Toyota 2010 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2010 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

TOYOTA ANNUAL REPORT 2010 69

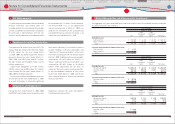

dividing net income attributable to Toyota Motor

Corporation by the weighted-average number of

shares outstanding during the reported period.

The calculation of diluted net income attributable

to Toyota Motor Corporation per common share

is similar to the calculation of basic net income

attributable to Toyota Motor Corporation per

share, except that the weighted-average number

of shares outstanding includes the additional

dilution from the assumed exercise of dilutive

stock options.

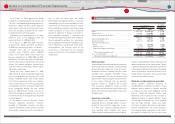

Stock-based compensation

Toyota measures compensation expense for its

stock-based compensation plan based on the

grant-date fair value of the award.

Other comprehensive income

Other comprehensive income refers to revenues,

expenses, gains and losses that, under U.S. GAAP

are included in comprehensive income, but

are excluded from net income as these amounts

are recorded directly as an adjustment to

shareholders equity. Toyotas other comprehensive

income is primarily comprised of unrealized

gains/losses on marketable securities designated

as available-for-sale, foreign currency translation

adjustments and adjustments attributed to

pension liabilities or minimum pension liabilities

associated with Toyotas defi ned benefi t pension

plans.

Accounting changes

In December 2007, FASB issued updated

guidance of accounting for and disclosure

of business combinations. This guidance

establishes principles and requirements for

how the acquirer recognizes and measures

the identifi able assets acquired, the liabilities

assumed, any noncontrolling interest, and the

goodwill acquired in a business combination or a

gain from a bargain purchase. Also, this guidance

provides several new disclosure requirements

that enable users of the fi nancial statements

to evaluate the nature and fi nancial eff ects of

the business combination. Toyota adopted this

guidance from the business combinations on

and after the beginning of fi scal year begun on

or after December 15, 2008. The adoption of

this guidance did not have a material impact on

Toyotas consolidated fi nancial statements.

In December 2007, FASB issued updated

guidance of accounting for and disclosure

of consolidation. This guidance establishes

accounting and reporting standards for the

noncontrolling interest in a subsidiary and for

the deconsolidation of a subsidiary. Toyota

adopted this guidance from the fi scal year

begun on or after December 15, 2008. As a result,

noncontrolling interest, formerly reported as

minority interest, is reported as shareholders

equity in the consolidated balance sheets, and

the amount of net income attributable to the

parent and to the noncontrolling interest are

identifi ed and presented in the consolidated

statements of income. Since the presentation

and disclosure requirements have been applied

retrospectively for all periods presented in the

consolidated fi nancial statements in which this

guidance is applied, certain prior year amounts

have been reclassifi ed to conform to this

guidance. The adoption of this guidance did not

have a material impact on Toyotas consolidated

fi nancial statements.

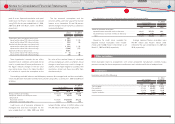

In December 2008, FASB issued updated

guidance of accounting for and disclosure

of compensation. This guidance requires

additional disclosures about postretirement

benefi t plan assets including investment policies

and strategies, classes of plan assets, fair value

measurements of plan assets, and signifi cant

concentrations of risk. Toyota adopted this

guidance from the fi scal year ended after

December 15, 2009. The adoption of this

guidance did not have a material impact on

Toyotas consolidated fi nancial statements.

In April 2009, FASB issued updated guidance

of accounting for and disclosure of investments.

This guidance revises the recognition and

presentation requirements for other-than-

temporary impairments of debt securities, and

contains additional disclosure requirements

related to debt and equity securities. Toyota

adopted this guidance from the fi scal year

ended after June 15, 2009. The adoption of this

guidance did not have a material impact on

Toyotas consolidated fi nancial statements.

In May 2009, FASB issued updated guidance

of accounting for and disclosure of subsequent

events. This guidance is intended to establish

general standards of accounting for and

disclosure of events that occur after the balance

sheet date but before fi nancial statements are

issued. Toyota adopted this guidance from the

fi scal year ended after June 15, 2009. The adoption

of this guidance did not have a material impact

on Toyotas consolidated fi nancial statements.

Recent pronouncements to be adopted in

future periods

In June 2009, FASB issued updated guidance of

accounting for and disclosure of transfers and

servicing. This guidance eliminates the concept

of a qualifying special-purpose entity, changes

the requirements for derecognizing fi nancial

assets, and requires additional disclosures about

transfers of fi nancial assets. This guidance is

eff ective for fi scal year beginning after November

15, 2009, and for interim period within the fi scal

year. Management is evaluating the impact of

adopting this guidance on Toyotas consolidated

fi nancial statements.

In June 2009, FASB issued updated guidance of

accounting for and disclosure of consolidation.

This guidance changes how a company

determines when a variable interest entity

should be consolidated. This guidance is eff ective

for fi scal year beginning after November 15,

2009, and for interim period within the fi scal

year. Management is evaluating the impact of

adopting this guidance on Toyotas consolidated

fi nancial statements.

Reclassifi cations

Certain prior year amounts have been reclassifi ed

to conform to the presentations as of and for the

year ended March 31, 2010.

Financial Section

Notes to Consolidated Financial Statements

Financial Section

Investor Information

Corporate Information

Consolidated

Performance Highlights

Business Overview

Special Feature

Top Messages