3M 2009 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2009 3M annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

84

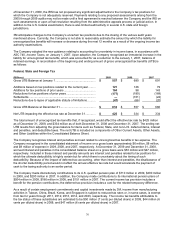

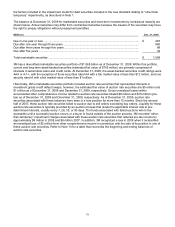

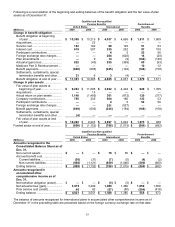

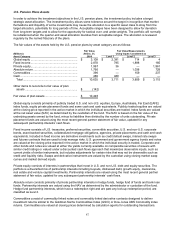

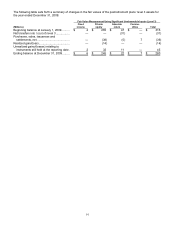

The accumulated benefit obligation of the U.S. pension plans was $10.769 billion and $9.844 billion at December 31,

2009 and 2008, respectively. The accumulated benefit obligation of the international pension plans was $4.279 billion

and $3.681 billion at December 2009 and 2008, respectively.

The following amounts relate to pension plans with accumulated benefit obligations in excess of plan assets as of

December 31:

Qualified and Non-qualified Pension Plans

United States International

(Millions) 2009 2008 2009 2008

Projected benefit obligation........................

$ 454 $ 10,395 $ 3,322 $ 3,562

Accumulated benefit obligation ..................

448 9,844 3,126 3,293

Fair value of plan assets ............................

23 9,243 2,526 2,529

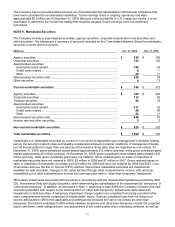

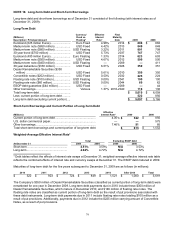

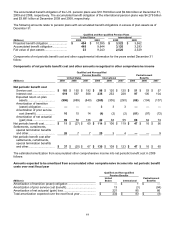

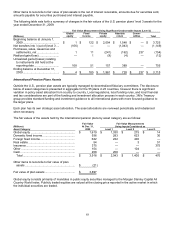

Components of net periodic benefit cost and other supplemental information for the years ended December 31

follow:

Components of net periodic benefit cost and other amounts recognized in other comprehensive income

Qualified and Non-qualified

Pension Benefits Postretirement

United States International Benefits

(Millions) 2009 2008 2007 2009 2008 2007 2009 2008 2007

Net periodic benefit cost

Service cost ............................ $ 183 $ 192 $ 192 $98

$ 120 $ 125 $ 51 $ 53 $ 57

Interest cost ............................ 619 597 568 235 252 228 97 100 104

Expected return on plan

assets.................................. (906) (889) (840) (260) (305) (290) (86) (104) (107)

Amortization of transition

(asset) obligation................. —

—

—

3

3 3

—

— —

Amortization of prior service

cost (benefit) ....................... 16 15 14 (4) (2) (2) (81) (97) (72)

Amortization of net actuarial

(gain) loss............................ 99 58 126 42 38 55 66 64 74

Net periodic benefit cost............. $ 11 $ (27) $ 60 $ 114 $ 106 $ 119 $ 47 $ 16 $ 56

Settlements, curtailments,

special termination benefits

and other................................. 26 7 7 25 3 4

—

— 9

Net periodic benefit cost after

settlements, curtailments,

special termination benefits

and other................................. $ 37 $ (20) $ 67 $ 139 $ 109 $ 123 $ 47 $ 16 $ 65

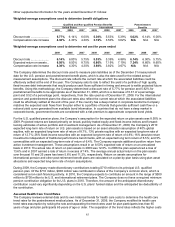

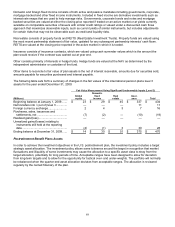

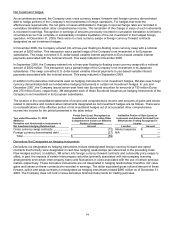

The estimated amortization from accumulated other comprehensive income into net periodic benefit cost in 2009

follows:

Amounts expected to be amortized from accumulated other comprehensive income into net periodic benefit

costs over next fiscal year

Qualified and Non-qualified

Pension Benefits

(Millions)

United

States International

Postretirement

Benefits

Amortization of transition (asset) obligation ................................... $ — $ 1 $ —

Amortization of prior service cost (benefit)..................................... 13 (3) (94)

Amortization of net actuarial (gain) loss ......................................... 221 85 86

Total amortization expected over the next fiscal year.................... $ 234 $ 83 $ (8)