $8 as of

February 28, 2009. The estimated fair value of notes receivable approximated the book value as of February 23,

2008. Notes receivable are valued based on a discounted cash flow approach applying a rate that is comparable

to publicly traded instruments of similar credit quality.

The estimated fair value of the Company’s long-term debt (including current maturities) was less than the

book value by approximately $452 and $42 as of February 28, 2009 and February 23, 2008, respectively. The

estimated fair value was based on market quotes, where available, or market values for similar instruments.

NOTE 7—LONG-TERM DEBT

The Company’s long-term debt and capital lease obligations consisted of the following:

55