Lumber Liquidators 2011 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2011 Lumber Liquidators annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

|

|

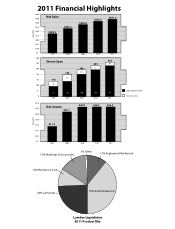

of certain products, ease of installation and lower average retail price points, hardwood flooring’s share of the overall U.S.

floor coverings market continues to increase. Similar to the overall U.S. floor coverings market, we estimate that the

hardwood flooring market has contracted approximately 13.5% since 2008.

Based on Catalina’s January 2012 Wood Flooring and December 2010 Floor Coverings Industry reports, we estimate

that the 2011 retail value of U.S. hardwood and laminate flooring was approximately $3.5 billion and $1.8 billion,

respectively, with the residential replacement market representing approximately 75% to 80%. Considering our sales mix of

hardwood and laminate flooring, we estimate that we have increased our market share in 2011. Further, Catalina projects the

hardwood flooring market will average annual growth of 4% per year 2012 through 2015.

The residential replacement wood flooring market is dependent on home-related, large-ticket discretionary spending,

which is influenced by a number of complex economic and demographic factors that may vary locally, regionally and

nationally. The market is impacted by, among other things, home remodeling activity, employment levels, housing turnover,

real estate prices, new housing starts, consumer confidence, credit availability and the general health of consumer

discretionary spending. Many of the economic indicators associated with the wood flooring market and generally associated

with consumer discretionary spending remain weak. Though we believe we have seen signs of stabilization at historically

low levels, we expect the wood flooring market to remain in a weakened state throughout 2012.

We believe the number of independent retailers serving the homeowner-based segment of the wood flooring market

continues to shrink under the difficult macroeconomic pressures. We believe our results have benefited from our gain of

market share in this environment and that we will continue to gain market share, primarily through new store openings. We

continue to believe that the longer term trends for our market remain favorable, including customer perception of hardwood

flooring as an attractive alternative to other floor coverings, the evolution of the hardwood flooring market, overall home

improvement spending and certain demographic trends.

Our Competition

We are the largest specialty retailer of hardwood flooring in the United States, and compete in a hardwood flooring

market that is highly fragmented. Catalina estimates that Lumber Liquidators, Home Depot and Lowes together represent

approximately 37% of hardwood flooring retail sales. The remainder of the market consists predominantly of regional and

local independent retailers and smaller national chains which specialize in the lower-end, higher-volume flooring market and

offer a wide range of home improvement products other than flooring. We also compete against smaller national specialty

flooring chains, some of which have an Internet presence, and a large number of local and regional independent flooring

retailers, including a large number of privately-owned single-site enterprises. Most of these retailers purchase their hardwood

flooring from domestic manufacturers or distributors, and typically do not stock hardwood flooring, but order it only when

the customer makes a purchase. As a result, we believe it takes these retailers longer than us to deliver their product to

customers, and their prices tend to be higher than ours. We also compete against companies that sell other types of floor

coverings, such as carpet, vinyl sheet and tile, ceramic tile, natural stone and others.

Seasonality and Quarterly Results

Our quarterly results of operations fluctuate depending on the timing of our advertising expenses and the timing of, and

income contributed by, our new stores. Our net sales also fluctuate slightly as a result of seasonal factors. We experience

slightly higher net sales in spring and fall, when more home remodeling activities are taking place, and slightly lower net

sales in holiday periods and during the hottest summer months. These seasonal fluctuations, however, are minimized to some

extent by our national presence, as markets experience different seasonal characteristics.

Our Employees

As of December 31, 2011, we had 1,302 employees, 97% of whom were full-time and none of whom were represented

by a union. Of these employees, 68% work in our stores, 17% work in corporate store support infrastructure or similar

functions (including our call center employees) and 15% work either on our finishing line or in our distribution center. We

believe that we have good relations with our employees.

Intellectual Property and Trademarks

We have a number of marks registered in the United States, including Lumber Liquidators®, Bellawood®,

1-800-HARDWOOD®, 1-800-FLOORING®, Dura-Wood®, Quickclic®, Virginia Mill Works Co. Hand Scraped and

9