Honda 2014 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2014 Honda annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

|

|

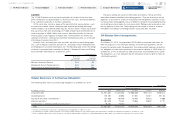

The following table provides information related to losses on operating leases

due to customer defaults:

Yen (billions)

Fiscal years ended March 31 2013 2014

Provision for credit losses on past

due rental payments ¥1.1 ¥1.7

Impairment losses on operating leases

due to early termination ¥4.7 ¥3.3

Fiscal Year 2014 Compared with Fiscal Year 2013

The provision for credit losses on finance receivables increased by ¥11.2 billion,

or 122.9%, and net charge-offs increased by ¥2.9 billion, or 21.6%. The increase

in net charge-offs was primarily due to the increase in finance receivables and

declines in used vehicle prices which reduced recoveries on repossessed col-

lateral in North America. Impairment losses on operating leases due to early

termination decreased by ¥1.4 billion, or 29.8%.

Losses on Lease Residual Values

Our finance subsidiaries in North America determine contractual residual values of

lease vehicles at lease inception based on expectations of future used vehicle

values, taking into consideration external industry data and our own historical

experience. Lease customers have the option at the end of the lease term to

return the vehicle to the dealer or to buy the vehicle for the contractual residual

value (or if purchased prior to lease maturity, at the outstanding contractual

balance). Returned lease vehicles can be purchased by the grounding dealer for

the contractual residual value (or if purchased prior to lease maturity, at the

outstanding contractual balance) or through market based pricing programs.

Returned lease vehicles that are not purchased by the grounding dealers are sold

through online and physical auctions. We are exposed to risk of loss on the dispo-

sition of returned lease vehicles when the proceeds from the sale of the vehicles

are less than the contractual residual values at the end of the lease term.

We assess our estimates for end of term market values of lease vehicles, at

minimum, on a quarterly basis. The primary factors affecting the estimates the

percentage of leased vehicles that we expect to be returned by the lessee at the

end of lease term and the expected loss severity. Factors considered in this evalu-

ation include, among other factors, economic conditions, historical trends, and

market information on new and used vehicles. For operating leases, adjustments

to estimated residual values are made on a straight-line basis over the remaining

term of the lease and are included as depreciation expense. For direct financing

leases, downward adjustments for declines in estimated residual values deemed

to be other-than-temporary are recognized as a loss on lease residual values in

the period in which the estimate changed.

We also review our investment in operating leases for impairment whenever

events or changes in circumstances indicate that their carrying values may not be

recoverable. If impairment conditions are met, impairment losses are measured by

the amount carrying values exceed their fair values. There were no events or cir-

cumstances that indicated that the carrying values of our operating leases would

not be recoverable during the fiscal years ended March 31, 2012, 2013, and 2014.

We believe that our estimated losses on lease residual values and impairment

losses is a “critical accounting estimate” because it is highly susceptible to market

volatility and requires us to make assumptions about future economic trends and

lease residual values, which are inherently uncertain. We believe that the assump-

tions used are appropriate. However actual losses incurred may differ from original

estimates as a result of actual results varying from those assumed in our estimates.

If future auction values for all Honda and Acura vehicles in our North American

operating lease portfolio as of March 31, 2014, were to decrease by approximately

¥10,000 per unit from our present estimates, holding all other assumption con-

stant, the total impact would be an increase in depreciation expense by approxi-

mately ¥4.6 billion, which would be recognized over the remaining lease terms.

Similarly, if future return rates for our existing portfolio of all Honda and Acura

vehicles were to increase by one percentage point from our present estimates, the

total impact would be an increase in depreciation expense by approximately ¥0.6

billion, which would be recognized over the remaining lease terms. With the same

prerequisites shown above, if future auction values in our North American direct

financing lease portfolio were to decrease by approximately ¥10,000 per unit from

our present estimates, the total impact would be an increase in losses on lease

residual values by approximately ¥0.1 billion. And if future return rates were to

increase by one percentage point from our present estimates, the total impact

would be slight. Note that this sensitivity analysis may be asymmetric, and are

specific to the base conditions in fiscal 2014. Also, declines in auction values are

likely to have a negative effect on return rates which could affect the sensitivities.

Pension and Other Postretirement Benefits

We have various pension plans covering substantially all of our employees in

Japan and certain employees in foreign countries. Benefit obligations and pension

costs are based on assumptions of many factors, including the discount rate, the

rate of salary increase and the expected long-term rate of return on plan assets.

The discount rate is determined mainly based on the rates of high quality corpo-

rate bonds currently available and expected to be available during the period to

maturity of the defined benefit pension plans. The salary increase assumptions

reflect our actual experience as well as near-term outlook. Honda determines the

expected long-term rate of return based on the investment policies. Honda con-

siders the eligible investment assets under investment policies, historical experi-

ence, expected long-term rate of return under the investing environment, and the

long-term target allocations of the various asset categories. Our assumed dis-

count rate and rate of salary increase as of March 31, 2014 were 1.5% and 2.2%,

Honda Motor Co., Ltd. Annual Report 2014 41

6 Financial Section

1 The Power of Dreams

2 Financial Highlights

3 To Our Shareholders

4 Review of Operations

5 Corporate Governance

7

Investor Relations

Information

Return to last

page opened

Go to

contents page