Lumber Liquidators 2011 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2011 Lumber Liquidators annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

|

|

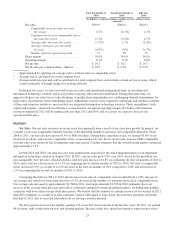

In 2012, we expect capital expenditures to total between $9 million and $12 million. In addition to general capital

requirements, we intend to:

• open between 20 and 25 new store locations;

• continue to relocate and remodel existing stores;

• continue to invest in our integrated technology solution;

• significantly upgrade our forklifts; and

• continue to improve the effectiveness of our marketing programs.

Cash and Cash Equivalents

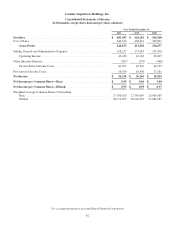

In 2011, cash and cash equivalents increased $26.8 million to $61.7 million as $44.1 million of cash provided by

operating activities and $4.8 million of proceeds received from stock option exercises were partially offset by the use of

$17.0 million to purchase property and equipment and $4.7 million to acquire certain assets of Sequoia. In 2010, cash and

cash equivalents decreased $0.8 million to $34.8 million. The decrease in cash and cash equivalents was primarily due to the

use of $20.5 million in capital expenditures, including software and hardware related to our integrated technology solution,

partially offset by $17.0 million in cash provided by operating activities and $3.1 million of proceeds received from stock

option exercises. In 2009, cash and cash equivalents increased $0.5 million to $35.7 million, as $7.8 million of cash provided

by operating activities and $4.5 million of proceeds received from stock option exercises were partially offset by the use of

$11.4 million to purchase property and equipment.

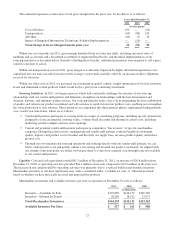

Cash Flows

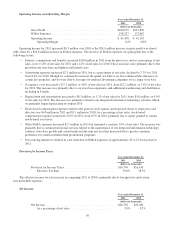

Operating Activities. Net cash provided by operating activities was $44.1 million for 2011, $17.0 million for 2010 and

$7.8 million for 2009. The $27.1 million increase in net cash comparing 2011 to 2010 is due primarily to a reduction in

merchandise inventories net of the change in accounts payable, customer deposits and store credits and certain other working

capital items. The $9.2 million increase in net cash comparing 2010 to 2009 is due primarily to a lower build in merchandise

inventories net of the change in accounts payable, the timing of certain tax items, and an increase in customer deposits

outstanding, partially offset by net changes in certain other working capital items, including prepaid expenses.

Investing Activities. Net cash used in investing activities was $21.7 million for 2011, $20.5 million for 2010 and $11.4

million for 2009. Net cash used in investing activities for 2011 included $4.7 million cash paid for the Sequoia acquisition.

Net cash used in investing activities included capital expenditures related to our integrated technology solution of $4.3

million in 2011, $11.3 million in 2010 and $3.9 million in 2009. In addition, net cash used in investing activities in each year

included capital purchases of store fixtures, equipment and leasehold improvements for store opened, relocated or remodeled,

investment in certain equipment including our finishing line and forklifts, routine capital purchases of computer hardware

and software, and certain leasehold improvements in our Corporate Headquarters.

Financing Activities. Net cash provided by financing activities was $4.5 million, $2.7 million and $4.2 million in 2011,

2010 and 2009, respectively, primarily due to equity activity, including the exercise of stock options.

Revolving Credit Agreement

A revolving credit agreement (the “Revolver”) providing for borrowings up to $25.0 million was available to us through

expiration on August 10, 2012. During 2011, 2010 and 2009, we did not borrow against the Revolver and at December 31,

2011 and 2010, there were no outstanding commitments under letters of credit. The Revolver is primarily available to fund

inventory purchases, including the support of up to $5.0 million for letters of credit, and for general operations. The Revolver

is secured by our inventory, has no mandated payment provisions and we pay a fee of 0.125% per annum, subject to

adjustment based on certain financial performance criteria, on any unused portion of the Revolver. Amounts outstanding

under the Revolver would be subject to an interest rate of LIBOR (reset on the 10th of the month) plus 0.50%, subject to

adjustment based on certain financial performance criteria. The Revolver has certain defined covenants and restrictions,

including the maintenance of certain defined financial ratios. We were in compliance with these financial covenants at

December 31, 2011.

Subsequent to December 31, 2011, the Company amended the Revolver (the “Amended Revolver”) to provide for

borrowings up to $50.0 million through expiration in February 2017. The Amended Revolver is secured by LLI’s inventory,

supports up to $10.0 million in letters of credit, has no mandated payment provisions and a fee of 0.1% per annum, subject to

adjustment based on certain financial performance criteria, on any unused portion of the Amended Revolver. Amounts

outstanding under the Amended Revolver would be subject to an interest rate of LIBOR plus 1.125%, subject to adjustment

based on certain financial performance criteria. The Amended Revolver has certain defined covenants and restrictions,

including the maintenance of certain defined financial ratios.

34