Macy's 2014 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2014 Macy's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

26

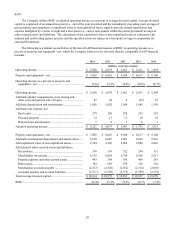

The credit agreement requires the Company to maintain a specified interest coverage ratio for the latest four quarters

of no less than 3.25 and a specified leverage ratio as of and for the latest four quarters of no more than 3.75. The

Company's interest coverage ratio for 2014 was 9.68 and its leverage ratio at January 31, 2015 was 1.83, in each case as

calculated in accordance with the credit agreement. The interest coverage ratio is defined as EBITDA divided by net

interest expense and the leverage ratio is defined as debt divided by EBITDA. For purposes of these calculations EBITDA

is calculated as net income plus interest expense, taxes, depreciation, amortization, non-cash impairment of goodwill,

intangibles and real estate, non-recurring cash charges not to exceed in the aggregate $400 million and extraordinary losses

less interest income and non-recurring or extraordinary gains. Debt is adjusted to exclude the premium on acquired debt

and net interest is adjusted to exclude the amortization of premium on acquired debt and premium on early retirement of

debt.

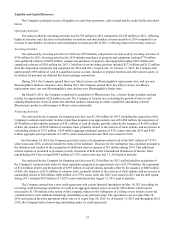

A breach of a restrictive covenant in the Company's credit agreement or the inability of the Company to maintain the

financial ratios described above could result in an event of default under the credit agreement. In addition, an event of

default would occur under the credit agreement if any indebtedness of the Company in excess of an aggregate principal

amount of $150 million becomes due prior to its stated maturity or the holders of such indebtedness become able to cause it

to become due prior to its stated maturity. Upon the occurrence of an event of default, the lenders could, subject to the

terms and conditions of the credit agreement, elect to declare the outstanding principal, together with accrued interest, to be

immediately due and payable.

Moreover, most of the Company's senior notes and debentures contain cross-default provisions based on the non-

payment at maturity, or other default after an applicable grace period, of any other debt, the unpaid principal amount of

which is not less than $100 million, that could be triggered by an event of default under the credit agreement. In such an

event, the Company's senior notes and debentures that contain cross-default provisions would also be subject to

acceleration.

At January 31, 2015, no notes or debentures contain provisions requiring acceleration of payment upon a debt rating

downgrade. However, the terms of approximately $4,300 million in aggregate principal amount of the Company's senior

notes outstanding at that date require the Company to offer to purchase such notes at a price equal to 101% of their

principal amount plus accrued and unpaid interest in specified circumstances involving both a change of control (as defined

in the applicable indenture) of the Company and the rating of the notes by specified rating agencies at a level below

investment grade.

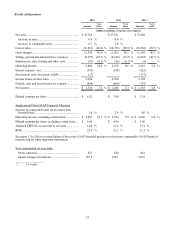

The Company's board of directors approved an additional authorization to purchase Common Stock of $1,500

million on May 14, 2014. During 2014, the Company repurchased approximately 31.9 million shares of its common stock

for a total of $1,900 million. As of January 31, 2015, the Company had $1,032 million of authorization remaining under its

share repurchase program. The Company may continue or, from time to time, suspend repurchases of shares under its share

repurchase program, depending on prevailing market conditions, alternate uses of capital and other factors.

On February 27, 2015, the Company's board of directors declared a quarterly dividend of 31.25 cents per share on its

common stock, payable April 1, 2015 to Macy's shareholders of record at the close of business on March 13, 2015.