Albertsons 2009 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2009 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

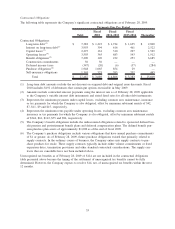

|

|

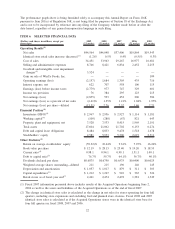

was not able to realize all or part of its net deferred tax assets in the future, the valuation allowance would be

increased. Likewise, if it was determined that the Company was more-likely-than-not to realize the net

deferred tax assets, the applicable portion of the valuation allowance would reverse. The Company had a

valuation allowance of $165 as of February 28, 2009 and February 23, 2008.

LIQUIDITY AND CAPITAL RESOURCES

Net cash provided by operating activities was $1,534, $1,732 and $801 in fiscal 2009, 2008 and 2007,

respectively. The decrease in cash provided by operating activities in fiscal 2009 compared to fiscal 2008 is

primarily attributable to the impact of deferred income taxes. The increase in cash provided by operating

activities in fiscal 2008 compared to fiscal 2007 is primarily attributable to the impact of the Acquired

Operations on Net earnings, Depreciation and amortization and working capital.

Net cash used in investing activities was $1,014, $968 and $2,760 in fiscal 2009, 2008 and 2007, respectively.

Fiscal 2009 and 2008 investing activities primarily reflect capital spending to fund retail store remodeling

activity, new retail stores and technology expenditures. Fiscal 2007 investing activities primarily reflect the net

assets acquired in the Acquisition and capital spending to fund retail store remodeling and new stores.

Net cash (used in) provided by financing activities was $(523), $(806) and $1,443 in fiscal 2009, 2008 and

2007, respectively. Fiscal 2009 financing activities primarily reflect net payments of long-term debt and capital

lease obligations and payment of dividends. Fiscal 2008 financing activities primarily reflect net payments of

long-term debt and capital lease obligations, payment of dividends and purchases of treasury shares offset by

proceeds received from the sale of common stock under the Company’s stock option plans. Fiscal 2007

financing activities primarily reflect the debt incurred in connection with the Acquisition and senior notes

issued in October 2006, partially offset by repayment of long-term debt of Albertsons standalone drug business

payables related to the sale of Albertsons.

Management expects that the Company will continue to replenish operating assets with internally generated

funds. There can be no assurance, however, that the Company’s business will continue to generate cash flow at

current levels. The Company will continue to obtain short-term or long-term financing from its credit facilities.

Long-term financing will be maintained through existing and new debt issuances. Maturities of debt issued

will depend on management’s views with respect to the relative attractiveness of interest rates at the time of

issuance and other debt maturities. Although there can be no assurances in these difficult economic times for

financial institutions, the Company believes that the lenders participating in its credit facilities will be willing

and able to provide financing to the Company in accordance with their legal obligations under the credit

facilities. While the Company’s short-term and long-term financing abilities are believed to be adequate as a

supplement to internally generated cash flows to fund capital expenditures and acquisitions as opportunities

arise, the current decline in the global financial markets may negatively impact the Company’s ability to

access the capital markets in a timely manner and on attractive terms. While management believes that the

Company’s cash flows and revolving credit facility will be more than sufficient to meet the Company’s

financing needs through fiscal 2011, the Company is also evaluating appropriate timing for accessing the debt

markets, which have shown recent improvement. In addition, the Company expects to renew its accounts

receivable securitization program which expires in May 2009.

Certain of the Company’s credit facilities and long-term debt agreements have restrictive covenants and cross-

default provisions which generally provide, subject to the Company’s right to cure, for the acceleration of

payments due in the event of a breach of the covenant or a default in the payment of a specified amount of

indebtedness due under certain other debt agreements. The Company was in compliance with all such

covenants and provisions for all periods presented.

The Company has senior secured credit facilities in the amount of $4,000. These facilities were provided by a

group of lenders and consist of a $2,000 five-year revolving credit facility (the “Revolving Credit Facility”), a

$750 five-year term loan (“Term Loan A”) and a $1,250 six-year term loan (“Term Loan B”). The rates in

effect on outstanding borrowings under the facilities as of February 28, 2009, based on the Company’s current

credit ratings, were 0.20 percent for the facility fees, LIBOR plus 0.875 percent for Term Loan A, LIBOR

plus 1.25 percent for Term Loan B, LIBOR plus 1.00 percent for revolving advances and Prime Rate plus

0.00 percent for base rate advances.

32