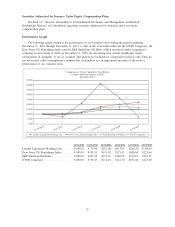

Lumber Liquidators 2015 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2015 Lumber Liquidators annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

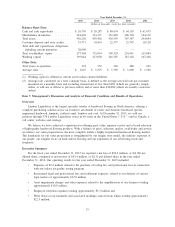

Cash Flows

Operating Activities. Net cash provided by operating activities was $9.2 million for 2015,

$57.1 million for 2014 and $53.0 million for 2013. The $47.9 million decrease in net cash flow from

operating activities comparing 2015 to 2014 is primarily due to unprofitable operations, a decrease in

merchandise inventories of $42.8 million, and a decrease in accounts payable of $21.5 million. The

$4.1 million increase in net cash flow from operating activities comparing 2014 to 2013 is primarily due to

our profitable operations, an increase in customer deposits and store credits of $12.6 million, an increase in

merchandise inventories of $62.1 million, and an increase in accounts payable of $21.5 million.

Investing Activities. Net cash used in investing activities was $22.5 million for 2015, $71.1 million for

2014 and $28.6 million for 2013. Net cash used in investing activities in each year included capital purchases

for store base expansion, and investments in and maintenance of forklifts, our integrated information

technology solution, our finishing lines and our Corporate Headquarters. In 2014 and 2013, capital

expenditures also included remodeling of existing stores to our expanded showroom format and $37.6 million

and $8.4 million, respectively, for land, buildings and equipment for the East Coast distribution facility and

$1.2 million and $2.1 million, respectively, for equipment and leasehold improvements for the West Coast

distribution facility.

Financing Activities. Net cash provided by financing activities was $19.7 million in 2015. Net cash

used in financing activities was $46.2 million in 2014 and $7.4 million in 2013. We used cash of $0.3 million,

$53.3 million and $34.8 million in 2015, 2014 and 2013, respectively, to repurchase our common stock,

primarily under our stock repurchase program initiated in February 2012. Stock option exercises provided

$7.2 million and $27.3 million in 2014 and 2013, respectively. During 2015, we had net borrowings of

$20.0 million under our revolving credit facility to fund capital expenditures and inventory purchases.

Revolving Credit Agreement

On April 24, 2015, the Company, exclusive of its non-domestic subsidiaries, entered into a Second

Amended and Restated Credit Agreement (as amended on May 21, 2015 and November 20, 2015, the ‘‘Credit

Agreement’’) with Bank of America, N.A. as administrative agent, collateral agent and lender (the ‘‘Bank’’).

The Credit Agreement amended and restated the Amended and Restated Credit Agreement that was entered

into between Lumber Liquidators, Inc. and the Bank on February 21, 2012 and amended on March 27, 2015.

Under the Credit Agreement, the Bank agreed to provide the Company with an asset-based revolving credit

facility (the ‘‘Revolving Credit Facility’’) under which the Company may obtain loans and letters of credit

from the Bank up to a maximum aggregate outstanding principal amount of the lesser of $100.0 million or a

calculated borrowing base. Letters of credit are subject to a sublimit of $20.0 million (subject to the

borrowing base). The Credit Agreement expires on April 24, 2020, is guaranteed by the Company and certain

of its domestic subsidiaries and is secured primarily by the Company’s inventory, including certain in-transit

inventory, and credit card receivables.

The Revolving Credit Facility has no mandated payment provisions and a fee of 0.15% per annum on

any unused portion, paid quarterly in arrears. Loans outstanding under the Revolving Credit Facility can bear

interest based on the Base Rate or the LIBOR Rate, each as defined in the Credit Agreement. Interest on Base

Rate loans is charged at varying per annum rates computed by applying a margin ranging from 0.125% to

0.375% (dependent on the Company’s average daily excess borrowing availability during the most recently

completed fiscal quarter) over the applicable base interest rate (defined as the greatest of the prime rate, a

specified federal funds rate plus 0.50%, or the one-month LIBOR Rate plus 1.00%). Interest on LIBOR Rate

loans and fees for standby letters of credit are charged at varying per annum rates computed by applying a

margin ranging from 1.125% to 1.375% (dependent on the Company’s average daily excess borrowing

availability during the most recently completed fiscal quarter) over the applicable LIBOR rate for one, two,

three or six month interest periods as selected by the Company. At December 31, 2015, the applicable interest

rate for outstanding borrowings was 1.4375%. For the year ended December 31, 2015, the Company paid cash

for interest in the amount of $0.2 million.

The Credit Agreement contains a fixed charge coverage ratio covenant that becomes effective in the event

that the Company’s excess borrowing availability under the Revolving Credit Facility at any time during the

term of the Revolving Credit Facility falls below the greater of $10.0 million or 10% of the borrowing base.

41